|

GLOBAL PORTFOLIO DIVERSIFICATION WITH

CRYPTOCURRENCIES

Master thesis submitted to the Faculty of Economics and

Business

Institute of Financial Analysis

University of Neuchâtel

For the Master of Science in Finance

by

Salma OUALI

Supervised by:

Prof. Frédéric SONNEY,

University of Neuchâtel

Neuchâtel, August 2019

|

Faculté des sciences économiques Avenue du

1er-Mars 26 CH-2000 Neuchâtel

www.unine.ch/seco

|

|

1

Abstract

This study raises questions about the potential of

cryptocurrencies as a new alternative investment. I explore the ability to

which major cryptocurrencies endow diversification and hedging benefits to a

global investor. Using the dynamic conditional correlation model developed by

Engle (2002), I find evidence of effective diversification and weak hedging

effects against global traditional assets. Furthermore, I investigate the issue

using risk based portfolio optimization frameworks. I find enhanced performance

of the investor's portfolio when including Bitcoin to a well-diversified

portfolio. Likewise, later generation of cryptocurrencies Ripple, Dash and

Litecoin provide better improvement on a risk adjusted basis. Nonetheless,

their very high volatility worsen off the portfolio's downside risk.1

1 ACKNOWLEDGEMENTS: I would like to express

my gratitude to my supervisor Prof. Frédéric Sonney for his

guidance and valuable advice. I would like to thank my family for their love

and unconditional support. I am also grateful to my partner and my best friend

for brightening my life throughout the thesis process.

2

1. Introduction

The 2008 financial crisis led to growing skepticism around

traditional financial systems.

As a response to these backdrops, a programmer under the

pseudonym of Nakamoto introduced Bitcoin, a decentralized medium of exchange in

2009. The peer-to-peer electronic currency shows unique features. It is not

backed by any central authority, has a fixed supply set in advance of 21

million Bitcoins and is created via an innovative technology, Blockchain that

registers transactions and stows them into transparent blocks. These blocks are

completed once these transactions are verified and secured into a distributed

network. Therefore, this creation process is similar to gold mining, which led

to Bitcoin being called the «digital gold».

Following the inception of Bitcoin, many alternative

cryptocurrencies, using the same blockchain technology emerged. Whether

addressing same purposes as Bitcoin or providing innovative decentralized

solutions, they attracted investors' attention and gained growing market shares

with the most popular among them being Ethereum, Ripple, Dash, Stellar and

Litecoin.

Driven by high capital inflows, Cryptocurrencies witnessed

price rise in tandem. Market capitalization and volume traded continued growing

exponentially until the end of 2017, when Bitcoin realized its meteoric rise

before topping out in the following months.

This rapid surge in prices and the high volatility displayed

by the cryptocurrency market has attracted mostly speculators seeing

Cryptocurrencies as a speculative asset rather than a currency store of value.

Consequently, many investors question whether cryptocurrencies are just

fictitious currencies forming speculation bubbles or a valuable opportunity

investment.

The main purpose of this study is to explore Cryptocurrencies

as a new alternative investment.

The research is conducted from the perspective of a global

investor who considers diversification as of paramount importance. Considering

the excessive volatility encompassing

3

cryptocurrencies, I restrain cryptocurrencies to hedging and

diversification uses only. According to Baur and Lucey (2010), a hedge is an

asset that shows adverse correlation to another asset, whereas a diversifier

exhibits marginal positive price co-movements with the other asset.

Furthermore, this study sheds light on the use of the cryptocurrencies as

performance enhancers in a global portfolio while previous research focused

only on Bitcoin. I benchmark the cryptocurrency market with Bitcoin and three

major alternative cryptocurrencies: Ripple, Dash and Litecoin. Whilst among

traditional assets I consider stocks, bonds, real estate and gold.

In order to investigate the diversification and hedging traits

of the aforementioned cryptocurrencies and capture the co-movement between each

cryptocurrency and the traditional assets, I consider the multivariate dynamic

conditional correlation GARCH model of Engle (2002). The results offer

compelling evidence of cryptocurrencies as effective diversifiers, yet they

exhibit weak hedging properties. I find that Bitcoin acts as a strong hedge

only against price movements of Chinese equities, global real estate and

corporate bonds. Additionally, Litecoin qualifies as a hedge for global real

estate and Japanese equities. Whereas Dash is only a good hedge against global

bonds. Ripple, on the other side, does not possess any hedging properties since

it exhibits moderately positive correlation with all traditional assets.

I further examine the diversification perquisites of

cryptocurrencies in a portfolio comprising all traditional asset classes.

Bruder and Roncalli (2012) argue that risk aversion of institutional and

individual investors increased significantly after the 2008 financial crisis.

Thus, they prompt the use of investment strategies based on risk budgeting and

diversification instead of return forecasting ones.

Regarding this matter and the high volatility nature of

Cryptocurrencies, this study adopts four optimization frameworks that focus on

measuring risk: traditional minimum variance, minimum conditional value at

risk, inverse volatility and maximum diversification.

4

The out-of-sample performance of the optimal portfolios is

studied on a risk adjusted return basis. The back-testing results confirm the

evidence of cryptocurrencies being outstanding diversifiers. Regardless of the

strategy, I find that adding cryptocurrencies to the basic portfolio, the risk

return ratio increases significantly albeit at different magnitudes. On the

other side, the downside risk of the portfolio increases especially when

alternative tokens are included. Interestingly, Bitcoin succeeds to reduce the

downside risk under minimum variance and inverse volatility.

The research paper is structured as follow: Section 2 presents

the literature review, section 3 undergoes the methodology details, section 4

introduces the data, section 5 reports empirical results and robustness check

and section 6 provides conclusion.

2. Literature review

Despite the global financial instability, the strong past

financial performance of bitcoin (BTC) made it comparable to a digital gold.

Therefore, a strand of studies examined Bitcoin and its properties as an asset

class. Yermack et al. (2013) compare BTC's daily exchange rates with gold and

fiat currencies and argue that BTC is more comparable to a speculative

investment. Baur et al. (2015) investigate statistical properties and future

usage of bitcoin. They suggest that bitcoin is a hybrid between conventional

currencies and commodity currency. Dyhrberg et al. (2015) find similarities of

BTC with gold and USD and confirm the views of Baur et al. (2015). Ciaian,

Rajcaniova and Kancs (2016) go a step further and analyze the impact of BTC's

supply and demand on its price formation. Thus, they discover similar price

formation patterns with other currencies.

Whether considered as a medium of exchange or a highly

speculative asset, BTC's skyrocketing returns are the main reason of its

attractiveness. After being accepted as a method of payment, its use as a

financial investment vehicle has been thoroughly examined. In point of fact, a

broad

5

range of literature studied whether including bitcoin in a

traditional portfolio can enhance its return and reduce the risk.

Brière et al. (2015), using mean variance spanning

test, assert BTC's diversification benefits in an investment portfolio. They

conclude that BTC's low correlation with other assets enhances the portfolio's

performance and compensates for the increase in the overall risk. As returns of

BTC exhibit high kurtosis and low skewness, Eisl et al. (2015), proposes the

use of a CVaR framework as an alternative to mean variance analysis. Their

findings are in line with the ones of Brière et al. (2015). Indeed,

investing a small fraction in BTC enhances intensely the portfolio's risk

return tradeoff.

Kihoon Hang (2016), performs a trading strategy based on

momentum (TSMOM). By conducting a mean variance analysis, he demonstrates that

enhanced returns and reduced volatility can be achieved in a portfolio of

equities and TSMOM.

Diversification and hedging are characteristics of huge

importance when building a portfolio. Therefore, an investigation of

correlation between BTC and other financial assets is crucial. Following this,

Bouri et al. (2017), employed a dynamic conditional correlation model (Engle,

2002) to estimate correlation between BTC and other financial assets. They find

that Bitcoin does qualify as an effective diversifier. However, it can only

serve as a hedge or safe haven in few cases. On the contrary, Bouoiyour and

Selmi (2017), vindicate the hedge and safe haven role of bitcoin against oil

price movements. Moreover, by adding Bitcoin to a portfolio of oil only, they

observe an enhancement in performance and downside risk reduction.

Guesmi et al. (2018), consider DCC GJR GARCH as the suitable

model for modeling joint dynamics of different financial assets. They document

that Bitcoin can be a systematic hedge and that adding a small fraction of

bitcoin reduces considerably the portfolio's risk exposure.

6

They also stress that a short position in Bitcoin hedges the

risk for commodities, stocks and currencies.

Due to the high trading and predominant mining activity in

China, Kajtazi and Moro (2017), raise the question of whether BTC adds value in

a Chinese asset-based portfolio. They show significant but low correlation with

Chinese assets and argue that Bitcoin fails in enhancing portfolio's

performance over all periods.

Evidence that Bitcoin offers diversification benefits in a

traditional portfolio is abundant in literature and so far, research towards

altcoins remains infrequent.

Aiming to close this gap, Osterrieder et al. (2016), were

amongst the first to explore the interdependences between cryptocurrencies

(CCs). They demonstrate that low mildly correlation exist between most CCs

except for the ones sharing the same technology. Following this, Braineis and

Mestel (2018), expand the research by exploring the effects of diversified

cryptocurrency investments. Their empirical results show that adding several

CCs expands the efficient frontier of a bitcoin-based portfolio.

Further investigating the diversification effect, Chuen et al.

(2017), advocate the use of the CRIX index, which was developed by Trimborn and

Hardle (2016) to mimic the CCs market performance. When looking at static and

dynamic correlations between CRIX and traditional assets, they give evidence of

diversification benefits. However, the mean-variance spanning tests reveal

enhancement of global minimum variance only. In fact, the negative skewness of

CRIX and high risk makes it redundant in a tangency portfolio.

Klein et al. (2018), argue that Bitcoin is not the new gold.

According to their research results, Bitcoin is only suitable for

diversification benefits and does not display stable hedging

7

capabilities. Meanwhile, they find CRIX to display better

hedging effects. Yet, it still fails to be an effective hedge like gold.

3. Data

To conduct the analysis, I retrieve data from two different

sources. I retrieve daily closing prices for traditional assets in form of

indices from DataStream. While the data for cryptocurrencies are extracted from

coinmarketcap.

According to Abidin et Al. (2004), international

diversification is proven to yield higher returns and reduce risks and since

cryptocurrencies are global in nature, I decide to adopt the perspective of a

global investor. Therefore, I create a well-diversified international portfolio

composed of cryptocurrencies and traditional assets.

Emphasis lies on the largest cryptocurrency assets. Therefore,

I select four cryptocurrencies from the ten largest cryptocurrencies by market

capitalization. Bitcoin and three major alternative cryptocurrencies: Litecoin,

Ripple and Dash. These cryptocurrencies are portrayed as more suitable than

other major altcoins like Bitcoin cash and Ethereum, which were only introduced

in 2015 and 2017, respectively, and would not provide enough set of data to

conduct the research. Additionally, the selection is made based on the

underlying correlation of the alternative cryptocurrencies with Bitcoin. Ripple

and Dash are moderately correlated with Bitcoin while Litecoin is relatively

highly correlated with the latter.

Traditional and alternative assets comprise equity, fixed

income, real estate and gold. Each asset class is embodied by liquid financial

indices.

Equity indices are selected based on the four most important

markets of cryptocurrencies trading. I use four regional indices S&P 500,

Euro Stoxx 50, Nikkei 225, SSE (Shanghai Stock Exchange) as well as MSCI

Emerging Markets Index. Considering the global bond universe of fixed income, I

adopt the following indices: S&P Global Developed Sovereign Bond Index

and

8

IBOXX Liquid Investment Corporate Grade Index. Gold is added in

consonance with Dyhrberg et al. (2015) since the latter is typically depicted

as hedge. As of real estate, I use as a reference FTSE EPRA NAREIT global.

The sample contains daily price information from 30 July 2014 to

31 April 2019. I remove the daily data of cryptocurrencies during the weekends

in order to match the number of observations with traditional assets.

Furthermore, I compute daily log returns since they are deemed

more convenient for time series analysis and provide a better fit for

statistical models. Therefore, daily log returns are obtained using the

following formula:

Pi,t

rit = log Pi,t-1

4. Methodology

Modern portfolio theory states that correlation is the basis

of diversification in a portfolio. Accordingly, investing in low correlated or

negatively correlated assets can achieve efficient diversification (Bodie et

Al, 2014). Following this, I examine diversification capabilities of

cryptocurrencies as well as their ability to enhance the risk-return reward of

a global investor.

4.1. Correlation analysis

I perform a correlation analysis in order to assess if

cryptocurrencies can be a diversifier or a hedge. At first, I estimate

correlation coefficients of cryptocurrencies and other assets via a pairwise

correlation. However, the latter is only the average estimation and correlation

in general is known to display time varying properties.

Hence, I conduct the multivariate dynamic conditional

correlation (DCC) model by Engle (2002). The advantage of the model lies in its

limited number of estimated parameters, univariate GARCH flexibility and its

direct parameterization of conditional correlation.

9

The estimation of the DCC model is performed in three steps:

I estimate an ARMA (1, 1)2 mean equation to model the

conditional mean and deal with the autocorrelation in the time series

returns.

The conditional mean equation for each asset is presented in the

equation below:

?? ??

???? = ?? + E??+ ? ????????-?? + ? ???? E??-??

??=1 ??=1

Where c is a constant term, E?? is the white noise, p is the

autoregressive term, q the moving average term and ö, è are the

model parameters.

After deeming the conditional mean for each asset, the ARMA

residuals are used to estimate the GARCH (1, 1) variance model.

Therefore, conditional variances are implemented one by one using

the following formula:

????2= ??+ ?? E??2 +

??????-1

2

Where ??t is the conditional variance, ?? is the

intercept, ?? is the coefficient displaying the impact of previous shocks,

E??2 is the squared residual and ?? is a coefficient that transmits

the GARCH (1, 1) effect.

Afterward, I model conditional covariance of standardized returns

using computed variances from first step.

With ????,??,??+1 = ????????(????+1

?? , ????+1

?? ) and ????,?? = ??

1-??-??

The dynamic conditional correlation is computed as follows:

??

????,??,??+1 = ????,?? + ?? (????+1??????+1- ??????) +

?? (????,??,?? - ??????)

2 Autoregressive moving average (1,1) model

10

Once the auxiliary variable gi,j,t+i is forecasted, I compute the

dynamic conditional correlation

|

as follows:

|

Pi,j,t+i =

|

gi,j,t+i

.gi,i,t+i.gj,j,t+i

|

After studying the co-movement between the selected asset

classes and cryptocurrencies, I investigate the usefulness of cryptocurrencies

as a diversification tool from a portfolio perspective.

4.2. Portfolio optimization

I start by constructing a portfolio without cryptocurrencies,

which will be referred to as the basis portfolio. Furthermore, I investigate

the options of including cryptocurrencies to the traditional assets' portfolio.

I construct two sets of portfolios. The first portfolio includes traditional

assets and only Bitcoin and the second one includes traditional assets and the

four cryptocurrencies. The benefits of adding cryptocurrencies are assessed in

terms of risk-return profiles, cumulative wealth and downside risk.

In order to calculate these performance metrics, I use the

out-of-sample backtesting method, which evaluates trading strategies using

historical data. The models' parameters are assessed via a rolling window

approach under the following steps: I use the 200 last days observations before

the rebalancing date for the parameters' estimation. Then, the resulting

weights are rebalanced on a monthly basis for the whole out of sample

period.

Thus, the optimized weights are subject to different

parameters depending on the optimization frameworks presented below.

11

4.2.1. Minimum risk approaches

Minimum variance portfolio is the Markowitz least variance

framework. It is set out as the portfolio that maximizes the use of

diversification to achieve the lowest risk. The portfolio weights are optimized

for each point in time using the subsequent formula:

min 6P = En1 Ey 1 wiw1611 s. t.

wl >_ 0, En1 wl = 1 Where weights are estimated by using

the historical variance and covariance matrix.

Nevertheless, a strong shortcoming of the mean variance

analysis is the assumption of normal distribution of returns. In this context,

cryptocurrencies' excess volatility infers a heavy tail distribution as already

stated by Eisl et al. (2015) and Chuen et al. (2017).

To cope with this issue, I follow Rockafeller and Uryasev

(2002) to construct the conditional value at risk strategy (CVaR). The strategy

uses the expected shortfall, which is a more coherent risk measure contrasting

to the variance since it aims to quantify only the downside risk. Log returns

are simulated via a T-student distribution.

Therefore, conditional value at risk portfolio weights are

given by solving the following optimization problem:

min CVARa(wt) s. t. up,t(wt) = rtarget

; wt1p = 1 , wl,t » 0 wtERP

1

CVARa(w) = (1 - a) if(w,r)<VARa(w)

f(w,r)p(r)dr

Where f (w, r) is the probability density function of

portfolio returns with weights w, a is the confidence level,

VARa is the loss to be expected in a.100% of the

times.

Short selling is constrained under the two strategies since

Bitcoin futures were only introduced recently on Chicago Board Options Exchange

(CBOE) and Chicago Mercantile Exchange

12

(CME) in December 2017. In addition, I impose a maximum weight

constraint of 50% for each asset in order to omit extreme weight

allocations.

0% < ???? < 50%

4.2.2. Risk budgeting approaches

Requiring only the estimation of volatility, risk budgeting

approaches are becoming a popular solution for risk adverse investors. Booth

and Fama (1992) argue that these models put diversification at the heart of the

investment strategy and are a good alternative to Markowitz least variance

framework when the assumption of normal returns is not solid. Therefore, I

adopt the subsequent risk budgeting approaches:

The inverse of the volatility is used to determine the weight

of each asset. Highly volatile assets will be given a lower weight in

comparison to low volatility assets. Hence, each asset contributes different

amount of risk to the overall portfolio. The optimization problem takes the

following form:

1

|

???? =

|

????????

|

|

? ( 1

?? ??=1 ????????)

|

Introduced by Choueifaty and Cognard (2008) maximum

diversification seeks to maximize the diversification ratio of the weighted

average assets volatilities to the total portfolio volatility. The

diversification ratio is given as:

Maximize DR = ? ????????

??

??=1 s. t. ? ????

?? ??=1 = 1 and ???? = 0

? ????

??

??=1

13

4.3. Performance measurement

In order to measure the portfolios performance, I rely on

Sharpe ratio, which is a performance criteria widely used by practitioners and

in literature.

u,,

=

^ - Rf

o-^,,

Sharpe ratio is defined as follow:

^ SR,,

With û,, the portfolio sample mean returns and

o-^,, its sample standard deviation.

In addition, I compute the cumulative returns and the maximum

drawdown of the investment strategies for each of the optimal portfolios.

5. Empirical results

5.1. Sample Characteristics

Table 1 and table 2 display summary statistics of daily log

returns for cryptocurrencies and traditional assets.

Regarding traditional assets, equity indices exhibit slightly

positive mean returns with S&P 500 showing the highest average daily

returns and the lowest standard deviation. As expected, corporate and

government bonds indices have low mean returns and showcase the lowest standard

deviation among all financial assets. Commodities depicted by S&P GSCI gold

provide the worst reward to volatility with negative mean return and an

annualized Sharpe ratio of -0.04. On the other hand, real estate exhibit

promising performance with a favorable annualized Sharpe ratio of 0.44.

Meanwhile, in line with Chuen et Al. (2017), I find that

cryptocurrencies outperform traditional financial assets in terms of average

daily returns and have the highest standard deviation by far.

14

As can be noticed, the 1% and 99 % percentiles show that

extreme price movements are more severe for cryptocurrencies than for

traditional assets. Albeit, the higher magnitude of positive returns is

emphasized for cryptocurrencies when compared with negative ones.

In the case of skewness and kurtosis, I find Ripple, Dash and

Litecoin to be positively skewed, a significant characteristic rational

investors look for. In contrast, Bitcoin, equities, bonds and real estate

display a negative skewness that indicates a higher tail risk. Additionally, I

find that all-time series are leptokurtic. Eurostoxx 50 and Shanghai stock

exchange present high excess kurtosis but to a lesser extent than altcoins.

Apart from Bitcoin, cryptocurrencies have very high excess

kurtosis as the market for altcoins is still developing.

Therefore, the Jarque-Bera test supports the latter findings

by rejecting the normality for all assets at 1% significance level. All the

conventional assets and cryptocurrencies are not normally distributed.

Moreover, I conduct Ljung box test to check for serial correlation. Hence, I

find most conventional assets as well as Ripple to show significant

autocorrelation. Nevertheless, Bitcoin, Dash, S&P500, Sovereign bonds and

Gold display a low autocorrelation of daily returns, which suggests a lack of

predictability.

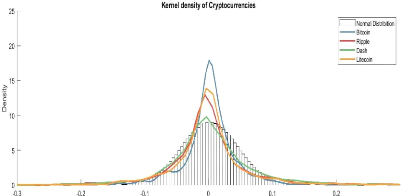

Cryptocurrencies pronounced deviation from normality is

visualized in Figure 1. The black line depicts a theoretical normal

distribution of Bitcoin. I observe that the latter is the least volatile with

more observations around the mean and a less pronounced tail than altcoins.

5.2. Correlation analysis

Accurate correlation assessment is one fundamental aspect in

portfolio theory. According to Corbet et Al. (2018), such important metric has

momentous implications on portfolio construction, diversification and

hedging.

15

Figure 2 illustrates pairwise correlation coefficients, which

give a first snapshot of average correlations between our different financial

assets. It is noteworthy that almost all correlation coefficients between

cryptocurrencies and traditional assets do not exceed 0.10. Regarding

cryptocurrencies, they range from 0.25 to 0.59 with Bitcoin and Litecoin

exhibiting the highest correlation. Relatively, traditional assets have more

varying correlations within themselves due to their global diversification.

Yet, this is only the average correlation for our sample period. That is why I

derive the multi-varying correlation through the Dynamic conditional

correlation model.

Tables 4, 5, 6 and 7 illustrate descriptive statistics of

dynamic conditional correlations between the innovations of each of the

cryptocurrencies and traditional assets. The multi-varying correlation analysis

will allow us to asses precisely the diversification and hedging benefits of

cryptocurrencies.

Table 4 depicts the DCC statistics for correlation pairs

within Bitcoin. The latter displays negative correlation among all the sample

period with the following asset categories: developed corporate bonds, global

real estate and Chinese equities. Hence, it acts as a strong hedge according to

the definition of Baur and Lucey (2010). Moreover, it has a correlation of

approximately zero with gold, MSCI emerging markets and sovereign bonds. It is

also notable that the standard deviation of those correlation pairs is very low

suggesting a stable correlation over time and high diversification benefits.

Regarding developed market equities, Bitcoin is negatively correlated to Nikkei

225 on average with a maximum value of 0.0194.

The highest average correlation from all conventional assets

is the pair with Eurostoxx 50 with a value of 0.0649. Nevertheless, it is very

stable among all the period. For S&P 500, DCC correlation is more dynamic

with a maximum spike of 0.27.

16

Table 5 reveals that Ripple cannot be regarded as a strong

hedge against any of the traditional assets. A further look into the

descriptive statistics of DCC correlations brings to light the noisy

correlation spikes. Moreover, the 25% and 75% quantiles show slightly positive

correlations with traditional assets over the whole sample period.

Table 6 shows that Dash has the highest correlation with

developed market equities within all the cryptocurrencies. Furthermore, dynamic

correlation is unstable for emerging markets equities and alternative

investments since it swings from negative to positive. Yet, it can be

considered as a strong hedge against developed corporate and sovereign bonds

only.

According to table 7, Litecoin possesses hedging capacities

against Japanese equities and global real estate. In addition, Low co-movements

with equity market indices are more persistent than for Ripple and Dash which

suggests better investment opportunities.

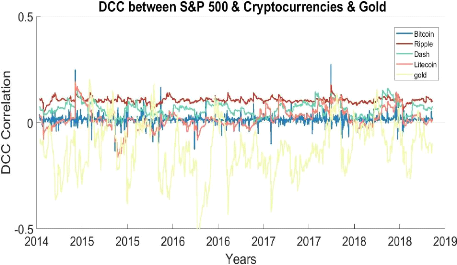

It is apparent that S&P 500 shows unstable dynamic

correlations with cryptocurrencies all over the sample period. For a better

assessment of hedging capacities, figure 2 plots its DCC correlation with

cryptocurrencies as well as gold. The latter is added as a reference point

since it is depicted as a safe haven against S&P 500. (Baur & Mc

Dermott 2016).

Ripple and Dash show mostly positive correlations as already

stated. Meanwhile, Bitcoin and Litecoin exhibit a wide range of positive and

negative correlation values. Albeit, with small periods and no persistence

while being negative. Gold, on the contrary, shows negative dynamic correlation

for successive several months. In this regard, safe haven and strong hedge

attributes should be excluded for Bitcoin and Litecoin. They can only be very

effective diversifiers against S&P 500.

5.3. Portfolio performance

In this section, I discuss the results of the different

optimization frameworks performed for the three optimal portfolios: a portfolio

of traditional assets, a portfolio of traditional assets and

17

Bitcoin and finally, a portfolio of traditional assets,

Bitcoin and the three alternative cryptocurrencies: Ripple, Dash and

Litecoin.

Table 8 reports the performance of the optimal portfolios

under the Minimum Variance optimization. I find that allocating Bitcoin to the

basic portfolio slightly increases the annualized returns. Interestingly, the

volatility of the optimal portfolio remains unchanged and maximum drawdown is

even lower.

Likewise, the inclusion of alternative cryptocurrencies

increases a bit more the returns but at the cost of a slightly higher

volatility and a higher maximum drawdown. In fact, allocating even an

insignificant share into altcoins does not compensate for their very high

volatility. However, the higher returns seem to offset the evident increase in

risk and the risk return reward of 1.26 vindicates the importance of adding

Cryptocurrencies to the basic portfolio.

Due to the fat tail problem of cryptocurrencies, Conditional

Value at Risk emerges as more coherent risk measure than variance. Table 9

presents the performance of Minimum Conditional Value at Risk optimization. It

is important to note that the strategy's ability to focus on the expected

shortfall only brought higher returns for the portfolios with

cryptocurrencies.

When including Bitcoin in the basic portfolio, the strategy

shows a slight increase in the returns from 3.8% to 4.51%. The inclusion of

alternative cryptocurrencies improved more the returns with an annualized mean

of 5.08%. Once again, the high returns of cryptocurrencies offset their excess

volatilities. Despite the increase in standard deviation, annualized Sharpe

ratio increases from 1.05 to 1.17 when adding Bitcoin and to 1.29 when Altcoins

are included.

Skewness and kurtosis of the second and third portfolios are

slightly improved. Cumulative wealth increases as well. However, I observe a

higher maximum drawdown when including Bitcoin and the effect is more prominent

for the third portfolio.

18

Optimal portfolio weights is the main scope of the two

aforementioned risk strategies. Now, I switch to risk budgeting strategies

which impose constraints on the volatility contribution of each asset to the

total portfolio volatility.

Table 10 summarizes the results of the inverse volatility

strategy. I observe that diversification effects of this framework worsen off

the performance of the basic portfolio. In fact, all the indices in the

portfolio have positive weights in spite of their level of risk while the two

first strategies omit weight allocations for the riskiest assets. The basic

portfolio gives mean return of 2.9%, a standard deviation of 5.17% and a Sharpe

ratio of only 0.56. The effect of cryptocurrencies is more prominent here. When

adding Bitcoin, Sharpe ratio increased by 0.28 from 0.56 up to 0.85 that is

driven by a significant improve in returns and an insignificant increase in

volatility of 0.03%. The contribution of alternative cryptocurrencies is even

more significant. Portfolio III displays a risk return efficiency of 1.30 and a

cumulative wealth of 1.30. Contrariwise, maximum drawdown is again higher than

first and second portfolios. Lastly, table 11 illustrates the performance of

the maximum diversification strategy, which aims to maximize diversification

effects by creating a portfolio with minimally correlated assets. Effective

diversification benefits of cryptocurrencies are the most pronounced under this

strategy. In fact, adding cryptocurrencies increases drastically the

performance of the basic portfolio as Sharpe ratio increases from 0.73 to 1.22

with Bitcoin and up to 1.54 when adding Ripple, Dash and Litecoin. The strategy

displays the highest returns for the second and third portfolio as well as the

highest standard deviation. Once more, the skyrocket returns of

cryptocurrencies seem to outweigh their high volatility.

Portfolio III shows higher maximum drawdown of 9.46% and more

leptokurtic returns. However, it is important to pinpoint that this is the only

portfolio to display positive skewness, which means that the probability of

positive returns was higher than negative ones. Moreover, portfolio III hits

the highest level of cumulative wealth with 1$ turning into 1.37$.

19

So far, this study revealed crucial portfolio benefits when

adding cryptocurrencies to a traditional assets' portfolio independently of the

optimization strategy employed.

For further insights, a detailed analysis of portfolios weight

allocation is presented in the following section.

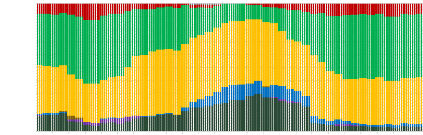

5.4. Portfolio weights analysis

As can be seen from the asset allocation weights graphs,

portfolios of traditional assets under inverse volatility and maximum

diversification strategies are more diversified. On the other hand, Conditional

Value at Risk strategy sets extreme weight allocations to bonds indices

followed by S&P 500 since they exhibit the least volatility. Therefore, the

C-var optimizer omits weighting other indices, which performed really bad and

were highly volatile during estimation periods. This results in the basis

portfolio exhibiting the best performance under this strategy with a Sharpe of

1.07.

When cryptocurrencies are included, I notice that the

weighting scheme of other asset classes fluctuates to compensate for the

additional volatility. Equity indices weights change the most during the sample

period. I observe a significant increase in S&P 500 proportion but also a

small position taken in gold. In addition, through the whole investment period,

optimal portfolios contain between 0 and 3% of cryptocurrencies with the higher

allocation share during the years 2016-2017, the period of tremendous growth

for cryptocurrencies. Indeed, cryptocurrencies are considered too risky for the

parameters of the optimization problem.

It is also noticeable that Bitcoin dominates over alternative

cryptocurrencies. In fact, none of the Altcoins is given more than 1% weight

during the whole optimization process.

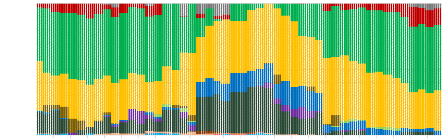

Regarding risk budgeting approaches, I observe that portfolio

assets do not fluctuate that much when adding cryptocurrencies. Moreover, the

weight allocated to cryptocurrencies is larger under those two strategies.

Until 2017, there is an increasing allocation in cryptocurrencies. However, it

decreases drastically after the Bitcoin boom.

20

Furthermore, the Maximum Diversification strategy, which

boosted the performance of investments significantly, invests between 0 and 10%

in cryptocurrencies. Thus, the higher cryptocurrency exposure had a huge impact

on maximizing the portfolio performance.

5.5. Robustness check

To assess the robustness of the trading strategies results,

tables 12, 13, 14 and 15 present performance results using weekly data and

monthly rebalancing.

The results of the study are robust with regard to the asset

allocations employed. I find that cryptocurrencies always add substantial value

when included in the stocks-bonds-alternative investments portfolio. Sharpe

ratio increases significantly under the different optimization frameworks.

However, similar results regarding the downside risk of the basis portfolio are

found when using weekly data. Alternative cryptocurrencies worsen of the

maximum drawdown of the portfolio whereas Bitcoin increases slightly the

maximum drawdown under Inverse volatility and minimum variance strategies.

Interestingly, Minimum conditional value at risk performs

better than maximum diversification and yields the highest Sharpe Ratio when

cryptocurrencies are added.

6. Conclusion

This study seeks to address the possible hedging and

diversification benefits of cryptocurrencies as an alternative investment. From

the perspective of a global investor, I investigate the market linkages between

Cryptocurrencies and global asset indices as well as the benefits of their

inclusion within these assets.

21

Using the dynamic conditional correlation model, I find that

block-chain assets can act as effective diversifiers for the investment period

analyzed. I also detect that the correlation of traditional assets against

Bitcoin are closer to zero and more stable than against over crypto-tokens.

Moreover, I find that Bitcoin, Dash and Litecoin do possess hedging properties

against some assets' indices. However, none of the cryptocurrencies acts as

hedge against European, American and emerging market equities.

The resulting diversification properties further endorse the

cryptocurrencies use case in a diversified portfolio. These findings are useful

for global investors seeking protection from markets downward movements. I

examine the out of sample performance of portfolios with and without

cryptocurrencies via risk-based investment strategies: minimum variance,

minimum conditional value at risk, inverse volatility and maximum

diversification.

The results are in line with previous research regarding the

inclusion of Bitcoin in a global portfolio of equities, bonds and alternative

assets. I find that the risk return efficiency is enhanced under all

strategies. The small increase in volatility was compensated with

proportionally greater returns.

Despite their extreme volatility, the addition of alternative

cryptocurrencies to a global diversified portfolio, which already contains

Bitcoin, enhances the risk return reward. However, these crypto-assets yield

higher volatility and higher maximum drawdown under all strategies. Further,

the performance of the portfolio is boosted significantly under inverse

volatility and maximum diversification. In fact, these modern risk based

strategies prompt higher risk return reward via greater cryptocurrency exposure

and especially greater alternative cryptos exposure. On the other side, due to

their volatility structure, Minimum variance and Minimum C-var strategies

invested in cryptocurrencies and particularly in Bitcoin only in certain points

of time.

22

Moreover, the hedging properties of Cryptocurrencies are

analyzed via the portfolios maximum drawdown. When adding Bitcoin, I find that

it slightly drops under minimum variance and inverse volatility strategy.

However, when Dash, Ripple and Litecoin are further added, the maximum drawdown

increases under the four optimization models.

As robustness checking, I apply the aforementioned allocation

strategies using weekly data. Results persist robustly. Cryptocurrencies

enhance the portfolio performance on risk-adjusted basis but do not really

decrease the portfolio downside risk.

In a nutshell, the study evidence suggests that

cryptocurrencies can act as outstanding diversifier tools on a global

perspective but do not offer appealing hedging properties.

However, the results of this study should be interpreted with

caution. This analysis employs only limited asset allocation strategies. The

sample period is small due to the short history of cryptocurrencies and better

alternative to the selected cryptocurrencies might exist.

23

Appendix:

Table 1: Descriptive statistics of traditional

assets.

Summary statistics of daily log returns for traditional assets

from 31 July 2014 to 30 April 2019. (N=1238 observations). Results are reported

on a percentage basis apart from skewness, kurtosis, Sharpe ratio, the JB and

LJBox tests. In addition, Sharpe ratio is annualized.

|

S&P 500 Eurostoxx 50

|

SSE A

shares

|

Nikkei 225

|

MSCI Markets EM

|

IBOXX LIG

|

S&P GSD

|

FTSE EPRA NAREIT

|

S&P GSCI GOLD

|

|

Mean

|

0.042

|

0.008

|

0.027

|

0.030

|

0.011

|

0.014

|

0.002

|

0.022

|

-0.002

|

|

Standard Deviation

|

0.833

|

1.117

|

1.507

|

1.136

|

0.897

|

0.295

|

0.354

|

0.792

|

0.815

|

|

Skewness

|

-0.448

|

-0.786

|

-1.190

|

-0.261

|

-0.311

|

-0.332

|

-0.002

|

-0.748

|

0.271

|

|

Kurtosis

|

7.068

|

12.335

|

10.063

|

7.079

|

4.721

|

3.926

|

5.312

|

9.167

|

6.036

|

|

Minimum

|

-4.184

|

-11.102

|

-8.869

|

-5.742

|

-5.101

|

-1.451

|

-1.922

|

-6.912

|

-3.418

|

|

1% percentile

|

-2.520

|

-3.037

|

-6.109

|

-3.460

|

-2.330

|

-0.741

|

-0.950

|

-2.271

|

-2.252

|

|

5% quantile

|

-1.427

|

-1.709

|

-2.221

|

-1.791

|

-1.501

|

-0.492

|

-0.580

|

-1.235

|

-1.353

|

|

25% quantile

|

-0.255

|

-0.574

|

-0.473

|

-0.486

|

-0.511

|

-0.157

|

-0.187

|

-0.373

|

-0.404

|

|

Median

|

0.029

|

0.039

|

0.032

|

0.063

|

0.060

|

0.015

|

0.000

|

0.052

|

0.000

|

|

75% percentile

|

0.445

|

0.577

|

0.606

|

0.614

|

0.540

|

0.198

|

0.197

|

0.464

|

0.411

|

|

99% percentile

|

2.103

|

2.925

|

4.183

|

3.003

|

2.172

|

0.685

|

0.939

|

1.977

|

2.176

|

|

Maximim

|

4.842

|

5.567

|

5.599

|

6.414

|

3.228

|

0.938

|

1.802

|

3.622

|

4.590

|

|

Sharpe Ratio

|

0.800

|

0.117

|

0.285

|

0.414

|

0.193

|

0.767

|

0.013

|

0.442

|

-0.044

|

|

Jarque Bera Test

|

894.984

|

4622.047

|

2865.479

|

872.227

|

172.802

|

66.976

|

275.770

|

2077.435

|

490.681

|

|

Ljung Box Test

|

18.779

|

40.143

|

69.939

|

105.296

|

69.638

|

39.657

|

24.314

|

43.257

|

20.791

|

|

Critical Value Jarque Bera Test

|

5.943

|

|

|

|

|

|

|

|

|

Critical Value Ljung Box Test

|

31.400

|

|

|

|

|

|

|

|

24

Table 2: Descriptive statistics of

cryptocurrencies.

Summary statistics of daily log returns for cryptocurrencies from

31 July 2014 to 30 April 2019. (N=1238 observations).

|

Bitcoin

|

Ripple

|

Dash

|

Litecoin

|

|

Mean

|

0.179

|

0.330

|

0.242

|

0.185

|

|

Standard Deviation

|

4.394

|

7.513

|

7.522

|

6.945

|

|

Skewness

|

-0.210

|

2.381

|

0.015

|

1.000

|

|

Kurtosis

|

8.206

|

20.257

|

27.050

|

15.789

|

|

Minimum

|

-23.874

|

-35.328

|

-86.020

|

-51.393

|

|

1% percentile

|

-13.533

|

-18.051

|

-19.343

|

-15.550

|

|

5% quantile

|

-7.056

|

-9.364

|

-9.759

|

-8.994

|

|

25% quantile

|

-1.423

|

-2.430

|

-2.845

|

-2.138

|

|

Median

|

0.222

|

-0.345

|

-0.276

|

0.000

|

|

75% percentile

|

1.890

|

2.089

|

2.990

|

1.822

|

|

99% percentile

|

13.828

|

27.293

|

23.589

|

26.831

|

|

Maximim

|

22.512

|

75.083

|

76.818

|

53.980

|

|

Sharpe Ratio

|

0.645

|

0.698

|

0.511

|

0.422

|

|

Jarque Bera Test

|

1406.84

|

16530.00

|

29834.76

|

8643.49

|

|

Ljung Box Test

|

31.76

|

91.30

|

26.56

|

36.60

|

|

Critical Value Jarque Bera Test

|

|

5.94

|

|

|

|

Critical Value Ljung Box Test

|

|

31.40

|

|

|

25

Table 3: Correlation matrix

This table shows unconditional pairwise correlation coefficients

between cryptocurrencies and traditional assets from 31 July 2014 to 30 April

2019.

|

Bitcoin

|

Ripple

|

Dash

|

Litecoin

|

S&P500

|

Eurostoxx

50

|

SSE A

Shares

|

Nikkei

225

|

MSCI

EM

|

IBOXX

LIG

|

S&P

GSD

|

FTSE

EPRA

|

S&P

GSCI

GOLD

|

|

Bitcoin

|

1.000

|

0.330

|

0.485

|

0.592

|

0.039

|

0.036

|

0.012

|

-0.037

|

0.016

|

-0.023

|

0.010

|

-0.019

|

0.023

|

|

Ripple

|

|

1.000

|

0.254

|

0.332

|

0.053

|

0.030

|

-0.007

|

0.020

|

0.063

|

0.035

|

0.033

|

0.010

|

0.026

|

|

Dash

|

|

|

1.000

|

0.431

|

0.080

|

0.068

|

0.030

|

-0.013

|

0.049

|

-0.073

|

-0.037

|

-0.017

|

-0.006

|

|

Litecoin

|

|

|

|

1.000

|

0.026

|

0.004

|

-0.015

|

-0.026

|

0.007

|

-0.006

|

0.009

|

-0.015

|

-0.016

|

|

S&P500

|

|

|

|

|

1.000

|

0.493

|

0.162

|

0.065

|

0.441

|

-0.193

|

-0.214

|

0.515

|

-0.138

|

|

Eurostoxx 50

|

|

|

|

|

|

1.000

|

0.127

|

0.160

|

0.578

|

-0.125

|

-0.026

|

0.256

|

-0.099

|

|

SSE A Shares

|

|

|

|

|

|

|

1.000

|

0.211

|

0.413

|

0.013

|

-0.101

|

0.230

|

-0.058

|

|

Nikkei 225

|

|

|

|

|

|

|

|

1.000

|

0.416

|

0.203

|

0.124

|

0.181

|

0.102

|

|

MSCI EM

|

|

|

|

|

|

|

|

|

1.000

|

0.022

|

-0.032

|

0.435

|

0.018

|

|

IBOXX LIG

|

|

|

|

|

|

|

|

|

|

1.000

|

0.446

|

0.108

|

0.280

|

|

S&P GSD

|

|

|

|

|

|

|

|

|

|

|

1.000

|

-0.373

|

0.558

|

|

FTSE EPRA

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

NAREIT

|

|

|

|

|

|

|

|

|

|

|

|

1.000

|

-0.177

|

|

S&P GSCI

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

GOLD

|

|

|

|

|

|

|

|

|

|

|

|

|

1.000

|

26

Figure 1 : Density of

Cryptocurrencies.

The following figure illustrates Gaussian kernel density

estimators of cryptocurrencies against fitted normal distribution.

The subsequent tables summarize the dynamic conditional

correlations between daily returns of the four cryptocurrencies and traditional

asset class. Standard deviations are expressed in percentage.

Table 4: DCC statistics for traditional assets against

Bitcoin

|

Mean

|

Std.deviation

|

Minimum

|

Median

|

Maximum

|

25%

quantile

|

75% quantile

|

|

S&P 500

|

0.0146

|

2.2501%

|

-0.1343

|

0.0147

|

0.2738

|

0.0099

|

0.0194

|

|

Eurostoxx 50

|

0.0648

|

0.0022%

|

0.0648

|

0.0648

|

0.0649

|

0.0648

|

0.0648

|

|

SSE_A shares

|

-0.0056

|

0.0038%

|

-0.0061

|

-0.0056

|

-0.0052

|

-0.0056

|

-0.0056

|

|

Nikkei 225

|

-0.0374

|

3.2494%

|

-0.0977

|

-0.0317

|

0.0194

|

-0.0693

|

-0.0102

|

|

MSCI EM

|

0.0196

|

0.0002%

|

0.0196

|

0.0196

|

0.0196

|

0.0196

|

0.0196

|

|

IBOXX LIG

|

-0.0149

|

0.0002%

|

-0.0150

|

-0.0149

|

-0.0149

|

-0.0149

|

-0.0149

|

|

S&P GSD

|

0.0112

|

0.2561%

|

-0.0252

|

0.0112

|

0.0243

|

0.0106

|

0.0118

|

|

FTSE EPRA

|

|

|

|

|

|

|

|

|

NAREIT

|

-0.0320

|

0.2980%

|

-0.0541

|

-0.0321

|

-0.0029

|

-0.0331

|

-0.0310

|

|

S&P GSCI gold

|

0.0166

|

0.0002%

|

0.0165

|

0.0166

|

0.0166

|

0.0166

|

0.0166

|

27

Table 5: DCC statistics for traditional assets against

Ripple

|

Mean

|

Std.deviation

|

Minimum

|

Median

|

Maximum

|

25% quantile

|

75% quantile

|

|

S&P 500

|

0.064

|

3.12%

|

-0.009

|

0.064

|

0.173

|

0.040

|

0.082

|

|

Eurostoxx 50

|

0.044

|

0.00%

|

0.044

|

0.044

|

0.044

|

0.044

|

0.044

|

|

SSE_A shares

|

0.004

|

7.65%

|

-0.255

|

-0.002

|

0.337

|

-0.040

|

0.048

|

|

Nikkei 225

|

0.013

|

2.13%

|

-0.049

|

0.011

|

0.094

|

0.000

|

0.025

|

|

MSCI EM

|

0.073

|

2.56%

|

-0.010

|

0.071

|

0.200

|

0.059

|

0.084

|

|

IBOXX LIG

|

0.018

|

0.13%

|

0.007

|

0.018

|

0.026

|

0.018

|

0.018

|

|

S&P GSD

|

0.034

|

0.00%

|

0.034

|

0.034

|

0.034

|

0.034

|

0.034

|

|

FTSE EPRA

|

|

|

|

|

|

|

|

|

NAREIT

|

0.020

|

4.48%

|

-0.312

|

0.019

|

0.338

|

0.002

|

0.037

|

|

S&P GSCI gold

|

0.026

|

0.00%

|

0.026

|

0.026

|

0.026

|

0.026

|

0.026

|

Table 6: DCC statistics for traditional assets against

DASH.

|

Mean

|

Std.deviation

|

Minimum

|

Median

|

Maximum 25% quantile 75% quantile

|

|

S&P 500

|

0.11

|

1.4%

|

0.03

|

0.10

|

0.18

|

0.10

|

0.11

|

|

Eurostoxx 50

|

0.10

|

3.1%

|

-0.08

|

0.10

|

0.27

|

0.09

|

0.11

|

|

SSE_A shares

|

0.04

|

0.0%

|

0.04

|

0.04

|

0.04

|

0.04

|

0.04

|

|

Nikkei 225

|

0.02

|

0.7%

|

-0.03

|

0.02

|

0.11

|

0.02

|

0.03

|

|

MSCI EM

|

0.08

|

2.5%

|

0.00

|

0.08

|

0.18

|

0.07

|

0.10

|

|

IBOXX LIG

|

-0.07

|

0.0%

|

-0.07

|

-0.07

|

-0.07

|

-0.07

|

-0.07

|

|

S&P GSD

|

-0.04

|

0.0%

|

-0.04

|

-0.04

|

-0.04

|

-0.04

|

-0.04

|

|

FTSE EPRA

|

|

|

|

|

|

|

|

|

NAREIT

|

-0.01

|

8.2%

|

-0.45

|

-0.01

|

0.49

|

-0.05

|

0.03

|

|

S&P GSCI gold

|

-0.02

|

2.1%

|

-0.26

|

-0.02

|

0.10

|

-0.02

|

-0.01

|

28

Table 7: DCC statistics for traditional assets against

Litecoin

|

Mean

|

Std.deviation Minimum

|

Median

|

Maximum

|

25% quantile 75% quantile

|

|

S&P 500

|

0.018

|

4.89%

|

-0.164

|

0.011

|

0.192

|

-0.010

|

0.040

|

|

Eurostoxx 50

|

0.035

|

1.88%

|

-0.036

|

0.035

|

0.120

|

0.027

|

0.043

|

|

SSE_A shares

|

-0.027

|

2.90%

|

-0.099

|

-0.029

|

0.042

|

-0.044

|

-0.014

|

|

Nikkei 225

|

-0.021

|

0.00%

|

-0.021

|

-0.021

|

-0.021

|

-0.021

|

-0.021

|

|

MSCI EM

|

0.020

|

2.47%

|

-0.086

|

0.020

|

0.110

|

0.006

|

0.033

|

|

IBOXX LIG

|

-0.010

|

4.31%

|

-0.129

|

-0.009

|

0.181

|

-0.031

|

0.012

|

|

S&P GSD

|

0.001

|

0.00%

|

0.001

|

0.001

|

0.001

|

0.001

|

0.001

|

|

FTSE EPRA

|

|

|

|

|

|

|

|

|

NAREIT

|

-0.016

|

0.00%

|

-0.017

|

-0.016

|

-0.016

|

-0.016

|

-0.016

|

|

S&P GSCI gold

|

-0.016

|

5.46%

|

-0.207

|

-0.009

|

0.154

|

-0.046

|

0.018

|

Figure 2 : Dynamic conditional correlation plot of

S&P 500 against cryptocurrencies and gold.

29

The following tables present the performance of the three

optimal portfolios: Portfolio I: a portfolio of traditional assets, which

encompasses equities, bonds and alternative investments. Portfolio II: a

portfolio of traditional assets and Bitcoin. Portfolio III: a portfolio of

traditional assets, Bitcoin and alternative cryptocurrencies. Four different

optimization frameworks are performed subsequently: Minimum variance, Minimum

Conditional Value at Risk, Inverse Volatility and Maximum Diversification

frameworks. I use a 200 days moving window and the out of sample period ranges

from May-08-2015 to April-30-2019. Sharpe ratio, mean daily return and standard

deviation are annualized.

|

Table 8: Minimum Variance strategy

|

|

|

Portfolio I

|

Portfolio II

|

Portfolio III

|

|

Mean (%)

|

3.81%

|

4.14%

|

4.60%

|

|

Standard deviation (%)

|

3.62%

|

3.62%

|

3.64%

|

|

Skewness

|

-0.45

|

-0.44

|

-0.43

|

|

Kurtosis

|

5.30

|

5.24

|

5.06

|

|

Maximum drawdown (%)

|

5.43%

|

5.37%

|

5.45%

|

|

Cumulative wealth

|

1.16

|

1.17

|

1.19

|

|

Sharpe ratio

|

1.05

|

1.14

|

1.26

|

Table 9: Minimum conditional value at risk

strategy

|

Portfolio I

|

Portfolio II

|

Portfolio III

|

|

Mean (%)

|

3.80%

|

4.51%

|

5.08%

|

|

Standard deviation (%)

|

3.64%

|

3.85%

|

3.94%

|

|

Skewness

|

-0.41

|

-0.36

|

-0.37

|

|

Kurtosis

|

5.25

|

5.13

|

5.09

|

|

Maximum drawdown (%)

|

5.50%

|

5.70%

|

6.93%

|

|

Cumulative wealth

|

1.16

|

1.19

|

1.21

|

|

Sharpe ratio

|

1.04

|

1.17

|

1.29

|

30

|

Table 10 : Inverse volatility strategy.

|

|

|

Portfolio I

|

Portfolio II

|

Portfolio III

|

|

Mean (%)

|

2.91%

|

4.42%

|

7.67%

|

|

Standard deviation (%)

|

5.17%

|

5.20%

|

5.88%

|

|

Skewness

|

-0.39

|

-0.46

|

-0.45

|

|

Kurtosis

|

5.35

|

5.53

|

5.57

|

|

Maximum drawdown (%)

|

11.85%

|

10.39%

|

11.70%

|

|

Cumulative wealth

|

1.12

|

1.18

|

1.32

|

|

Sharpe ratio

|

0.56

|

0.85

|

1.30

|

Table 11 : Maximum diversification

strategy.

|

Portfolio I

|

Portfolio II

|

Portfolio III

|

|

Mean (%)

|

3.31%

|

5.94%

|

8.75%

|

|

Standard deviation (%)

|

4.50%

|

4.86%

|

5.65%

|

|

Skewness

|

-0.37

|

-0.31

|

0.07

|

|

Kurtosis

|

5.08

|

4.91

|

7.09

|

|

Maximum drawdown (%)

|

8.15%

|

9.40%

|

9.46%

|

|

Cumulative wealth

|

1.13

|

1.24

|

1.36

|

|

Sharpe ratio

|

0.73

|

1.22

|

1.54

|

FIGURES: Weight Allocation

The following graphs display the weight allocation for

traditional assets and cryptocurrencies from 8 May 2015 until 30 April 2019

under the following strategies: minimum conditional value at risk, inverse

volatility, and maximum diversification.

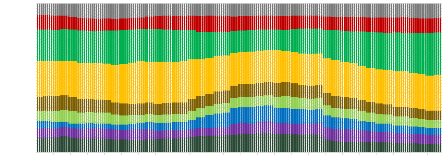

Minimum Conditional Value at Risk

Portfolio of traditional

assets

08.05.2015 08.07.2015 08.09.2015 08.11.2015 08.01.2016 08.03.2016

08.05.2016 08.07.2016 08.09.2016 08.11.2016 08.01.2017 08.03.2017 08.05.2017

08.07.2017 08.09.2017 08.11.2017 08.01.2018 08.03.2018 08.05.2018 08.07.2018

08.09.2018 08.11.2018 08.01.2019 08.03.2019

1,00

0,90

0,80

0,70

Weights

0,60

0,50

0,40

0,30

0,20

0,10

0,00

Year

S&P 500 Eurostoxx 50 SSE A Shares Nikkei 225 MSCI EM

IBOXX LIG S&P GSD FTSE EPRA NAREIT S&P GSCI GOLD

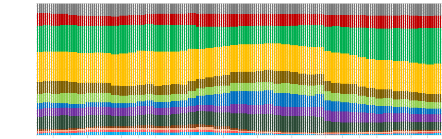

Minimum Conditional Value at Risk Portfolio of tradtional assets

and cryptocurrencies

08.05.2015 08.07.2015 08.09.2015 08.11.2015 08.01.2016 08.03.2016

08.05.2016 08.07.2016 08.09.2016 08.11.2016 08.01.2017 08.03.2017 08.05.2017

08.07.2017 08.09.2017 08.11.2017 08.01.2018 08.03.2018 08.05.2018 08.07.2018

08.09.2018 08.11.2018 08.01.2019 08.03.2019

1,00

0,90

0,80

0,70

Weights

0,60

0,50

0,40

0,30

0,20

0,10

0,00

31

Year

Bitcoin Ripple Dash Litecoin S&P500

Eurostoxx 50 SSE A Shares Nikkei 225 MSCI EM IBOXX LIG

S&P GSD FTSE EPRA NAREIT S&P GSCI GOLD

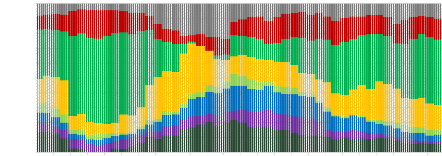

Inverse Volatility

Portfolio of traditional assets

08.05.2015 08.07.2015 08.09.2015 08.11.2015 08.01.2016 08.03.2016

08.05.2016 08.07.2016 08.09.2016 08.11.2016 08.01.2017 08.03.2017 08.05.2017

08.07.2017 08.09.2017 08.11.2017 08.01.2018 08.03.2018 08.05.2018 08.07.2018

08.09.2018 08.11.2018 08.01.2019 08.03.2019

1,00

0,90

0,80

0,70

Weights

0,60

0,50

0,40

0,30

0,20

0,10

0,00

Year

S&P 500 Eurostoxx 50 SSE A Shares Nikkei 225 MSCI EM

IBOXX LIG S&P GSD FTSE EPRA NAREIT S&P GSCI GOLD

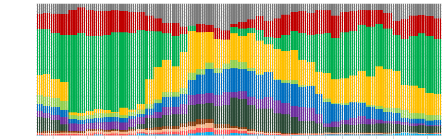

Inverse Volatility

Portfolio of traditional assets and

cryptocurrencies

08.05.2015 08.07.2015 08.09.2015 08.11.2015 08.01.2016 08.03.2016

08.05.2016 08.07.2016 08.09.2016 08.11.2016 08.01.2017 08.03.2017 08.05.2017

08.07.2017 08.09.2017 08.11.2017 08.01.2018 08.03.2018 08.05.2018 08.07.2018

08.09.2018 08.11.2018 08.01.2019 08.03.2019

1,00

0,90

0,80

0,70

Weights

0,60

0,50

0,40

0,30

0,20

0,10

0,00

32

Year

Bitcoin Ripple Dash Litecoin S&P500

Eurostoxx 50 SSE A Shares Nikkei 225 MSCI EM IBOXX LIG

S&P GSD FTSE EPRA NAREIT S&P GSCI GOLD

Maximum Diversification

Portfolio of traditional

assets

08.05.2015 08.07.2015 08.09.2015 08.11.2015 08.01.2016 08.03.2016

08.05.2016 08.07.2016 08.09.2016 08.11.2016 08.01.2017 08.03.2017 08.05.2017

08.07.2017 08.09.2017 08.11.2017 08.01.2018 08.03.2018 08.05.2018 08.07.2018

08.09.2018 08.11.2018 08.01.2019 08.03.2019

1,00

0,90

0,80

0,70

Weights

0,60

0,50

0,40

0,30

0,20

0,10

0,00

Year

S&P 500 Eurostoxx 50 SSE A shares Nikkei 225 MSCI EM

IBOXX LIG S&P GSD FTSE EPRA NAREIT S&P GSCI GOLD

Maximum Diversification

Portfolio of traditional assets and

crytocurrencies

08.05.2015 08.07.2015 08.09.2015 08.11.2015 08.01.2016 08.03.2016

08.05.2016 08.07.2016 08.09.2016 08.11.2016 08.01.2017 08.03.2017 08.05.2017

08.07.2017 08.09.2017 08.11.2017 08.01.2018 08.03.2018 08.05.2018 08.07.2018

08.09.2018 08.11.2018 08.01.2019 08.03.2019

1,00

0,90

0,80

0,70

Weights

0,60

0,50

0,40

0,30

0,20

0,10

0,00

33

Year

Bitcoin Ripple Dash Litecoin S&P500

Eurostoxx 50 SSE A Shares Nikkei 225 MSCI EM IBOXX LIG

S&P GSD FTSE EPRA NAREIT S&P GSCI GOLD

34

The subsequent tables present the results obtained from the

robustness check. It reports the performance of the optimal portfolios when

using weekly data. I use 40 weeks (Equivalent of 200 trading days) moving

window and the out of sample period ranges from May-08-2015 to April-30-2019.

Sharpe ratio, mean daily return and standard deviation are annualized.

|

Table 12: Minimum variance strategy

|

|

|

Portfolio I

|

Portfolio II

|

Portfolio III

|

|

Mean (%)

|

3.38%

|

4.08%

|

5.64%

|

|

Standard deviation (%)

|

4.29%

|

4.31%

|

4.53%

|

|

Skewness

|

-1.17

|

-1.26

|

-1.01

|

|

Kurtosis

|

10.07

|

10.31

|

8.93

|

|

Maximum drawdown (%)

|

6.97%

|

6.50%

|

7%

|

|

Cumulative wealth

|

1.13

|

1.16

|

1.22

|

|

Sharpe ratio

|

0.79

|

0.95

|

1.24

|

Table 13: Minimum conditional value at risk

strategy

|

Portfolio I

|

Portfolio II

|

Portfolio III

|

|

Mean (%)

|

3.30%

|

4.36%

|

10.40%

|

|

Standard deviation (%)

|

4.45%

|

5.15%

|

6.07%

|

|

Skewness

|

-1.30

|

-2.54

|

-1.53

|

|

Kurtosis

|

14.30

|

21.90

|

14.09

|

|

Maximum drawdown (%)

|

7.00%

|

8.74%

|

9.00%

|

|

Cumulative wealth

|

1.14

|

1.17

|

1.39

|

|

Sharpe ratio

|

0.74

|

0.85

|

1.60

|

35

|

Table 14: Inverse volatility strategy

|

|

|

Portfolio I

|

Portfolio II

|

Portfolio III

|

|

Mean (%)

|

3.00%

|

4.59%

|

8.16%

|

|

Standard deviation (%)

|

6.15%

|

6.23%

|

6.85%

|

|

Skewness

|

-0.78

|

-0.83

|

-0.66

|

|

Kurtosis

|

5.75

|

5.81

|

4.73

|

|

Maximum drawdown (%)

|

10.83%

|

9.83%

|

11.0%

|

|

Cumulative wealth

|

1.11

|

1.18

|

1.32

|

|

Sharpe ratio

|

0.49

|

0.74

|

1.19

|

|

Table 15: Maximum diversification strategy

|

|

|

Portfolio I

|

Portfolio II

|

Portfolio III

|

|

Mean (%)

|

3.11%

|

6.55%

|

11.64%

|

|

Standard deviation (%)

|

5.76%

|

6.52%

|

8.83%

|

|

Skewness

|

-1.24

|

-1.20

|

0.36

|

|

Kurtosis

|

9.39

|

8.25

|

7.40

|

|

Maximum drawdown (%)

|

8.69%

|

10.02%

|

9.57%

|

|

Cumulative wealth

|

1.12

|

1.26

|

1.45

|

|

Sharpe ratio

|

0.54

|

1.00

|

1.31

|

36

Salma Ouali

References

Bouri, E., Molnár, P., Azzi, G., Roubaud, D., Hagfors,

L.I., 2017. On the hedge and safe haven properties of Bitcoin: Is it really

more than a diversifier? Finance Research Letters 20, 192-198.

Briere, M., Oosterlinck, K., Szafrz, A., 2015. Virtual

currency, tangible return: Portfolio diversification with bitcoin. Journal of

Asset Management, 16, 6, 365-373.

Brauneis, A., Mestel, R., 2019. Cryptocurrency-portfolios in a

mean-variance framework. Finance Research Letters 28, 259-264.

Dyhrberg, A. H., 2016. Bitcoin, gold and the dollar- A GARCH

volatility analysis. Finance Research Letters, 85-92.

Eisl, A., Gasser, S.M., Weinmayer, K., 2015. Caveat emptor:

Does bitcoin improve portfolio diversification?

Engle, E., 2000. Dynamic conditional correlation - A simple

class of multivariate GARCH models.

Guesmi, K. Samir Saadi, S., Abid, I., Ftiti, Z., 2018.

Portfolio diversification with virtual currency: Evidence from bitcoin.

International Review of Financial Analysis.

Henriques, I., Sadorsky, P., 2018. Can bitcoin replace gold in

an investment portfolio? Journal of Risk and Financial Management 11, 48.

Hong, K., 2016. Bitcoin as an alternative investment vehicle.

Springer Science+ Business Media

Kajtazi, A., Moro, A., 2017. Bitcoin, portfolio

diversification and Chinese financial markets

Klein, T., Thu, H.P., Walthe, T., 2018. Bitcoin is not the new

gold, a comparison of volatility, correlation, and portfolio performance.

Working paper.

Lee, D.K.K., Li Guo, L., Yu Wang, Y., 2017. Cryptocurrency: A

new investment opportunity? Liu, W., 2018. Portfolio diversification across

cryptocurrencies. Finance Research Letters.

Lorenz, J., Strika, M., 2017. Bitcoin and cryptocurrencies -

not for the faint-hearted. International Finance and Banking 4, 1.

Petukhina, A., Trimborn, S., Härdle, W.K., Elendner, H.,

2018. Investing with cryptocurrencies - evaluating the potential of portfolio

allocation.

Platanakis, E., Urquhart, A., 2018. Should investors include

bitcoin in their portfolios? A portfolio theory approach.

Rockafellar, R.T., Uryasev, S., 1999. Optimization of

conditional value at risk. Journal of Risk, 21-41.

37

Salma Ouali

Svärd, S., 2014. Dynamic portfolio strategy using

multivariate garch model. Working Paper

Symitsi, E., Chalvatzis, K.J., 2019. The economic value of

bitcoin: A portfolio analysis of currencies, gold, oil and stocks. Research in

International Business and Finance 48, 97-110.

Urquhart, A., Zhang, H., 2016. Bitcoin a hedge or safe-haven for

currencies? An intraday analysis.

|