2.3 Co nclusio

The chapter examined three theoretical views about the link

between economic growth and financial development: the one stating that the

financial sector development leads to economic growth, another putting economic

growth ahead of financial development and lastly the view which does not

support the importance of financial development on economic growth. On the

empirical side, a strong positive role of financial development on economic

growth has been found mostly in developed countries, and a weak or absence of

link in developing countries. In some cases, the demand leading hypothesis has

not been supported. In the next chapter we present the Rwandan financial

sector.

Financial Development and Economic Growth in Rwanda

CHAPTER 3

OVERVIEW OF THE RWANDAN FINANCIAL SECTOR 3.0

Introduction

This chapter narrows the financial development issue to

Rwandan case and highlights the weaknesses as well as the strength of the

Rwandan financial system. To situate the level of financial development in

macroeconomic perspective, a brief review of Rwandan economy is first

presented. The chapter finishes with a comparison of the financial sector in

Rwanda with those of other country members of East African region where Rwanda

and Burundi were admitted in 2008.

3.1. Overview over the Rwandan economy

Rwanda is a small landlocked country in Central-East Africa,

with 26,338 square kilometers. Its GDP per capita was $ 62.95 in 1970 with a

population of 3.7 million, eight years after its independence from Belgium in

1962. The country is hampered by mountainous terrain and distance from the

sea.

Rwanda is among most densely populated countries in Africa.

In 2009, Rwanda was ranked 29th among densely countries in 239

countries with density of 379 people per square kilometer, far ahead of the

African average of 34 people per square kilometer. In 2009, the population was

9.998 million, growing at 2.8 %, compared to African average of 1.66 %, thus

putting increasing pressure on agriculture land and environment (United Nations

Population Division, 2008).

Rwanda's economy is essentially rural; nearly 81% of the

population lives in rural areas (United Nations Statistic Division, 2009) and

derives its livelihood from subsistence agriculture, cultivating coffee and tea

for export with rudiment methods. Besides agriculture, there is exploitation of

scarce natural resources in some regions like cassiterite, wolframite, and

methane recently discovered in Lake Kivu.

Rwandan economy has been improving since 2000 with an

increasing growth

rate especially for the last four years, when the country

maintained an average

growth rate vis-à- vis many African countries over the

period 2005-2008. In fact, the growth rate was 7.2 % in 2005, 7.3% in 2006, 7.9

% and 11.2 % in 2007 and 2008 respectively accumulating into an average growth

rate of 8.4 % above the African average rate of 5.82% during this period. In

addition, the country became the third, after Angola and Ethiopia (IMF, 2009).

Moreover, Rwanda has made considerable efforts in improving living conditions

of her population. Poverty has fallen by 3%, from 60% of the population living

under the poverty line in 2000/2001 to 56.9% in 2006 but leaving 37.9% still

extremely poor (IFAD website). However, Rwanda's development indicators are

still below the African and East African averages, as indicated by the table

below:

Table1: Trends i n average of per capita GDP

Indicator

|

Country

|

1970=

1980

|

1981=

1990

|

1991=

2000

|

2000=

2008

|

Overall average

|

Per capita GDP (in US$)

|

Rwanda

|

147.4

|

323.5

|

268.2

|

276.6

|

250

|

|

489.21

|

768.9

|

733.9

|

1029.8

|

734.59

|

|

232.45

|

313.9

|

278.8

|

346.76

|

288.69

|

Growth rate of GDP (%)

|

Rwanda

|

5.54

|

2

|

3.2

|

7.13

|

4.36

|

|

3.08

|

3.26

|

3.17

|

5.27

|

3.55

|

|

3.87

|

2.14

|

2.82

|

5.83

|

3.5

|

Share of Gross capital formation in GDP (in %)

|

Rwanda

|

14.45

|

18.71

|

13.35

|

17.27

|

15.84

|

|

29.80

|

26.07

|

20.05

|

24.26

|

25.32

|

|

22.29

|

17.77

|

16.26

|

19.15

|

18.94

|

|

Source: Author's calculations from data

provided by United Nations Statistics Division, CIA World Fact books and World

Development indicators Database.

As the table indicates, for the period 1981-1990 Rwanda

reached the highest average per capita GDP with $323.5 compared to the average

of $276.6 during the recent period ranging from 2000-2008. In addition, it is

only in this period where its per capita GDP and the share of Gross capital

formation in GDP was

above East African average. This was mainly due to political

stability and favorable weather that prevailed during that time which made

agricultural sector to contribute a lot in GDP.

The period 1990-2000 was marked by war of four years

(1990-1994), the genocide of 1994 in which more than one million lost their

lives and insecurity which affected the north (1996-1998). This explains the

decrease in above indicators. Despite this situation, the growth rate of GDP

exceeded African and East African average, as the country was trying to

recover. Although the recent period was marked by the highest per capita GDP in

2008 with $ 458.49, but the period was characterized by a low per capita GDP in

the period ranging from 2001-2003, a figure less than $200.

It is worth to say that it is in 2008 where the country

recovered and passed over the level of per capita GDP reached before the

genocide, that of 1988 with $360.87. The per capita GDP has been declining as

from 1989, one year before the beginning of the war of 1990, up to 1994 from

$360.87 in 1988 to $207.43 in 1994. Since 1995, the economic growth started to

recover and currently, though the per capita GDP is still low, but Rwanda is

among top performing in Africa with the growth rate currently above both

African and East African average.

Many reasons explain the poverty of the country: being a

landlocked country, on this it added the bad governance which has characterized

the country since its independence, war, genocide and insecurity, lack of

natural resources, little skilled human capital, as per year 2005, less than 1%

of the population had a tertiary education, and a low level of investment.

3.2 The Rwandan financial sector

We analyse the financial sector by looking at the banking

sector, MFIs, insurance companies and financial markets. We begin by mentioning

that the Rwandan financial sector can be traced back from the creation of the

Central Bank, National Bank of Rwanda and issue of the local currency, Rwandan

Franc (RWF) in April 1964.

Financial Development and Economic Growth in Rwanda

3.2.1 Banking sector

The development of the financial sector before the genocide

of 1994 was slow. At the time, only 3 commercial banks and 2 specialized banks

operated with a total of less than 20 branches in the country, and one

microfinance (UBPR) with around 146 branches. The war and the genocide affected

heavily the banking sector: The genocide itself resulted in closure of the

Central bank for 4 months. The former government left the country in 1994 for

the DRC, after committing the genocide, with two-thirds of the national

monetary base in addition to US $7 million in cash which was taken from the

UBPR (Alson et al, 2001). Consequently, it took two years for this bank to

reopen, in 1996. Moreover, almost both physical and human capital of all banks

were destroyed during the genocide.

The post genocide period was marked by increase in number of

banks, where in 2002 there were 6 commercial banks with 28 branches, 2

specialized banks and 1 union of financial institutions (UBPR) with 148

branches (NBR, 2004). In 2007, commercial banks operated only 38 branches,

making only 7 % of all branches of financial institutions and by the end of

2008, 8 commercial banks, 2 specialized banks and 1 Microfinance bank were

operating.

However, there was a lack of competition as three banks (BCR,

BK and ECOBANK) held 66% market share before the licensing of UBPR as

commercial bank in 2008. This situation has led to high interest rate spreads

(8.6% in 2005), a modest 16% per annum growth in deposits over the past 5

years, and lending primarily to a core group of about 50 relatively large

customers concentrated in Kigali and a few sectors (Murgatroyd et al, 2007).

The penetration of banking sector is very low, and worse in

rural areas. The survey conducted by FinMark Trust in 2008 showed that in

general, only 14 percent of the active population use banks, 7% use MFIs, 26%

are informally served and 52% are financially excluded. In rural areas, less

than 6 percent of the population hold savings account in a formal finance

institution. Indeed, penetration of domestic credit to the private sector is

underperforming, with 11

Financial Development and Economic Growth in Rwanda

percent of GDP, compared to 18 percent of GDP for peer countries

(NBR, 2008).

Several reasons explain the underdevelopment of financial

services. The weak culture of savings among the people is due to low level of

per capita income in the country. In fact, in 2009 Rwanda was ranked

21st poorest of the least developed countries in the world and 56.9

percent of its population lives on less than US$0.45 equivalent a day, the

poverty threshold in Rwanda (IMF, 2009).

Secondly, a high spread between the deposit rate (around 7%)

and a lending rate (around 16%) does not provide an incentive to the public to

save. Many bank accounts are used as a payment mechanism for employees. It is

important to note that due to relative higher penetration of UBPR, it has been

upgraded to commercial bank in 2008 and became BPR S.A, and that KCB, a new

regional bank from Kenya has been licensed.

3.2.2 Microfi na nce institutions

Microfinance initiatives mushroomed from 2002, primarily as a

response to the weak involvement of the traditional banks in small and micro

enterprises, and rural areas. Sixty-three microfinance institutions were

licensed in 2006 (Habyalimana, 2007).

In 2009, the microfinance sub-sector consisted of around 125

MFIs including 111 COOPECS (Kantengwa, 2009). In June 2006, NBR estimated that

MFIs represented 24.18% of the total financing of the economy with RWF 59bn

(equivalent of $100 million) out of RWF 244bn of credit of the financial

institutions and 25% of savings mobilization. The mobilized savings amounted to

RWF 65bn (equivalent to around $.110 million) out of RWF 259bn. Informal

finance is so popular that 73 % of total population reported using informal

loans in 2005 (Habyalimana, 2007).

However, Microfinance institutions are inexperienced,

characterised by management with poor corporate governance, weak information

systems, important losses caused by poor internal organisation and a

mismanagement of their loan portfolio (Kantengwa, 2009). All these weaknesses

culminated into

the failure of nine microfinance institutions in 2006 with

total deposits of more than $5.3 million, leading to a general panic (NBR,

2007). To include rural population in the financial system, UMURENGE SACCOs was

introduced in the end of 2008, a saving scheme to be operating in each of 421

sectors.

3.2.3 Insurance and pension funds

This sector comprises 5 classic insurance companies (SONARWA,

SORAS, COGEAR, CORAR and Phoenix of Rwanda Assurance Company) and six insurance

brokers. In 2006, only about 3% of the active population held insurance policy.

In addition, there are three public medical insurance companies: RAMA, MMI and

Mutuelle de Santé and one private company, AAR Health Services, licensed

in 2008. The relatively well performing RAMA and MMI serve only 5% of the

population (NISR, 2008).

The pension sector is assured by one Public Pension fund

(SSFR) and 10 Growing Private Pension funds. The SSFR covers only 7.5% of

active population and on overall less than 8% of the active population is under

pension schemes (NBR, 2009).

3.2.4 Financial markets

In January 2008, Rwanda established a capital market with the

creation of an Over-The-Counter market operated and regulated by a Capital

Market Advisory Council (CMAC). However, its market capitalisation is still

very low as only $ 360, 000 has been traded in 15 transactions (the average of

$24,000 in each transaction) and newspapers frequently reported that the OTC

has been silent due to lack of transactions recorded. The main reason is the

poverty of Rwandan citizen which does not allow the culture of saving where

even those who earn monthly salary are able to spend it for survival only. With

regard to market participants, Rwandan OTC has 7 members divided into three

categories: Stockbrokers, Dealers and Sponsors (CMAC website).

3.2.5 Financial liberalization i n Rwanda

Before the financial liberalization, tools of monetary policy

were mainly credit

rationing, directed credit and interest rate controls.

The financial deregulation

was characterized by legal reforms affecting the nature of

central bank supervision and new tools of monetary policy were introduced like

regal reserve requirements and discount rate, alongside the abolition of

interest rate ceilings, directed credit and credit rationing as well.

The process of financial liberalization started in March 1995

by the liberalization of exchange rate and interest rate in 1996. In the same

year, banking structure was opened to foreign investment and entry requirements

for MFIs were relaxed. However, despite abolition of controls on interest

rates, the rigidity in the later is still observed, fluctuating around 16% for

lending and 7% for deposit rates of interest, due to oligopolistic nature of

the banking system.

The period 2004-2006 was characterized by take over of

nonperforming banks due to poor corporate governance. BACAR and BCDI were taken

over by FINABANK and ECOBANK respectively, and the government sold its majority

of share in BCR. In 2006, the spread of MFIs nationwide came as another step in

financial liberalization, following the failure of commercial banks to deliver

in rural areas. However, as prophesized by Diaz-Alejandro (1985), the end of

2006 and 2007 turned the financial sector in crisis as consequence of

unmonitored regularization, after which the central bank started exerting basic

controls on financial institutions through micro finance law and regulation

adopted in 2008, and strengthened by creation of MFI association created in

2007.

3.2.6 Monetary policy i n Rwanda

Monetary policy is a responsibility of the NBR and is a part

of the annual economic program aiming at implementing the medium-term program

referred to as EDPRS. Like all central banks, NBR uses open market operations,

reserve requirements (fixed at 8% before 2009 and reduced to 5% from 2009), and

discount rate (which fluctuates between 7.5 % and 8%). With its basic objective

of price and foreign exchange stability, its development can be regarded in two

periods: the period of financial regulation, from 1964 to 1995 and after

liberalization in 1995.

Before 1995, the country was in fixed exchange rate regime.

From 1970 to 1990, the foreign exchange rate was 1$ for nearly 82 RWF. However,

the war period 1990-1994 saw many devaluations, especially that of 1991 with

51.5 % and that of 1994 of 91.64% and by the end of 1994, the exchange rate

stood at 1$ for 220 RWF (DUSHIMUMUKIZA, 2006).

The period of flexible exchange rate was characterized by

volatility in exchange rate. As evidence, in January 2003, the average exchange

rate stood at 511.2168 RWF for 1$, but by end of the year, the exchange rate

was at 574.83RWF for 1$. The depreciation rate stood at 11.6% from one year to

another. If we compare the average exchange rate of 2002 and 2008, the index is

115.2 in six years, from the exchange rate of 475.32 FRW for 1$ in 2002 to

547.61 FRW for 1$ in 2008 (NBR, annual report, 2008). Indeed, this exchange

rate can be compared to 220 RWF for 1$ in 1994.

Regarding price stability, again the rampant inflation

characterized the after liberalization period, as compared to the period before

where the price stability was observed. Evidence from Kigali (the Capital city)

in 2003 shows that the CPI for all products in constant terms of 1982 was

559.32 compared to the CPI of 408.93 and in 1996 (NBR, annual report of 2003).

The inflation rate is fluctuating around 7.5%

For money supply, there was an upward trend in money supply

to the level where its growth rate was above that of GDP. For instance, in

2007, increase in money supply was 31.25% against 13% of nominal GDP. Indeed,

in some years, the money supply experiences an over expansion, especially

during election periods like 2003 and 2008.

For payment system monetization, SIMTEL was introduced in

2005 aiming at speeding up the level of financial innovation, which is very

low, as in 2008 the value of transactions using bank cards was 0.59 percent of

the non cash payment instruments (dominated by cheques) and cash payment

represented 98% of the payment system (NBR, 2009). Introduction of Real Time

Gross Settlement and an Automated Clearing House were few among mechanisms of

such modernization.

Financial Development and Economic Growth in Rwanda

3.3 Comparison of financial development within

EAC

The discussion omits comparison based on the number of

financial institutions as the countries are not equally sized and formal

financial markets since Rwanda and Burundi do not have them while Kenya

launched its stock market (Nairobi Stock Exchange) in 1954 and those of

Tanzania and Uganda are operational since 1998. We rather use some ratios

regarded as proxies of the level of financial development.

The need for this comparison lies in the sense that the

macroeconomic policies of these countries are tied together, hence it pays for

Rwanda to know its status quo in this community of countries. Three indicators

are used: Liquid liabilities as % of GDP, claims on private sector to GDP ratio

and domestic credit to GDP ratio. Data which are sources of the figures are

presented in appendices.

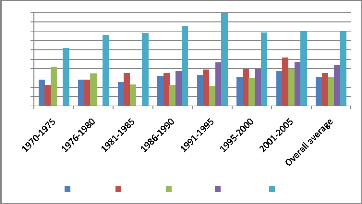

3.3.1 Ratio of Liquid liabilities (M3) to

GDP

Rwanda and Uganda are the last and their M3/GDP ratio are far

below the average of the AEC (21.98 % of GDP) with Kenya leading at 39.77%

compared to 15.35% of Rwanda, as shown by the chart below:

45

40

25

20

50

35

30

15

10

0

5

Rwanda Burundi Uganda Tanzania Kenya

Figure 1: Evolution i n ration of liquid liabilities i n

EAC

On overall, Kenya comes first followed by Tanzania, Burundi,

Rwanda and Uganda. We noted that in 2005, worldwide ranking of these countries

were: Kenya 94th, Tanzania 113rd, Burundi

118th, Rwanda 131st and Uganda 132nd out of

173 countries, with weighted average of 58%.

Financial Development and Economic Growth in Rwanda

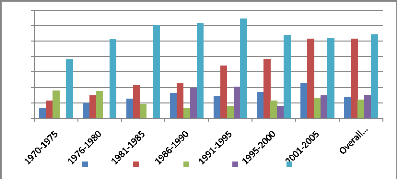

3.3.2 Claims o n private sector to GDP ratio

This indictor was suggested by some researchers as the best

measurement of the level of financial depth as discussed in chapter two. The

figure below indicates the level of financial depth in East African Countries

had been this indicator used.

35

30

25

20

15

10

0

5

Rwanda Burundi Uganda Tanzania Kenya

Figure 2: Evolution i n average of claims o n private

sector to GDP i n EAC

Kenya is still leading followed by Burundi whereas other

countries are almost at the same level, which is very low below the average of

14.75%. Rwanda is the fourth with 7.05% while Uganda is the last in the group

with 6.11%. Based on this indicator, we can say that Kenya enjoys a financial

deepening four times that of Rwanda. However, Rwanda has been improving but at

a slow rate compared to Burundi which made a significant improvement. This

ratio for Burundi was more than three times that of Uganda and more than double

that of Rwanda in recent period, while 30 years ago the difference between

these countries was slightly small (less than 3%).

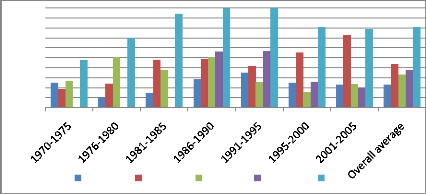

3.3.3 Domestic credit to GDP ratio

As the next figure shows, Burundi has been improving

considerably from the last in row during the period 1970-1975 (with 9.45 %) to

the 2nd position (with 36.62%) for last two consecutive periods,

from 1995 to 2005. Surprisingly, this indicator declined considerably in

Rwanda's post genocide where it moved from 17.51% as the average for the war

period of 1990-1995 to 11.54% for the last period 2001-2005 while the country

was supposed to be putting enough effort in the credit to private sector to

speed up the economic growth.

Financial Development and Economic Growth in Rwanda

45.00

40.00

50.00

35.00

30.00

25.00

20.00

15.00

10.00

0.00

5.00

Rwanda Burundi Uganda Tanzania Kenya

Figure 3: Evolution i n average ratio of domestic credit

to GDP i n EAC

This ratio for Rwanda was below the EAC average throughout

the period. Moreover, there is an increasing gap between Rwanda, the last in

group, and Kenya, the first, from 11.46% over the period 1970-1975 to 27.97%.

This is one among reasons that explain the gap in the level of economic

development among these countries. Uganda and Tanzania too have the low ratio.

Though several reasons can explain why Rwanda is lagging behind in financial

development, civil war, insecurity and poor governance are paramount factors to

the explanation. However, a detailed analysis is needed to explain why Tanzania

and Uganda are not performing well in some areas while they enjoyed a relative

stability, contrary to Burundi which was in war since 1993 up to 2005 and

performed well.

3.4 Co nclusio

Rwandan economy has been growing during post genocide period

but still the economy is at the lower level when compared to other countries.

Indeed, the financial development is still low and below the average of the

East African countries. When considering some indicators of the financial

development over the period 1970-2005, Rwanda is almost the last within five

countries though Uganda and Tanzania too are not performing well. This

observation brings to mind the empirical question of the extent to which the

level of financial development in Rwanda is linked with the level of economic

growth. Therefore the following chapter presents the methodology followed to

conduct this study.

Financial Development and Economic Growth in Rwanda

CHAPTER 4

METHODOLOGY

4.0 I ntroductio

This chapter presents the methods and techniques, the model,

estimation techniques and types of data used in this study in investigating the

causality among the proxies of financial development and economic growth.

4.1 Meaning and rationale of the model used

The use of VAR was motivated by its ability to capture the

dynamic interaction of financial sector development and economic growth. A VAR

is a direct generalization of the univariate AR(p) model to the case of a

vector of variables and is used to express the dynamic correlations between the

variables and hence is considered as an alternative to large-scale simultaneous

equations structural models (Brooks, 2008).

It allows treating each variable as endogenous thus avoiding

restrictions, judged incredible by Sims (1980), imposed by univariate AR, by

specifying some variables as being exogenous. This model was chosen because the

changes in indicators of financial development are possibly correlated with the

disturbance term in the equation of economic growth. This is because an

unobserved factor that influences growth of GDP may very well influence

indicators of financial development, making them endogenous. Further more, this

study joins other studies on the matter which used the VAR frame work, namely:

Hassan and Jung-Suk (2007); Teame (2002); Sakutukwa (2008) and others.

4.2 Model specification and rationale of

variables

In a VAR model, all variables have equations linking the

change in that variable to its own current and past values and the current and

past values of all the variables in the model, as it describes the dynamic

evolution of a number of variables from their common history (Verbeek, 2004).

The model is expressed

in a matrix form as:Yt = B +

Elic_i AtYt_i + Et with:

V, = ( GRATES

DEPTHBANKPRIVATESOPHT )

Yt : It is a 5×1 column vector of 5 variables

including proxy measures of the financial development, B is a 5×1 column

vector of constants, At and

Yt_i are

5×5 matrices of coefficients and lagged variables

respectively, i is the lag length

to be determined by AIC criteria and et is a 5×1

column vector of error terms. Variables included in the models are:

GRATE = Growth rate of Real per capita GDP, following the works

of Sinha and Macri (2001) and Kesseven et al (2007);

DEPTH = Claims on Private sector to GDP ratio considered as

proxy of financial deepening, following the works of Karima and Holden (2001),

Firdu and Struthers (2003) and Zhang et al (2007);

BANK = Domestic credit by deposit money bank and other banking

institutions divided by total domestic credit;

PRIVATE = Claims on the non-financial private sector to gross

domestic credit; SOPHT = Ratio of broad money to narrow money (M2/M1) as proxy

of financial sophistication, following the work of Sakutukwa (2008).

BANK and PRIVATE are inspired by the work of Levine and King

(1993). Unlike to them, we have included the domestic credit for other banking

institutions in BANK to mitigate the drawbacks of this indicator as commercial

banks are not the only financial institutions to provide valuable financial

functions. However, there is still a weakness in these proxies in Rwanda

because data used on assets of financial institutions do not include the UBPR

which play an important role in Rwandan financial sector.

4.3. Model estimatio

4.3.1 Statio narity and coi ntegratio

Due to spurious regression resulting from nonstationary

series in the regressions, we have conducted the tests for stationarity, using

ADF to check whether the residual series are white noise. The tests for

cointegration have been conducted to determine the form of the VAR to be

estimated. In fact, trend stationary variables are estimated by OLS, if the

variables contain stochastic trends and cointegrated, a VECM is used and

finally if the variables are not stationary and not cointegrated, the model is

estimated after the stochastic

trends have been removed by taking first differences of the data.

All tests were run within Eviews 6.

4.3.2 Granger causality tests

To determine which sets of variables have a significant

effects on each dependent variable, causality tests have been conducted by

restricting the coefficient of the lags of a particular variable to zero

(Wooldridge, 1990). The objective is to find out if changes in one variable do

affect changes in another variable and vice versa. If this is the case, as

explained by Brooks (2008), a sets of lags of the included variable should be

significant and it would be said that there is a bi-directional causality,

otherwise it should be said that some included variables are exogenous or no

causality exists at all between variables had been all lags insignificant.

4.3.3. Variance decomposition and Impulse

response

The ambiguity in interpreting individual coefficients in VAR

model (Gujarati, 2004) motivated us to use the variance decomposition and

impulse response function which trace out the response of the dependent

variable in the VAR model to shocks in the error term for several periods in

the future, keeping constant all other variables dated t and

before.

4.4. The data source and measurement

The five considered time series are ratios we have computed

from data provided by the IFS Yearbooks. The database includes 42 annual

observations from 1964 to 2005. Unlikely to previous studies which used natural

logarithm of the series, we did not find any graphical relationship, as advised

by Gujarati (2004), which motivates a priori transformation of the data to

log-log model.

4.5 Co nclusio

This chapter has presented the methodology that has been used

in this study. The next chapter presents and analyses the results of

econometric estimation. The main objective of the chapter is the hypothesis

testing.

Financial Development and Economic Growth in Rwanda

CHAPTER 5

MODEL ESTIMATION AND FINDINGS

5.0 I ntroductio

So far we have presented the literature both on theoretical

and empirical side on the causality between economic growth and financial

development. It is now time to turn to the empirical testing of this

relationship for Rwandan economy. This chapter presents the results obtained

from econometric testing and discusses the meaning and reason behind the

figures.

5.1 Test for statio narity

The footstep of this analysis is to determine whether the

series are stationary or not. The ADF was used to test for stationarity of

these series as it provides a superior test to DF, especially in case the

residuals of the regression could be serially correlated. The lag length has

been automatically selected by AIC from nine proposed lags and all three

possibilities have been tested: neither intercept nor trend, intercept but no

trend and both intercept and trend. In all cases, results were found similar

irrespective of the model used.

Here we present the results from the general model including

intercept with

trend, as depicted by: AYt=f3i +

f32t + SYt_i + al El:=i AYt_p + Et.

In addition, we have tested for the presence of trend in series,

with the model:

Yt =cx +f3t + Et. The presence or the absence of the trend will

be used for

subsequent tests. The table below presents the results:

Table 2: ADF Test Statistics i n levels

Variable

|

t= statistics

|

Critical values at

|

Lag length

|

Decision at 5%

|

|

5%

|

|

Presence of trend

|

GRATE

|

-3.59

|

-4.20

|

-3.52

|

1

|

Stationary

|

No

|

DEPTH

|

-6.11

|

-2.62

|

-1.94

|

0

|

Stationary

|

Yes

|

|

Variable

|

t= statistics

|

Critical values at

|

Lag length

|

Decision at 5%

|

|

5%

|

|

Presence of trend

|

SOPHT

|

-3.36

|

-4.21

|

-3.52

|

2

|

Not stationary

|

Yes

|

BANK

|

-2.96

|

-4.19

|

-3.52

|

0

|

Not stationary

|

Yes

|

PRIVATE

|

-2.25

|

-4.21

|

-3.55

|

3

|

Stationary

|

Yes

|

|

The hypotheses tested are:

Ho: S = 0, the series are not stationary, )62 = 0,

there is no trend

Ho: S * 0, the series are stationary, )62 * 0, there

is a trend

After taking first differences of SOPHT and BANK, the series

were found to be stationary at 1%, as the table below depicts:

Table 3: ADF Test Statistics with first

difference

Variables

|

t=

|

Critical values at

|

Lag length

|

Decision

|

|

Statistic

|

1%

|

5%

|

selected

|

|

D(SOPHT)

|

-6.019

|

-4.205

|

-3.526

|

0

|

Stationary at 1%

|

D(BANK)

|

-6.759

|

-4.211

|

-3.529

|

1

|

Stationary at 1%

|

|

The above results conclude that GRATE, DEPTH and PRIVATE are

I(0) while SOPHT and BANK are I(1). Therefore, VAR in levels cannot be

applied.

5.2 Test for coi ntegratio

In econometric literature, it is not clear whether

cointegration should be applied to only series integrated of the same order.

Though Verbeck (2004) noted that the concept of cointegration can be applied to

(nonstationary) integrated time series only and Dickey et al, quoted by

Gujarati (2004), stipulated that Cointegration deals with the relationship

among a group of variables, where (unconditionally) each has a unit root,

however Brooks (2004) stressed that it is also possible to combine levels and

first differenced terms in a VECM. The later therefore illustrates that

cointegration can exist among variables not integrated of the same order.

Heij et al (2004) developed the mathematical proof of this

view where they asserted that a cointegration relationship exists between

stationary and nonstationary variables. If their mathematical proof is put in

simple terms, there are three possibilities in VAR with many variables: If m:

the number of variables, r= rank of the matrix of coefficients and also the

number of cointegration relations, therefore:

· If all variables are stationary, r=m and all roots lie

outside the unit cycle

· If all variables are not stationary, r=0, there are m

unit roots or m stochastic trends.

· If some variables are stationary and others not

stationary, r= 0<r<m, there are m-r unit roots, the polynomial have m-r

common stochastic trends and there are r cointegrating relations.

As some variables are stationary and others not, Johansen

cointegration test has been used to determine whether there exists a long-run

relationship between these variables. This test was preferred to Engle-Granger

approach because in case of five variables we may have more than one

cointegrating relationship (Brooks, 2004).

a) Johansen coi ntegratio n test

Johansen trace test was used on the number of cointegrating

relations with null hypothesis of no cointegration between series against the

alternative hypothesis of existence of cointegration between the series. All

variables enter the cointegration analysis in levels. This table depicts

cointegrating vectors for each model with 4 lags.

Table 4: Number of coi ntegrati ng relations by model, at

5% level*

|

Data Trend:

|

None

|

None

|

Linear

|

Linear

|

Quadratic

|

|

Test Type

|

No Intercept

|

Intercept

|

Intercept

|

Intercept

|

Intercept

|

|

No Trend

|

No Trend

|

No Trend

|

Trend

|

Trend

|

|

Trace

|

2

|

3

|

3

|

4

|

3

|

|

Max-Eig

|

0

|

1

|

3

|

4

|

3

|

*Critical values based on MacKinnon-Haug-Michelis (1999)

All five possibilities about the nature of deterministic trend

assumption suggest

that the series are cointegrated. At least there is one

cointegrating factor except

the Max-Eig method with neither intercept nor

trend in data, which is unlikely to

be the case. The subsequent step is to determine whether an

intercept or trend or both are included in the cointegrating relationship and

to present the results of the selected model. The analysis of the nature of

trend conducted showed that all variables except GRATE have significant

intercept and trend. After estimating the selected model of both intercept and

trend with 3 lags selected by AIC, the results were as follows:

Table 5: Unrestricted Coi ntegrati ng Rank Test

(Trace)

|

Hypothesized

No. of CE(s)

|

Eigenvalue

|

Trace

Statistic

|

0.05

Critical Value

|

Prob.**

|

|

None *

|

0.890720

|

137.1029

|

88.80380

|

0.0000

|

|

At most 1

|

0.517635

|

55.19081

|

63.87610

|

0.2162

|

|

At most 2

|

0.306696

|

28.21578

|

42.91525

|

0.6091

|

|

At most 3

|

0.251814

|

14.66319

|

25.87211

|

0.6026

|

|

At most 4

|

0.100754

|

3.929364

|

12.51798

|

0.7523

|

Trace test indicates 1 cointegrating eqn(s) at the 0.05 level *

denotes rejection of the hypothesis at the 0.05 level **MacKinnon-Haug-Michelis

(1999) p-values

The statistic of 137.1 considerably exceeds the critical value

(of 88.8) and so the null of no cointegrating vectors is rejected. But the

2nd row shows that the null hypothesis of at most one cointegrating

vector can not be rejected as trace statistic of 55.19 is less than critical

value of 63.9. Therefore, there exists one cointegrating relation which means

that the rank of the matrix (r) is one.

The results from trace test were the same if maximum

eigenvalue test was considered. As there is one cointegrating vector, this

allows us to estimate a VECM, in line with advice of Brooks (2004) of not using

models in differences when cointegration is present, as this flows away

important information and have no long-run solution.

5.3 Vector Error Correction Model (VECM)

The lag length was chosen based on AIC, which was consistent

with LR and HQ. Noting that as data are annual observations, a maximum of 4

lags is reasonable, as suggested by Brooks (2004) based on the frequency of the

observation and AIC picked 3 lags. The estimated output is presented in the

appendix, but the table below presents the significant lags at 5% level.

Financial Development and Economic Growth in Rwanda

Table 6: Significant Vector Error Correction

Estimates

|

Variable

|

Significant lags at 5% and their coefficients i n I

l

|

|

D(GRATE)

|

CointEq1

[-2.03]

|

D(GRATE(-1)) [0.63]

|

D(GRATE(-2)) [0.25)

|

D(DEPTH(-1)) [0.69]

|

|

D(DEPTH(-2)) [0.86]

|

D(DEPTH(-3)) [0.96]

|

D(Bank(-1)) [0.4]

|

|

|

D(DEPTH)

|

CointEq1

[-1.16]

|

D(DEPHT(-1)) [0.69]

|

D(DEPTH(-2)) [-0.79]

|

D(DEPTH(-3)) [-0.49]

|

|

D(SOPHT(-1) [1.01]

|

|

|

|

|

D(SOPHT)

|

CointEq1

[-0.72]

|

D(PRIVATE(-2)) [-0.7]

|

|

|

|

D(BANK)

|

D(Bank(-1))

[-0.51]

|

D(PRIVATE(-1)) [1.11]

|

D(PRIVATE(-2)) [-1.26]

|

D(PRIVATE(-3)) [0.95]

|

|

D(PRIVATE)

|

D(PRIVATE(-1)) [0.62]

|

D(PRIVATE(-2)) [-0.52]

|

D(PRIVATE(-3)) [0.48]

|

|

The Error correction term showing the long-run equilibrium is

estimated as:

CointEgl = GRATEt_i -- 0.057 SOPHTt_i + 0.0019 /31t -- 0.0019

/30

+ 0.332DEPHTt_1 -- 0.114 PRIVATEt_i + 0.298BANKt_1

In all equations, the cointegrating equation has a negative

sign as expected and significant in three out of five equations. We note from

the table above that in many equations of the VECM, the coefficients of lags of

other variables are not significant, especially for PRIVATE which is determined

solely by its own lags, SOPHT is explained by one lag from PRIVATE whereas for

DEPTH only its own lags and 1 lag of SOPHT are significant.

The cointegration is strongly significant for GRATE, DEPTH and

SOPHT. However, as noted by Brooks (2004), evaluation of the significance of

variables in a VECM is based on the joint tests on all of the lags of a

variable in the equation rather than individual coefficient estimates.

Therefore we proceed to F test as indicated in the table below:

Table 7: F=statistics for VECM

|

Variables

|

D(GRATE)

|

D(DEPTH)

|

D(SOPHT)

|

D(Bank)

|

D(Private)

|

|

R2

|

0.97

|

0.67

|

0.67

|

0.62

|

0.55

|

|

Adj R2

|

0.95

|

0.41

|

0.41

|

0.33

|

0.19

|

|

F-stat

|

45.41

|

2.59

|

2.60

|

2.12

|

1.54

|

Critical values of F-statistic are taken from F-statistic table

provided by Gujarati

(2004) and are 3.09; 2.2 and 1.84 for 1%; 5% and 10%

respectively. The VECM

shows that for GRATE the null hypothesis being all

coefficients are simultaneously zero is rejected at 1%, for DEPTH and SOPHT the

null hypothesis is rejected at 5%, for BANK it is rejected at 10% and for

PRIVATE the null hypothesis can not be definitely rejected.

The results suggest that there exist: a long-run relationship

between growth rate of real per capita GDP and proxies of financial

development, a long-run relationship between financial depth, rate of growth of

real per capita GDP and other included measures of financial development and

the same applies to financial sophistication. The F-test denies any long-run

relationship between the ratio of credit to private sector to total domestic

credit with GDP, and other measures of financial development and for the ratio

of credit allocated by banks to total domestic credit when 5% level is

considered.

5.4 The E ngle=Gra nger test

The test is meant to detect any short-term relationship

between the variables and it is applied to test whether the changes in one

variable can cause changes in another variable and vice-versa. As there is a

long-run relationship between variables, the error correction term will be

included in the Granger causality test for estimating a short-run relationship.

It is worth noting that Granger causality test should be applied to stationary

series (Sinha and Macri, 2001). Therefore, we have applied this test with

differences in non-stationary series. When estimated the VAR model with

differences in nonstationary variables to come up with lag length, the AIC and

HQ criteria gave out 5 lags. The model to be estimated is:

M'at =0(0-Foci ~ 78 ~ ~~ ~ 98 ~

8 8 ~~ where Ya and Yb are

~~~ ~~~

variables on which causality test is being applied. The

hypotheses to be tested are:

Ho: âi=0, Yb does not Granger causes Ya

H1: âi ?0, Yb does Granger causes Ya

The results for Granger causality are presented in table

below:

Financial Development and Economic Growth in Rwanda

Table 8: Marginal significance levels associated with

joint F=test

|

Dependent variable

|

Lags of variables

|

Significant lags

|

|

GRATE

|

DEPTH

|

DSOPHT

|

DBANK

|

PRIVATE

|

|

GRATE

|

0

|

9.8E-13

|

0.01503

|

0.60738

|

0.16923

|

DEPTH and SOPHT

|

|

DEPTH

|

0.99980

|

0

|

0.12400

|

0.99071

|

0.61635

|

None

|

|

DSOPT

|

0.00777

|

0.00338

|

0

|

0.54904

|

0.28578

|

GRATE and DEPTH

|

|

DBANK

|

0.99662

|

0.08847

|

0.73048

|

0

|

0.03597

|

PRIVATE

|

|

PRIVATE

|

0.25647

|

0.29164

|

0.38541

|

0.82127

|

0

|

None

|

The table above gives the probability values at 5% for the

null hypothesis that all the lags of a given variable are jointly insignificant

in a given equation. The second row after the headings shows that all the lags

of DEPTH and DSOPHT are jointly significant in explaining the changes of GRATE

(values less than 0.05). Indeed, both lags of GRATE and DEPTH jointly explain

the changes in DSOPHT. Moreover, a part from the lags of PRIVATE which jointly

explain DBANK, there is as well no causality between DEPTH and other variables

as applied for PRIVATE.

The Engle-Granger causality suggests that in short-term, there

is unidirectional causality from financial deepening to growth rate of real per

capita GDP and bidirectional feedback between financial sophistication and

growth rate of real per capita GDP. But other proxies of financial development

do not seem to have affected economic growth, or being affected by economic

growth.

5.5 Impulse responses and variance

decompositions

The Granger Causality solves the problem of existence or not

of variables with significant lags in the model but will not indicate whether

there is a positive or a negative relationship between variables or how long

the effects will take place. Fortunately, this information is given by Variance

decomposition and Impulse responses.

5.5.1 Variance decompositio

Gebhard and Wolters (2007) define variance decompositions as a

determinant

of how much the s-step-ahead forecast error variance of a given

variable is

explained by innovations to each explanatory variable for s = 1,

2, etc. The estimated variance decompositions are as follows:

Table 9: Variance decomposition of GRATE

|

Period

|

S.E.

|

GRATE

|

DEPTH

|

SOPHT

|

BANK

|

PRIVATE

|

|

1

|

0.110866

|

100.0000

|

0.000000

|

0.000000

|

0.000000

|

0.000000

|

|

2

|

0.124707

|

82.69667

|

8.579287

|

3.272943

|

3.121836

|

2.329268

|

|

3

|

0.147683

|

68.46577

|

21.21998

|

2.911180

|

3.706309

|

3.696768

|

|

4

|

0.161082

|

63.06704

|

22.01977

|

5.362547

|

4.577584

|

4.973060

|

|

5

|

0.230705

|

30.74644

|

56.71985

|

2.944156

|

5.417225

|

4.172328

|

|

6

|

0.264102

|

25.86977

|

48.00195

|

11.86883

|

10.10530

|

4.154157

|

|

7

|

0.279128

|

27.88629

|

45.35033

|

11.21903

|

9.305821

|

6.238536

|

|

8

|

0.297045

|

24.98740

|

40.23873

|

20.10273

|

9.132219

|

5.538915

|

|

9

|

0.299774

|

25.47580

|

39.51314

|

20.12288

|

9.053579

|

5.834607

|

|

10

|

0.311132

|

25.82532

|

38.50044

|

21.06230

|

8.824819

|

5.787122

|

The data shows that in period 1, changes in Growth rate of GDP

are due to its own shocks at 100%. However as time passes, the effects of

shocks of other proxies of financial development to GDP increase significantly,

especially financial depth shocks, which increase from 0 in period 1 to 56% in

fifth period and represent more than 45% of all shocks on GDP from period 5-7

and nearly 40% above period 8. For Financial sophistication, although its

shocks to GDP are low up to fifth period, they become important in the

long-run, as they account from 10% - 20% of the whole shocks in GDP growth

rate.

In long-run, BANK and PRIVATE exert some influence on Growth

rate of GDP as they account for around 9% and 6 % respectively after the

seventh period. This leads to a considerable decrease of responsiveness of

growth rate of GDP to its own shocks from the range of 20% to 30 % after the

fifth period.

Table 10: Variance decomposition of DEPTH

|

Period

|

S.E.

|

GRATE

|

DEPTH

|

SOPHT

|

BANK

|

PRIVATE

|

|

1

|

0.166228

|

6.593561

|

93.40644

|

0.000000

|

0.000000

|

0.000000

|

|

2

|

0.177693

|

5.794367

|

81.81403

|

10.71161

|

1.676598

|

0.003399

|

|

3

|

0.181328

|

6.251779

|

78.93336

|

11.59888

|

3.148914

|

0.067069

|

|

4

|

0.196067

|

5.909571

|

67.51985

|

21.31578

|

3.279901

|

1.974900

|

|

5

|

0.200638

|

5.771625

|

64.94746

|

20.47421

|

6.396104

|

2.410596

|

|

6

|

0.203363

|

5.642555

|

63.22212

|

20.70156

|

7.800917

|

2.632850

|

|

7

|

0.204559

|

5.698593

|

62.48965

|

20.49198

|

8.642176

|

2.677599

|

Financial Development and Economic Growth in Rwanda

Period S.E. GRATE DEPTH SOPHT BANK PRIVATE

|

8

|

0.206029

|

5.618773

|

61.74162

|

20.20135

|

9.476386

|

2.961867

|

|

9

|

0.206866

|

5.583026

|

61.38685

|

20.08648

|

9.998728

|

2.944921

|

|

10

|

0.209391

|

5.449760

|

61.67798

|

19.73869

|

10.25844

|

2.875138

|

From the first period, the shocks in GDP growth rate account

for 6.59% of the shocks in DEPTH and no other variable exerts a shock on

financial depth. However, as from the fourth period, the financial

sophistication exerts a relatively higher significant influence on DEPTH than

other variables, around 20%. Shocks in rate of GDP account still for around 5%

and 2.8% for PRIVATE. It is noted that the impact of BANK shocks as well

increase in the long-run, from 0% to 10.25% from the first period onwards.

Table 11: Variance decomposition of SOPHT

|

Period

|

S.E.

|

GRATE

|

DEPTH

|

SOPHT

|

BANK

|

PRIVATE

|

|

1

|

0.074312

|

26.69308

|

0.003523

|

73.30339

|

0.000000

|

0.000000

|

|

2

|

0.092146

|

18.38277

|

0.672448

|

74.86819

|

6.069340

|

0.007246

|

|

3

|

0.133858

|

9.698140

|

11.79599

|

67.75000

|

7.847544

|

2.908331

|

|

4

|

0.170257

|

6.012045

|

23.10979

|

54.15415

|

12.49342

|

4.230598

|

|

5

|

0.220413

|

3.774206

|

39.20184

|

37.55349

|

15.89273

|

3.577740

|

|

6

|

0.240093

|

3.239503

|

40.45313

|

31.95285

|

20.92763

|

3.426890

|

|

7

|

0.258410

|

2.844621

|

43.07799

|

28.56225

|

21.77780

|

3.737332

|

|

8

|

0.271110

|

2.841146

|

44.52708

|

26.18426

|

22.98927

|

3.458246

|

|

9

|

0.279182

|

2.780299

|

45.79558

|

24.69353

|

23.46618

|

3.264411

|

|

10

|

0.284385

|

2.707705

|

46.31954

|

23.86455

|

23.96186

|

3.146348

|

From the above table, the shocks in growth rate of GDP account

for 26.69% in explaining changes in financial sophistication whereas its own

shocks account for 73%, as other variables do not influence SOPHT in the first

period. However, this order changes over time as financial depth takes over

growth rate of GDP in explaining changes in financial sophistication. In fact,

starting from the third period, shocks in financial depth lead to variability

in financial sophistication by 11.7% compared to 9.6% of growth rate in GDP

where still its own shocks account for more than 60%.

The influence of financial depth increases considerably up to

40% in sixth period and the own shocks decline to 31.95%, coupled with an

increase in influence of BANK with 20.92% and a decrease in influence of GDP

rate from 26.69% to 3.23% and remained at this level. The impact of PRIVATE

shocks

remains low close to 3.5% whereas that of shocks from

financial depth account for 40% to 45% in long-run, leaving the own shocks

between 30% to 23% and BANK shocks around 23%.

Table 12: Variance decomposition of BANK

|

Period

|

S.E.

|

GRATE

|

DEPTH

|

SOPHT

|

BANK

|

PRIVATE

|

|

1

|

0.108855

|

0.758292

|

7.481317

|

2.693772

|

89.06662

|

0.000000

|

|

2

|

0.134533

|

2.800047

|

9.892457

|

3.375928

|

70.39165

|

13.53991

|

|

3

|

0.157558

|

3.654779

|

15.77366

|

3.449549

|

66.83704

|

10.28497

|

|

4

|

0.179687

|

4.319090

|

21.15028

|

5.165073

|

61.43189

|

7.933671

|

|

5

|

0.210744

|

5.307566

|

19.52585

|

10.44650

|

54.85325

|

9.866828

|

|

6

|

0.238217

|

5.969085

|

17.27681

|

17.65179

|

48.14008

|

10.96223

|

|

7

|

0.252272

|

6.237416

|

17.76269

|

20.31924

|

45.59069

|

10.08995

|

|

8

|

0.269294

|

6.611854

|

17.00039

|

23.16878

|

43.29296

|

9.926012

|

|

9

|

0.288331

|

6.654749

|

15.18331

|

25.94057

|

40.74650

|

11.47487

|

|

10

|

0.301548

|

6.780441

|

14.72203

|

27.67418

|

39.01775

|

11.80560

|

The part of changes to BANK due to its own shocks declines

sharply from 89% in the first period to around 40% in long-run. In the

short-run, shocks from DEPTH have a largest impact on BANK, varying from 7% to

21% whereas in long-run, shocks from SOPHT outweigh DEPTH shocks in explaining

changes in BANK. Financial deepening and sophistication continue to exert a

significant influence on the ratio of sources of credit (BANK), contributing to

40% of BANK shocks in the long-run (from the fifth period). Whereas, the shocks

from growth rate of GDP and PRIVATE account for nearly 6% and 10%

respectively.

Table 13: Variance decomposition of PRIVATE

|

Period

|

S.E.

|

GRATE

|

DEPTH

|

SOPHT

|

BANK

|

PRIVATE

|

|

1

|

0.058234

|

3.888004

|

8.796400

|

31.81067

|

0.011581

|

55.49335

|

|

2

|

0.113552

|

7.271370

|

4.966717

|

42.35623

|

0.397619

|

45.00806

|

|

3

|

0.147942

|

7.691150

|

8.030448

|

46.93222

|

1.178470

|

36.16772

|

|

4

|

0.185169

|

7.908759

|

8.726697

|

52.17925

|

0.932194

|

30.25310

|

|

5

|

0.228011

|

8.044798

|

8.260887

|

54.36709

|

0.645529

|

28.68169

|

|

6

|

0.267550

|

7.654312

|

6.582612

|

58.03725

|

0.605966

|

27.11986

|

|

7

|

0.295786

|

7.572517

|

6.240606

|

59.76170

|

0.888040

|

25.53714

|

|

8

|

0.325691

|

7.389561

|

5.409754

|

61.44629

|

0.957495

|

24.79690

|

|

9

|

0.352531

|

7.122818

|

4.661823

|

61.92543

|

1.102570

|

25.18736

|

|

10

|

0.376020

|

6.932724

|

4.193691

|

62.39958

|

1.343631

|

25.13037

|

Compared to other variables mentioned above, PRIVATE own shocks

are

relatively small (55.5%) in the first period, and the shocks decline

sharply to a

quarter in long-run. Shocks from Financial sophistication have

a strong influence on PRIVATE and account for more than a half of total shocks

from the fourth period onwards. Shocks from BANK are insignificants as they do

not account for 2% and shocks from growth rate of GDP and DEPTH together

account for nearly 10% of total PRIVATE shocks.

5.5.2 Impulse response models

Gebhard and Wolters (2007) define impulse responses as the

measure of the effect of a unit shock of the variable i at time t on the

variable j in later periods. So for each variable from each equation

separately, a unit shock is applied to the error term and the effects upon the

VAR system over time are noted. Details of impulse responses are presented in

appendices and their summarized results are:

o Positive shocks of DEPTH and BANK to GDP growth rate but

negative shocks from SOPHT and PRIVATE.

o Positive shocks on DEPTH from GDP growth rate, financial

sophistication and BANK in short-run. Moreover, SOPHT and BANK have positive

shocks on DEPTH in long-run and negative PRIVATE shocks on DEPTH.

o Positive shocks on financial sophistication from BANK and

growth rate of GDP in short-run and negative shocks from growth rate of GDP,

DEPTH and PRIVATE in long-run.

o Positive shocks on BANK from PRIVATE and negative shocks from

growth rate of GDP and financial sophistication.

o Negative shocks on PRIVATE from all variables.

In the results above, the ordering was GRATE, DEPTH, SOPHT,

BANK, and PRIVATE. Unfortunately, the main drawback of Variance decomposition

and Impulse responses is that if the variable order is altered the results will

change too. For independent results from variable order, a priori knowledge

about the order is required, but not easy in most interdependent financial time

series data.

5.6 Discussion of findings

The tests revealed a long-run relationship between the Growth

rate of real per

capita GDP and 4 proxies of financial development.

Precisely, financial

deepening and financial sophistication were revealed to be

associated to this rate of GDP in the long-run. This implies that as the

economy allocates more credit to the private sector, as new financial

instruments are introduced in Rwandan financial system, with time, then the

level of economic growth will be affected. The causality test, Variance

decomposition and impulse responses show that financial deepening influences

positively economic growth. But no bidirectional causality detected from growth

rate of GDP to financial deepening.

These results confirm the importance of the level of financial

depth for Rwandan economic growth, unlikely to the conclusion of some

researchers who used panel data analysis and affirmed the irrelevance of the

level of financial deepening on economic growth for Sub-Saharan Africa and poor

countries in general, as noted by Hassan and Jung-Suk (2007) and Michael and

Giovanni (2001). Our results do agree with the conclusions of Zhang et al

(2007) in China, Demetriades and Luintel (1996) in India and Sakutukwa (2008)

in Zimbabwe.

The causality test and variance decomposition showed a

bi-directional influence between the level of financial sophistication and

economic growth. Surprisingly, impulse responses show that this relationship is

negative and a mere interpretation may conclude that financial sophistication

aggravates economic growth. But there can be an intuitive explanation of this

situation: «the true measurement of the financial sophistication in

Rwanda». The used growth rate of real per capita GDP excludes effects of

inflation and the increase in the ratio of M2 to M1 used as proxy of financial

sophistication could imply increase in money supply due to inflationary

pressure rather than financial innovation.

This is the case for Rwanda where post genocide economy was

characterized by high rate of inflation and volatility in exchange rate.

Despite the increase in the quasi-money which resulted in the increase of the

ratio of M2 to M1, there was no E-banking in Rwanda up to 2005, no remarkable

new financial instruments and ATM cards were recent in few banks, in major

towns only.

No link was found between economic growth and allocation of

credit. Were the

relationships to be established by Granger causality, the

impulse responses

show that the relationship would be negative. The absence or a

negative relationship between the growth rate of real per capita GDP and

PRIVATE, and between PRIVATE and DEPTH can be explained by the allocation of

credit. Credit devoted to agricultural sector which employs more than 80% of

the population was less than 1.5% of total credit to private sector while the

manufacturing, trade, restaurants and hotels received more than 60% of the

total credit, while these sectors employ less than 5% of the population and

contributed to only 17.4% in GDP in 2005.

Moreover, some loans were given to no profitable projects and

non credit worthy customers as indicated by the high level of defaulters which

led to bank crisis in former BACAR, BICDI and many MFIs. These findings of

negative relationship between credit allocation and economic growth conquer

with findings of Karima and Holden (2001), in a panel of 30 developing

countries.

5.7 Co nclusio

The study finds a strong positive causality from financial

deepening to economic growth and a negative bi-directional feedback between

economic growth and financial sophistication, in the short-run, and a long-run

relationship between economic growth and proxies of financial development.

The lack of short-run relationship between economic growth and

the credit allocation, from the source (commercial bank versus central bank) to

the users (private sector versus public sector) has been confirmed, while in

the long-run, variance decompositions and impulse responses showed a minor

relationship between economic growth rate and credit allocation. The found

negative link between level of economic growth and financial sophistication is

explained by the lack of accuracy of measurement of financial sophistication in

Rwanda. The next chapter will therefore put forward the general conclusions and

recommendations of the study.

Financial Development and Economic Growth in Rwanda

CHAPTER 6

CONCLUSIONS AND RECOMMENDATIONS

6.0 I ntroductio

This study intended to examine the bi-directional influence

between financial development and economic growth in Rwanda from 1964 to 2005.

Chapter one presented the existing problem which was the rationale of our study

alongside the objectives, research hypotheses among others. Chapter two

reviewed the literature on the subject both on theoretical and empirical

ground. In chapter three, a comparative analysis of the level of financial

development within East African countries has been carried out and revealed a

weak level of financial development in Rwanda. The results indicate that Rwanda

either takes the fourth or the last position among five countries.

In chapter four, we have explained the methodology followed,

focused on a VAR with five variables, namely: the indicator of financial

deepening, financial sophistication and other two indicators of the credit

allocation, and the growth rate of real per capita GDP was used as proxy of

economic growth. The fifth chapter has been devoted to econometric testing.

This chapter summarizes the results of the study and gives recommendations as

well as areas for further studies.

6.1 Summary of findings

The empirical results demonstrated both a short and a long-run

relationship between both financial depth and sophistication and economic

growth. For financial deepening, the causality runs from financial deepening to

economic growth and for financial sophistication, the causality is

bi-directional but negative. As some studies have concluded, we have not found

any evidence of the link between credit allocation and economic growth and even

if the relationship was to be significant, it would be negative. This is

explained by the pattern of the credit to private sector which has become

increasingly skewed to service sector with less employment and loan defaulters

rather than to agriculture and businesses for productive investments.

All in all, we found that the level of financial development

matters most for Rwandan economy, contrary to the irrelevance of the financial

development on economic growth in cross-sectional analysis for developing

countries confirmed by previous studies. The reason being that their analysis

does not take into consideration country's unique characteristics or the

results are biased by the presence of outliers in their regression, due to size

inequalities of countries within a region.

The first and fourth hypotheses were partly confirmed while

the second and third could not be confirmed. The study has attained its

objectives and recommendations for further strengthening both Rwandan financial

sector and Rwandan economy in general have been suggested.

6.2 Policy recommendations

Based on the results of the study, it is urgent that Rwandan

government takes the financial sector as a pillar of economic growth which can

replace non performing industrial sector and agriculture. The emphasis put on

it can allow Rwanda to be the net exporter of financial services within East

African Community and Commonwealth where Rwanda was admitted recently, as we do

not have any comparative advantage in remaining sectors.

The emphasis should be put on the level of financial

intermediation through increase in the credit allocated to private sector. It

is however important to note that the allocation of the credit should be

changed from private consumption and services to agriculture and other

investment projects like construction sector. Additionally, credit allocation

should be based on the profitability of the investment rather than personal

considerations or values.

More so, Rwandan government should accelerate financial

innovations which are currently very low, by making compulsory: distribution of

ATM cards by banks upon bank account opening; and the use of credit cards as a

means of payment in strong legalized supermarkets and shops, as a first step in

the introduction of card-based system of payment.

BPR S.A has provided evidence that bank branch proximity is a

key factor in bank profitability. It is therefore, recommended that other

commercial banks in Rwanda should open at least one branch in each district.

Due to the absence of positive impact of financial innovations on economic

growth explained by inflationary pressures and exchange rate depreciation, the

Government of Rwanda should put more efforts on price and exchange rate

stability.

The introduction of OTC market was a good step for financial

development. However, a lot need to be done regarding empowering the saving

capacity of Rwandans, by policy measures enhancing an equal distribution of

income, poverty eradication and the fight against rampant unemployment. We

believe these factors to have been the reasons for the absence of transactions

on OTC market rather than lack of public awareness as reported by

newspapers.

For employed population, the government of Rwanda should

ensure that the salary is enough to cover the subsistence needs so that saving

is possible. This can be done through the minimum wage legislation since a

larger group of employed people earn even what is not enough for family

expenses. In such conditions, any policy aimed at saving mobilization would

futile.

We can not claim that the study has explored all areas of the

problem. For instance, we have not used the level of stock market development

in our econometric analysis due to lack of data as the existing OTC started in

2008.

6.3 Areas for further research

Studies need to be conducted to determine best proxies of

financial development in Rwanda, especially for financial innovations, as the

used ratio of M2 to M1 may reflect the increase in classical saving functions

rather than diversification of financial instruments and use of modern

technology in the financial sector. Indeed, a cross-sectional study in EAC

would be interesting, to assess how developed financial systems are and how

they are relevant to economic growth.

Financial Development and Economic Growth in Rwanda

REFERENCES

1. Abebe, A. (1990), «Financial Repression and its

Impact on Financial development and Economic Growth in the African Least

Developed Countries", Savings and Development, no1, X1V, pp. 23-55.

2. Alison, T., Geda, A., Le Billon, P., Murshed, S.M. (2001),

«Financial Reconstruction in Conflict and 'Post-Conflict'

Economies", Paper presented at the Conference of the Finance and

Development Research Programme, pp. 5-6.

3. Beck, T., Demirguc-Kunt, A. and Maksimovic, V. (2006),

«Financing Patterns around the World: Are Small Firms

Different?", World Bank mimeo.

4. Bodie. Z, Kane A. and Marcus A. (2008), Essentials of

Investments, McGraw -Hill International ed, 7ed, New York, USA

5. Brooks, C.(2008), "Introductory Econometrics for

Finance", 2nd ed, The ICMA Centre, University of Reading,

Cambridge University Press

6. Buffie, E. F. (1984), «Financial Repression: The

New Structuralist and Stabilization, Policy in Semi-industrialized

economies", Journal of Economic Development, 14,3, pp. 303-322.

7. Cameron, R. (1961), «France and Economic Development

in Europe", Princeton University Press, Princeton, NJ.

8. CIA World Factbooks, 2003-2008,

www.cia.gov

9. CMAC, www,

cmac.gov.rw

10. Demetriades, P.O and Luintel, K.B (1996),

«Financial Development, Economic Growth and Banking Sector Controls:

Evidence from India", The Economic Journal, The Journal of the Royal

Economic Society, pp. 359- 374.

11. Demirgüç-Kunt, A. and Maksimovic, V. (1998),

«Law, Finance, and Firm Growth", Journal of Finance 53,

pp. 2107-2137.

12. Diaz-Alejandro, C.(1985), «Good-bye Financial

Repression, Hello Financial Crisis", Journal of Development Economics, 19

(1/2), 1-24.

13. Douglas, K. (2003), «The Finance Growth Nexus:

Evidence from Sub-Saharan Africa", IAER: May 2003, Vol. 9, no. 2.

14. Dushimumukiza, D. (2006), «Correlation entre le Taux de

Change et la Balance des Paiements», UNR, Huye-Rwanda, Unpublished

Dissertation.

15.

Firdu, G. and Struthers, J. (2003), «The

McKinnon-Shaw Hypothesis: Thirty Years on: A Review of Recent Developments in

Financial Liberalization Theory", Paper presented at DSA Annual Conference

on «Globalisation and Development», Glasgow, Scotland, September

2003.

16. Friedman, M. and Schwartz, A.J. (1963), «A Monetary

History of United States, Princeton», Princeton University press

17. Fry, M.J. (1989), «Financial development: Theories

and recent experience", Oxford Review of Economic policy, vol 5 no 4

18. Fry, M.J. (1997), «In Favour of Financial

liberalization", The Economic Journal, Vol. 107, No. 442, pp.754-770.

19. Gebhard, K. and Wolters, J.(2007), «Introduction to

Modern Time series", Springer-Verlag Berlin Heidelberg.

20. Greenwood, J. and Jovanovic, B. (1990), «Financial

Development and the Development of Income"; Journal of political economy,

Vol. 98

21. Gujarati, D. (2004), «Basic Econometrics",

4th edition, The MacGraw-Hill companies.