The impact of monetary policy on consumer price index (CPI): 1985-2010( Télécharger le fichier original )par Sylvie NIBEZA Kigali Independent University (ULK) - Master Degree 2014 |

CHAPTER 2: LITERATURE REVIEWIntroductionThis chapter refers to defining the key words used in the work in order to facilitate the interested reader to have the same understanding with the authors about such important concepts. It is also aimed at analyzing and putting in place all theories made by different authors, scholars and researchers and it facilitate to understand the different relationship between terms or concepts of the topic in order to understand deeply this topic which is the monetary policy on CPI. According to Monetary Theory, Monetary Policy manipulates the money supply and rate of interest in such a way to achieve the goals of the manifestation of the ruling party (Shoaib k, 2010). Monetary Policy provides a logical relationship between its variables stipulated to affects the outcomes regarding the Central Bank applies these tools to regulate the money creation, targeting the rate of interest to manage the pace of monetary circulation. The objective is to stabilize internal and external value of the currency (Wikipedia, Monetary policy September, 2014). In present times wide range monetary decisions are required such as short term and long term interest rates; velocity of money; exchange rates; bonds and equities. They will also have to look into the government and private expenditure; savings; inflows of capital and other financial derivatives (Wikipedia, Monetary policy September, 2014). Many scholars who have investigated on the effect of monetary policy have come up with varieties of remedial steps. Tailor (1963) studied the interest rate effect of monetary transmission mechanism and Observed that contractionary monetary policy leads to a rise in domestic real interest rates, raises cost of capital, thereby causing a fall in investment spending and a decline in output. Ozme (1998) adopted a simplified Ordinary Least Square techniques in his analysis on monetary policy and macroeconomic stabilization in Nigeria and found out that interest rate has an insignificant influence on price stability. Killick and Mwega (1990:3) recapitulated traditional monetary policy goals to include price stability, promoting growth, achieving full employment, smoothing the business cycle, preventing financial crises, and stabilizing long-term interest rates and the real exchange rate. Genev (2002) studied the effects of monetary shocks in 10 Central and Eastern European (CEE) countries and found some indication that changes in the Exchange rate affects output but no evidence that suggests that changes in interest rate affect output. Balogun (2007) used simultaneous equation model in testing the hypothesis of effectiveness of monetary policy in Nigeria, and found out that rather than promote growth, domestic monetary policy was a source of stagnation and persistent inflation. Okwo and Nwoha (2010) examined the effect of monetary policy outcomes on macroeconomic stability in Nigeria using a simplified Ordinary least square technique stated in multiple forms. They found out that there exists an insignificant relationship between monetary policy, gross domestic product, credit to private sector and inflation in Nigeria.

Omoke and Ugwuanyi (2010) in their long - run study of money, prices and output in Nigeria found out that there exists no co-integrating vector but however proved that money supply granger causes both output and inflation. Thus, suggest that monetary stability can contribute towards price stability since inflation in Nigeria is a monetary phenomenon. Nwosa (2011) in his appraisal of monetary policy development in Nigeria, examined the effect of monetary policy on macroeconomic variables using an Ordinary Least Square technique after conducting the unit root, co -integration tests revealed that monetary policy has a significant effect on exchange rate and an insignificant influence on price stability.

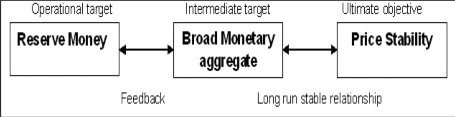

Government policies, including monetary policy, affect the growth of domestic output to the extent that they affect the quantity and productivity of capital and labor. Monetary policy is only one element of overall macroeconomic policy, and can only affect the production process through its impact on interest rates. There are two main channels of monetary policy. One is through the effect that interest rate changes have on the exchange rate of a currency, and the other is through the effect that interest rate changes have on demand. Therefore monetary policy has an impact on economic activity and growth through the workings of foreign and domestic markets for goods and services (Boweni, 2000) The instrument of monetary policy ought to be the short term interest rate, that policy should be focused on the control of inflation, and that inflation can be reduced by increasing short term interest rates (Alvarez, 2001). Kuttner and Mosser (2002) indicated that monetary policy affects the economy through several Transmission mechanisms such as the interest rate channel, the exchange rate channel, Tobin's q theory, the wealth effect, the monetarist channel, and the credit channels including the bank lending channel and the balance-sheet channel. But mainly monetary policy plays its role in controlling inflation through money supply and interest rate. Money Supply (M2) would affect real GDP positively because an increase in real quantity of money causes the nominal interest rate to decline and real output to rise (Hsing, 2005). Friedman (1963) emphasizes money supply as the key factor affecting the wellbeing of the economy. Thus, in order to promote steady growth rate, the money supply should grow at a fixed rate, instead of being regulated and altered by the monetary authority. After the Great Depression, JM Keynes who advocates for demand management policies, for the first time recognized the direct effect of money supply on the economic health of a nation. He also argues for intervention of the Central Bank to operate monetary policy to stabilize the economy (Shoaibk, 2010). The concepts defined in this study are: Consumer Price Index, Nominal Interest Rate, Money Supply and Exchange rate. 2.1 Theory of Monetary PolicyMonetary policy is the process by which the government, Central bank or monetary authority of a country controls: (i) the supply of money, (ii) availability of money, and (iii) cost of money or rate of interest to attain a set of objectives oriented towards the growth and stability of the economy. Monetary theory provides insight into how to craft optimal monetary policy. Monetary policy rests on the relationship between the rates of interest in an economy, that is the price at which money can be borrowed, and the total supply of money. Monetary policy uses a variety of tools to control one or both of these, to influence outcomes like economic growth, inflation, exchange rates with other currencies. Where currency is under a monopoly of issuance, or where there is a regulated system of issuing currency through banks which are tied to a Central bank, the monetary authority has the ability to alter the money supply and thus influence the interest rate (to achieve policy goals). If policymakers believe that private agents anticipate low inflation, they have an incentive to adopt an expansionist monetary policy (where the marginal benefit of increasing economic output outweighs the marginal cost of inflation); however, assuming private agents have rational expectations, they know that policymakers have this incentive. Hence, private agents know that if they anticipate low inflation, an expansionist policy will be adopted that causes a rise in inflation. Consequently, (unless policymakers can make their announcement of low inflation credible), private agents expect high inflation. This anticipation is fulfilled through adaptive expectation (wage-setting behavior); so, there is higher inflation (without the benefit of increased output). Hence, unless credible announcements can be made, expansionary monetary policy will fail. While a Central bank might have a favorable reputation due to good performance in conducting monetary policy, the same Central bank might not have chosen any particular form of commitment (such as targeting a certain range for inflation). Reputation plays a crucial role in determining how much markets would believe the announcement of a particular commitment to a policy goal but both concepts should not be assimilated. Also, note that under rational expectations, it is not necessary for the policymaker to have established its reputation through past policy actions; as an example, the reputation of the head of the Central bank might be derived entirely from his or her ideology, professional background, public statements. In fact it has been argued that to prevent some pathology related to the time inconsistency of monetary policy implementation (in particular excessive inflation), the head of a Central bank should have a larger distaste for inflation than the rest of the economy on average. Hence the reputation of a particular Central bank is not necessary tied to past performance, but rather to particular institutional arrangements that the markets can use to form inflation expectations. Despite the frequent discussion of credibility as it relates to monetary policy, the exact meaning of credibility is rarely defined. Such lack of clarity can serve to lead policy away from what is believed to be the most beneficial. For example, capability to serve the public interest is one definition of credibility often associated with Central banks. The reliability which a Central bank keeps its promises is also a common definition. While everyone most likely agrees a Central bank should not lie to the public, wide disagreement exists on how a Central bank can best serve the public interest. Therefore, lack of definition can lead people to believe their supporting one particular policy of credibility when they are really supporting another ( B.M. Friedman, 2001). Before proceeding to review what other researchers have found about relationship of CPI and Money supply, interest rate, and Inflation, we first attempt to explain the importance of monetary policy in light of available literature. Government policies, including monetary policy, affect the growth of domestic output to the extent that they affect the quantity and productivity of capital and labor. Monetary policy is only one element of overall macroeconomic policy, and can only affect the production process through its impact on interest rates. There are two main channels of monetary policy. One is through the effect that interest rate changes have on the exchange rate of a currency, and the other is through the effect that interest rate changes have on demand. Therefore monetary policy has an impact on economic activity and growth through the workings of foreign and domestic markets for goods and services (Boweni, 2000) Kuttner and Mosser (2002) indicated that monetary policy affects the economy through several transmission mechanisms such as the interest rate channel, the exchange rate channel but mainly monetary policy plays its role in controlling inflation through money supply and interest rate. Money Supply (M2) would affect real GDP positively because an increase in real quantity of money causes the nominal interest rate to decline and real output to rise (Hsing, 2005). The National Bank of Rwanda establishes and enforces banking rules that affect monetary policy and the overall level of the competition between different banks. It determines which non-banking activities, such as brokerage services, leasing and insurance, are appropriate for banks and which should be prohibited. The National Bank of Rwanda is also responsible for supervising the central insurance funds that protects the deposits of member institution (O.C. Ferrell et al, 2006). 2.1.1 Transmission of monetary policyThe monetary policy transmission mechanism describes the channels through which changes in monetary policy affect the objective target. It describes how private sector agents respond to the policy actions of the monetary authorities. The channels through which monetary policy are transmitted are varied and complex depending on the financial structure, expectations, openness of the economy and production functions. In the long run the price level is determined solely by the actions of the monetary authorities. This stems from the fact that the central bank alone creates the ultimate means of payments, base money, on which a monetary economy depends. By altering the terms at which this means of payment is provided, the authorities are able to determine the nominal value of transactions in the economy and hence the price level in the long run. To a large extent the debate on the mechanism is centered on the precise temporal impact of monetary shocks on the economy and the means by which such shocks are propagated. The intellectual divide on this issue involves the classical /monetarist school (Friedman, Cagan, Meltzer, MaCallum, Lucas et al) and the Keynesians/Neo-Keynesians such as Grossman, Mankiw and Romer among others. For the case of Rwanda, the transmission of monetary policy can be schematized as follow: Figure 1: Monetary targeting Framework

Source: BNR, Economic Review no3 Based on this figure, the NBR sets base money as an operating target with the intention of changing the intermediate target of any monetary aggregate (money stock in the economy). Indeed monetary aggregate targeting is part of the strategy by which the National Bank of Rwanda chooses the money stock as the nominal anchor for achieving price stability as a final objective. To attain this final objective, the following two requirements are necessary: (i) A stable demand functions for money; (ii) A long-run relationship between the money stock and the price level (Hansen and Kim, 1995:286). |

|