IV.2.3- Selection of developmental indicators for the

informal sector

Within the framework of our research, indicators of informal

sector development related to performance (social and financial) is illustrated

by the number of deposits and the number of gross loans granted by microfinance

institutions, all things being equal (Ceteris Paribus). Table 6 resulting from

table 3 of section III.1.2 on the evolution of the activity of microfinance in

Cameroun from 2002 to 2010 illustrates this situation clearly.

53

Analysis of microfinances' performance and

development of informal institutions in Cameroon

By Djamaman Brice Gaétan

Table 6: evolution of fixed deposits and gross loan

from 2002 to 2010

|

Years

|

2002

|

2003

|

2004

|

2005

|

2006

|

2007

|

2008

|

2010

|

|

Fixed deposits

|

66727

|

55769

|

98743

|

116840

|

162427

|

194830

|

258220

|

373872

|

|

Gross loan

|

44748

|

56077

|

65402

|

70795

|

104173

|

117233

|

138523

|

221378

|

Source COBAC

Under to this table, we obtained the following figure:

Figure2: Evolution of fixed deposits and gross loan

from 2002 to 2010

|

400000 350000 300000 250000 200000 150000 100000

50000

0

|

|

|

|

|

Fixed deposits and goss loan

|

|

Years

Fixed deposit* Gross loan*

|

1 2 3 4 5 6 7 8

Years

*in Million FCFA

The observation of the figure shows that deposits and gross

loans change in the same direction, but the increase in gross loans is less

proportional than bank deposits. In the first year, there was a slight increase

in savings from the credit to this sector. In year 2, the amount of deposits is

substantially equal to the credits, but with a slight decrease with respect to

savings. Then the situation changes proportionally to year 5 where we observe

that the volume of savings has significantly increased (in reference to the

year 1), and this is due to the proliferation of small and medium enterprises

which promotes the mobilization of a large volume of informal savings.

Subsequently, the position of deposits and loans is growing exponentially until

reaching in 2010 the respective amounts of 373,872 million and 221,378

million.

54

Analysis of microfinances' performance and

development of informal institutions in Cameroon

By Djamaman Brice Gaétan

IV.2.4- Selection of the control variables

For reasons of robustness, three control variables are used in

the regression explaining the performance (both social and financial) of MFIs,

namely: Total Asset, Coefficient of Activity and Hedge Loans by Available

Resources.

Those indicators have been chosen with reference to the

research environment. In fact, and in spite of scarcity of data, the control

variables reflect perfectly and respectively the capital structure, a day to

day activities and available resources of the MFIs environment

IV.3- The research hypothesis and research model

In this section, we are going to

give guidelines about the formulation of research hypothesis.

Firstly, the research concentrates on the financial

performance of MFIs. The general assumption under this hypothesis (H1) is that:

social performance influences financial performance of MFIs. This

hypothesis can be subdivided into two categories as follows:

? Positive link, H1a: «influence of social

performance on financial performance implies a good management of

MFI»;

? Negative link, H1b: «influence of social

performance on financial performance implies arbitration». This

hypothesis means that any socially responsible initiative moves away the

leaders from their objective for profit maximization (this hypothesis lead to

the occurrence of mission drift by MFIs)

Secondly the research focuses on hypothesis two (H2) which

assumes that: «financial performance influences social

performance». As we have undertaken in the first hypothesis, the

second can also be subdivided into two categories such as positive and negative

links

? Positive link, H2a: «good financial performance

enables the firm to allocate some margin to social issues» this

hypothesis implies the availability of fund by the microfinance institution.

Thus, an allowance resulting from good economic figures brings in an

improvement of SP

? Negative link, H2b: «financially powerful companies

are the worse in terms of SP because of their leaders' greed, who do not share

the margin»

55

Analysis of microfinances' performance and

development of informal institutions in Cameroon

By Djamaman Brice Gaétan

Apart from the above hypothesis, it is important to remember

that our study takes into consideration not only social and financial aspects,

but also the relationship between these aspects and development of informal

institutions in Cameroon. Indeed we have included some variables in our

research which are correlated to the development of the informal sector. The

aforesaid variables are Fixed Deposit and Gross Loan.

Consequently, in a bid to reach one of our objectives (which

is to show the relationship between microfinance performance and the

development of non-formal institutions) we have stated another hypothesis as

follows:

? 113: «financial performance influences the

development of informal sector»

The idea behind this hypothesis is that the improvement of

financial performance indicators could contribute to increase the fixed deposit

and gross loan of MFIs. The latter allowing the measurement of the growth of

small and medium size enterprises, ceteris paribus.

? 114: «social performance influences the development

of the informal sector»

This hypothesis implies that more contact of MFIs with the

poorest population (those who cannot access to the classical bank system) will

contribute to improve the amount of fixed deposits and gross loan.

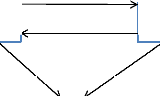

Figure 3: Summary of research

hypothesis

SOCIAL

PERFORMANCE

FINAACIAL

PERFORMANCE

H1

H2

H4 H3

DEVELOPMENT OF

INFORMAL SECTOR

|