LES ANNEXES

ANNEXE 1 : TABLEAUX DES DONNEES

Données des variables

macroéconomiques

|

Année

|

Taux de croissance du PIB réel (en %)

|

Taux d'inflation (en %)

|

|

2000

|

5,2

|

1

|

|

2001

|

4,7

|

4,5

|

|

2002

|

4

|

2,8

|

|

2003

|

4,2

|

0,6

|

|

2004

|

3,7

|

0,3

|

|

2005

|

2,3

|

1,9

|

|

2006

|

3,2

|

5,1

|

|

2007

|

3,9

|

1,1

|

|

2008

|

3,5

|

5,3

|

Source : BEAC

Données des variables

macro-financières

|

Année

|

ACTFPIB

|

CONC (%)

|

|

2000

|

0,159

|

56,48

|

|

2001

|

0,169

|

57,36

|

|

2002

|

0,188

|

53,83

|

|

2003

|

0,184

|

51,72

|

|

2004

|

0,186

|

52,85

|

|

2005

|

0,197

|

54,22

|

|

2006

|

0,206

|

54,92

|

|

2007

|

0,224

|

50,28

|

|

2008

|

0,221

|

48,35

|

Sources : Rapports annuels COBAC et BEAC,

2000-2008

Données des variables

managériales

|

Année

|

FGACTF

|

KXACTF

|

LOGACTF

|

IHHP

|

|

2000

|

0,036

|

0,063

|

13,91

|

0,473

|

|

2001

|

0,039

|

0,069

|

14

|

0,494

|

|

2002

|

0,039

|

0,062

|

14,17

|

0,494

|

|

2003

|

0,041

|

0,067

|

14,19

|

0,488

|

|

2004

|

0,041

|

0,066

|

14,25

|

0,495

|

|

2005

|

0,04

|

0,067

|

14,36

|

0,491

|

|

2006

|

0,038

|

0,076

|

14,47

|

0,482

|

|

2007

|

0,036

|

0,07

|

14,61

|

0,474

|

|

2008

|

0,036

|

0,063

|

14,7

|

0,468

|

Sources : Rapports annuels COBAC, 2000-2008

Les données relatives au rendement des

actifs

|

Année

|

Résultat net (en millions)

|

Total actif (en millions)

|

ROA (en %)

|

|

2000

|

12531

|

1 096 049

|

0,011

|

|

2001

|

14581

|

1 200 984

|

0,012

|

|

2002

|

19785

|

1 426 885

|

0,014

|

|

2003

|

22213

|

1 460 639

|

0,015

|

|

2004

|

21111

|

1 548 205

|

0,014

|

|

2005

|

21772

|

1 727 979

|

0,013

|

|

2006

|

23868

|

1 931 226

|

0,012

|

|

2007

|

25678

|

2 212 430

|

0,012

|

|

2008

|

26411

|

2 424 883

|

0,011

|

Sources : Rapports annuels COBAC, 2000-2008

ANNEXE 2 : TEST DE NORMALITE

|

ACTFPIB

|

CONC

|

FGACTF

|

IHHP

|

RISK

|

|

Mean

|

0.189486

|

52.70694

|

0.047698

|

0.473141

|

0.000852

|

|

Median

|

0.186938

|

53.46500

|

0.039000

|

0.487878

|

0.000707

|

|

Maximum

|

0.223625

|

57.66875

|

0.386250

|

0.494380

|

0.004093

|

|

Minimum

|

0.138125

|

30.21875

|

0.022500

|

0.182702

|

2.70E-05

|

|

Std. Dev.

|

0.021281

|

4.893847

|

0.058135

|

0.054728

|

0.000729

|

|

Skewness

|

-0.168135

|

-2.969473

|

5.715903

|

-4.576654

|

2.597589

|

|

Kurtosis

|

2.597712

|

13.87508

|

33.80187

|

23.89186

|

12.00293

|

|

|

|

|

|

|

|

Jarque-Bera

|

0.412369

|

2.303075

|

1.619162

|

0.780792

|

1.620640

|

|

Probability

|

0.813683

|

0.279615

|

0.696712

|

0.660602

|

0.656613

|

|

|

|

|

|

|

|

Observations

|

36

|

36

|

36

|

36

|

36

|

|

INF

|

KXACTF

|

LOGACTF

|

PIB

|

ROA

|

|

Mean

|

2.450000

|

0.066292

|

14.08917

|

3.794444

|

0.012663

|

|

Median

|

2.418750

|

0.066500

|

14.22000

|

3.831250

|

0.012688

|

|

Maximum

|

4.775000

|

0.075250

|

14.68875

|

5.137500

|

0.014875

|

|

Minimum

|

0.337500

|

0.039375

|

9.187500

|

2.187500

|

0.006875

|

|

Std. Dev.

|

1.407632

|

0.005965

|

0.902934

|

0.784313

|

0.001599

|

|

Skewness

|

0.107683

|

-2.539879

|

-4.658385

|

-0.156421

|

-1.258986

|

|

Kurtosis

|

1.745570

|

12.98526

|

25.65109

|

2.340528

|

6.007051

|

|

|

|

|

|

|

|

Jarque-Bera

|

2.429965

|

1.882640

|

0.998109

|

0.799160

|

2.307381

|

|

Probability

|

0.296715

|

0.766714

|

0.967168

|

0.670602

|

0.266710

|

|

|

|

|

|

|

|

Observations

|

36

|

36

|

36

|

36

|

36

|

ANNEXE 3 : TEST DE STATIONNARITE

ROA, à la différence première avec trend et

constante (stationnaire)

|

ADF Test Statistic

|

-4.881427

|

1% Critical Value*

|

-4.2605

|

|

|

5% Critical Value

|

-3.5514

|

|

|

10% Critical Value

|

-3.2081

|

|

*MacKinnon critical values for rejection of hypothesis of a unit

root.

|

|

|

|

|

|

|

|

|

|

|

|

Augmented Dickey-Fuller Test Equation

|

|

Dependent Variable: D(ROA1)

|

|

Method: Least Squares

|

|

Date: 06/15/10 Time: 15:41

|

|

Sample(adjusted): 2000:4 2008:4

|

|

Included observations: 33 after adjusting endpoints

|

|

Variable

|

Coefficient

|

Std. Error

|

t-Statistic

|

Prob.

|

|

ROA1(-1)

|

-1.606906

|

0.329188

|

-4.881427

|

0.0000

|

|

D(ROA1(-1))

|

0.213195

|

0.195701

|

1.089395

|

0.2849

|

|

C

|

0.000840

|

0.000298

|

2.814644

|

0.0087

|

|

@TREND(2000:1)

|

-5.30E-05

|

1.46E-05

|

-3.638346

|

0.0011

|

|

R-squared

|

0.629308

|

Mean dependent var

|

-6.44E-05

|

|

Adjusted R-squared

|

0.590961

|

S.D. dependent var

|

0.001146

|

|

S.E. of regression

|

0.000733

|

Akaike info criterion

|

-11.48634

|

|

Sum squared resid

|

1.56E-05

|

Schwarz criterion

|

-11.30495

|

|

Log likelihood

|

193.5246

|

F-statistic

|

16.41069

|

|

Durbin-Watson stat

|

1.102513

|

Prob(F-statistic)

|

0.000002

|

IHHP, à la différence quatrième sans

trend et constante (stationnaire)

|

ADF Test Statistic

|

-2.582002

|

1% Critical Value*

|

-2.6423

|

|

|

5% Critical Value

|

-1.9526

|

|

|

10% Critical Value

|

-1.6216

|

|

*MacKinnon critical values for rejection of hypothesis of a unit

root.

|

|

|

|

|

|

|

|

|

|

|

|

Augmented Dickey-Fuller Test Equation

|

|

Dependent Variable: D(IHHP4)

|

|

Method: Least Squares

|

|

Date: 06/15/10 Time: 14:53

|

|

Sample(adjusted): 2001:3 2008:4

|

|

Included observations: 30 after adjusting endpoints

|

|

Variable

|

Coefficient

|

Std. Error

|

t-Statistic

|

Prob.

|

|

IHHP4(-1)

|

-2.880338

|

1.115544

|

-2.582002

|

0.0153

|

|

D(IHHP4(-1))

|

0.483892

|

1.094862

|

0.441966

|

0.6619

|

|

R-squared

|

0.849805

|

Mean dependent var

|

0.005159

|

|

Adjusted R-squared

|

0.844440

|

S.D. dependent var

|

0.052391

|

|

S.E. of regression

|

0.020664

|

Akaike info criterion

|

-4.856546

|

|

Sum squared resid

|

0.011956

|

Schwarz criterion

|

-4.763133

|

|

Log likelihood

|

74.84819

|

F-statistic

|

158.4238

|

|

Durbin-Watson stat

|

2.013657

|

Prob(F-statistic)

|

0.000000

|

KXACTF, à la différence deuxième sans

trend ni constante (stationnaire)

|

ADF Test Statistic

|

-1.959162

|

1% Critical Value*

|

-2.6369

|

|

|

5% Critical Value

|

-1.9517

|

|

|

10% Critical Value

|

-1.6213

|

|

*MacKinnon critical values for rejection of hypothesis of a unit

root.

|

|

|

|

|

|

|

|

|

|

|

|

Augmented Dickey-Fuller Test Equation

|

|

Dependent Variable: D(KXACTF2)

|

|

Method: Least Squares

|

|

Date: 06/15/10 Time: 15:02

|

|

Sample(adjusted): 2001:1 2008:4

|

|

Included observations: 32 after adjusting endpoints

|

|

Variable

|

Coefficient

|

Std. Error

|

t-Statistic

|

Prob.

|

|

KXACTF2(-1)

|

-0.556716

|

0.284160

|

-1.959162

|

0.0594

|

|

D(KXACTF2(-1))

|

0.443284

|

0.284160

|

1.559982

|

0.1293

|

|

R-squared

|

0.080269

|

Mean dependent var

|

-0.000289

|

|

Adjusted R-squared

|

0.049611

|

S.D. dependent var

|

0.001519

|

|

S.E. of regression

|

0.001480

|

Akaike info criterion

|

-10.13259

|

|

Sum squared resid

|

6.57E-05

|

Schwarz criterion

|

-10.04098

|

|

Log likelihood

|

164.1215

|

F-statistic

|

2.618220

|

|

Durbin-Watson stat

|

1.984043

|

Prob(F-statistic)

|

0.116110

|

FGACTF, à la différence troisième avec

trend et constante (stationnaire)

|

ADF Test Statistic

|

-5.902610

|

1% Critical Value*

|

-4.2826

|

|

|

5% Critical Value

|

-3.5614

|

|

|

10% Critical Value

|

-3.2138

|

|

*MacKinnon critical values for rejection of hypothesis of a unit

root.

|

|

|

|

|

|

|

|

|

|

|

|

Augmented Dickey-Fuller Test Equation

|

|

Dependent Variable: D(FGACTF3)

|

|

Method: Least Squares

|

|

Date: 06/15/10 Time: 15:09

|

|

Sample(adjusted): 2001:2 2008:4

|

|

Included observations: 31 after adjusting endpoints

|

|

Variable

|

Coefficient

|

Std. Error

|

t-Statistic

|

Prob.

|

|

FGACTF3(-1)

|

-1.129047

|

0.191279

|

-5.902610

|

0.0000

|

|

D(FGACTF3(-1))

|

-0.001355

|

0.002676

|

-0.506470

|

0.6166

|

|

C

|

0.000456

|

0.000397

|

1.148972

|

0.2606

|

|

@TREND(2000:1)

|

-3.05E-05

|

1.83E-05

|

-1.669156

|

0.1066

|

|

R-squared

|

0.577076

|

Mean dependent var

|

4.03E-05

|

|

Adjusted R-squared

|

0.530085

|

S.D. dependent var

|

0.001203

|

|

S.E. of regression

|

0.000825

|

Akaike info criterion

|

-11.24252

|

|

Sum squared resid

|

1.84E-05

|

Schwarz criterion

|

-11.05749

|

|

Log likelihood

|

178.2590

|

F-statistic

|

12.28043

|

|

Durbin-Watson stat

|

2.008125

|

Prob(F-statistic)

|

0.000030

|

LOGACTF, à la différence septième avec

trend et constante (stationnaire)

|

ADF Test Statistic

|

-4.480666

|

1% Critical Value*

|

-4.3382

|

|

|

5% Critical Value

|

-3.5867

|

|

|

10% Critical Value

|

-3.2279

|

|

*MacKinnon critical values for rejection of hypothesis of a unit

root.

|

|

|

|

|

|

|

|

|

|

|

|

Augmented Dickey-Fuller Test Equation

|

|

Dependent Variable: D(LOGACTF7)

|

|

Method: Least Squares

|

|

Date: 06/15/10 Time: 15:13

|

|

Sample(adjusted): 2002:2 2008:4

|

|

Included observations: 27 after adjusting endpoints

|

|

Variable

|

Coefficient

|

Std. Error

|

t-Statistic

|

Prob.

|

|

LOGACTF7(-1)

|

-6.893965

|

1.538603

|

-4.480666

|

0.0002

|

|

D(LOGACTF7(-1))

|

1.720362

|

1.501365

|

1.145866

|

0.2636

|

|

C

|

0.283567

|

0.227574

|

1.246046

|

0.2253

|

|

@TREND(2000:1)

|

-0.016323

|

0.009995

|

-1.633192

|

0.1160

|

|

R-squared

|

0.961067

|

Mean dependent var

|

0.270787

|

|

Adjusted R-squared

|

0.955989

|

S.D. dependent var

|

1.817898

|

|

S.E. of regression

|

0.381373

|

Akaike info criterion

|

1.045876

|

|

Sum squared resid

|

3.345243

|

Schwarz criterion

|

1.237852

|

|

Log likelihood

|

-10.11932

|

F-statistic

|

189.2540

|

|

Durbin-Watson stat

|

2.123511

|

Prob(F-statistic)

|

0.000000

|

INF, à niveau avec trend et constante (stationnaire)

|

ADF Test Statistic

|

-4.857478

|

1% Critical Value*

|

-4.2505

|

|

|

5% Critical Value

|

-3.5468

|

|

|

10% Critical Value

|

-3.2056

|

|

*MacKinnon critical values for rejection of hypothesis of a unit

root.

|

|

|

|

|

|

|

|

|

|

|

|

Augmented Dickey-Fuller Test Equation

|

|

Dependent Variable: D(INF)

|

|

Method: Least Squares

|

|

Date: 06/15/10 Time: 15:18

|

|

Sample(adjusted): 2000:3 2008:4

|

|

Included observations: 34 after adjusting endpoints

|

|

Variable

|

Coefficient

|

Std. Error

|

t-Statistic

|

Prob.

|

|

INF(-1)

|

-0.234204

|

0.048215

|

-4.857478

|

0.0000

|

|

D(INF(-1))

|

0.907766

|

0.106446

|

8.527911

|

0.0000

|

|

C

|

0.553928

|

0.161041

|

3.439678

|

0.0017

|

|

@TREND(2000:1)

|

-9.77E-05

|

0.006661

|

-0.014664

|

0.9884

|

|

R-squared

|

0.727082

|

Mean dependent var

|

0.064706

|

|

Adjusted R-squared

|

0.699790

|

S.D. dependent var

|

0.674006

|

|

S.E. of regression

|

0.369298

|

Akaike info criterion

|

0.955704

|

|

Sum squared resid

|

4.091426

|

Schwarz criterion

|

1.135276

|

|

Log likelihood

|

-12.24697

|

F-statistic

|

26.64101

|

|

Durbin-Watson stat

|

0.961000

|

Prob(F-statistic)

|

0.000000

|

ACTFPIB, à niveau sans constante ni tendance

(stationnaire)

|

ADF Test Statistic

|

-3.316335

|

1% Critical Value*

|

-2.6321

|

|

|

5% Critical Value

|

-1.9510

|

|

|

10% Critical Value

|

-1.6209

|

|

*MacKinnon critical values for rejection of hypothesis of a unit

root.

|

|

|

|

|

|

|

|

|

|

|

|

Augmented Dickey-Fuller Test Equation

|

|

Dependent Variable: D(ACTFPIB)

|

|

Method: Least Squares

|

|

Date: 05/10/10 Time: 15:27

|

|

Sample(adjusted): 2000:3 2008:4

|

|

Included observations: 34 after adjusting endpoints

|

|

Variable

|

Coefficient

|

Std. Error

|

t-Statistic

|

Prob.

|

|

ACTFPIB(-1)

|

-0.014187

|

0.004278

|

-3.316335

|

0.0023

|

|

D(ACTFPIB(-1))

|

1.841700

|

0.150351

|

12.24936

|

0.0000

|

|

R-squared

|

0.824566

|

Mean dependent var

|

-0.000585

|

|

Adjusted R-squared

|

0.819084

|

S.D. dependent var

|

0.011093

|

|

S.E. of regression

|

0.004718

|

Akaike info criterion

|

-7.817652

|

|

Sum squared resid

|

0.000712

|

Schwarz criterion

|

-7.727866

|

|

Log likelihood

|

134.9001

|

F-statistic

|

150.4052

|

|

Durbin-Watson stat

|

1.894554

|

Prob(F-statistic)

|

0.000000

|

CONC, à la différence quatrième avec

trend et constante (stationnaire)

|

ADF Test Statistic

|

-4.053394

|

1% Critical Value*

|

-4.2949

|

|

|

5% Critical Value

|

-3.5670

|

|

|

10% Critical Value

|

-3.2169

|

|

*MacKinnon critical values for rejection of hypothesis of a unit

root.

|

|

|

|

|

|

|

|

|

|

|

|

Augmented Dickey-Fuller Test Equation

|

|

Dependent Variable: D(CONC4)

|

|

Method: Least Squares

|

|

Date: 06/15/10 Time: 15:25

|

|

Sample(adjusted): 2001:3 2008:4

|

|

Included observations: 30 after adjusting endpoints

|

|

Variable

|

Coefficient

|

Std. Error

|

t-Statistic

|

Prob.

|

|

CONC4(-1)

|

-2.454073

|

0.605437

|

-4.053394

|

0.0004

|

|

D(CONC4(-1))

|

0.317514

|

0.518145

|

0.612790

|

0.5453

|

|

C

|

0.693284

|

0.524127

|

1.322740

|

0.1974

|

|

@TREND(2000:1)

|

-0.043607

|

0.024178

|

-1.803573

|

0.0829

|

|

R-squared

|

0.833607

|

Mean dependent var

|

0.176542

|

|

Adjusted R-squared

|

0.814408

|

S.D. dependent var

|

2.513447

|

|

S.E. of regression

|

1.082803

|

Akaike info criterion

|

3.120548

|

|

Sum squared resid

|

30.48400

|

Schwarz criterion

|

3.307374

|

|

Log likelihood

|

-42.80822

|

F-statistic

|

43.41892

|

|

Durbin-Watson stat

|

1.982389

|

Prob(F-statistic)

|

0.000000

|

PIB, à niveau avec trend et constante (stationnaire)

|

ADF Test Statistic

|

-4.264166

|

1% Critical Value*

|

-4.2505

|

|

|

5% Critical Value

|

-3.5468

|

|

|

10% Critical Value

|

-3.2056

|

|

*MacKinnon critical values for rejection of hypothesis of a unit

root.

|

|

|

|

|

|

|

|

|

|

|

|

Augmented Dickey-Fuller Test Equation

|

|

Dependent Variable: D(PIB)

|

|

Method: Least Squares

|

|

Date: 06/15/10 Time: 15:29

|

|

Sample(adjusted): 2000:3 2008:4

|

|

Included observations: 34 after adjusting endpoints

|

|

Variable

|

Coefficient

|

Std. Error

|

t-Statistic

|

Prob.

|

|

PIB(-1)

|

-0.165958

|

0.038919

|

-4.264166

|

0.0002

|

|

D(PIB(-1))

|

1.079044

|

0.103544

|

10.42110

|

0.0000

|

|

C

|

0.821835

|

0.193218

|

4.253409

|

0.0002

|

|

@TREND(2000:1)

|

-0.011765

|

0.002868

|

-4.101596

|

0.0003

|

|

R-squared

|

0.792362

|

Mean dependent var

|

-0.085294

|

|

Adjusted R-squared

|

0.771599

|

S.D. dependent var

|

0.228456

|

|

S.E. of regression

|

0.109182

|

Akaike info criterion

|

-1.481470

|

|

Sum squared resid

|

0.357621

|

Schwarz criterion

|

-1.301898

|

|

Log likelihood

|

29.18498

|

F-statistic

|

38.16083

|

|

Durbin-Watson stat

|

1.159024

|

Prob(F-statistic)

|

0.000000

|

Risk, à la différence troisième avec

trend et constante (stationnaire)

|

ADF Test Statistic

|

-5.027815

|

1% Critical Value*

|

-4.2826

|

|

|

5% Critical Value

|

-3.5614

|

|

|

10% Critical Value

|

-3.2138

|

|

*MacKinnon critical values for rejection of hypothesis of a unit

root.

|

|

|

|

|

|

|

|

|

|

|

|

Augmented Dickey-Fuller Test Equation

|

|

Dependent Variable: D(RISK3)

|

|

Method: Least Squares

|

|

Date: 06/15/10 Time: 15:35

|

|

Sample(adjusted): 2001:2 2008:4

|

|

Included observations: 31 after adjusting endpoints

|

|

Variable

|

Coefficient

|

Std. Error

|

t-Statistic

|

Prob.

|

|

RISK3(-1)

|

-1.482924

|

0.294944

|

-5.027815

|

0.0000

|

|

D(RISK3(-1))

|

0.142920

|

0.163239

|

0.875523

|

0.3890

|

|

C

|

-0.000104

|

0.000105

|

-0.987902

|

0.3320

|

|

@TREND(2000:1)

|

7.01E-06

|

4.80E-06

|

1.461483

|

0.1554

|

|

R-squared

|

0.753789

|

Mean dependent var

|

-3.37E-05

|

|

Adjusted R-squared

|

0.726432

|

S.D. dependent var

|

0.000456

|

|

S.E. of regression

|

0.000238

|

Akaike info criterion

|

-13.72523

|

|

Sum squared resid

|

1.53E-06

|

Schwarz criterion

|

-13.54020

|

|

Log likelihood

|

216.7411

|

F-statistic

|

27.55403

|

|

Durbin-Watson stat

|

1.916145

|

Prob(F-statistic)

|

0.000000

|

ANNEXE 4 : LES ESTIMATIONS

Estimation 1 : avec toutes les variables stationnaires

|

Dependent Variable: ROA1

|

|

Method: Least Squares

|

|

Date: 06/17/10 Time: 18:53

|

|

Sample(adjusted): 2001:4 2008:4

|

|

Included observations: 29 after adjusting endpoints

|

|

Variable

|

Coefficient

|

Std. Error

|

t-Statistic

|

Prob.

|

|

C

|

8.73E-05

|

0.000572

|

0.152576

|

0.8803

|

|

IHHP4

|

0.004469

|

0.013627

|

0.327984

|

0.7465

|

|

KXACTF2

|

0.059171

|

0.043182

|

1.370249

|

0.1866

|

|

FGACTF3

|

0.198470

|

0.204089

|

0.972470

|

0.3430

|

|

LOGACTF7

|

-0.000471

|

0.000264

|

-1.781862

|

0.0908

|

|

INF

|

8.13E-05

|

2.67E-05

|

3.049296

|

0.0066

|

|

ACTFPIB

|

-0.007244

|

0.002458

|

-2.947055

|

0.0083

|

|

CONC4

|

7.23E-05

|

9.74E-05

|

0.742725

|

0.4667

|

|

PIB

|

0.000311

|

6.37E-05

|

4.880711

|

0.0001

|

|

RISK3

|

-0.176354

|

0.174930

|

-1.008139

|

0.3261

|

|

R-squared

|

0.949423

|

Mean dependent var

|

-0.000185

|

|

Adjusted R-squared

|

0.925465

|

S.D. dependent var

|

0.000621

|

|

S.E. of regression

|

0.000170

|

Akaike info criterion

|

-14.25992

|

|

Sum squared resid

|

5.46E-07

|

Schwarz criterion

|

-13.78844

|

|

Log likelihood

|

216.7689

|

F-statistic

|

39.62927

|

|

Durbin-Watson stat

|

0.890045

|

Prob(F-statistic)

|

0.000000

|

Estimation 2 : sans la variable FGACTF

|

Dependent Variable: ROA1

|

|

Method: Least Squares

|

|

Date: 06/17/10 Time: 19:05

|

|

Sample(adjusted): 2001:4 2008:4

|

|

Included observations: 29 after adjusting endpoints

|

|

Variable

|

Coefficient

|

Std. Error

|

t-Statistic

|

Prob.

|

|

C

|

2.28E-05

|

0.000568

|

0.040105

|

0.9684

|

|

IHHP4

|

0.014656

|

0.008704

|

1.683919

|

0.1077

|

|

KXACTF2

|

0.074995

|

0.039945

|

1.877486

|

0.0751

|

|

LOGACTF7

|

-0.000668

|

0.000170

|

-3.934491

|

0.0008

|

|

INF

|

8.23E-05

|

2.66E-05

|

3.093779

|

0.0057

|

|

ACTFPIB

|

-0.007038

|

0.002446

|

-2.877894

|

0.0093

|

|

CONC4

|

7.73E-05

|

9.71E-05

|

0.795942

|

0.4354

|

|

PIB

|

0.000317

|

6.32E-05

|

5.014062

|

0.0001

|

|

RISK3

|

-0.169220

|

0.174539

|

-0.969527

|

0.3439

|

|

R-squared

|

0.946905

|

Mean dependent var

|

-0.000185

|

|

Adjusted R-squared

|

0.925668

|

S.D. dependent var

|

0.000621

|

|

S.E. of regression

|

0.000169

|

Akaike info criterion

|

-14.28031

|

|

Sum squared resid

|

5.73E-07

|

Schwarz criterion

|

-13.85598

|

|

Log likelihood

|

216.0646

|

F-statistic

|

44.58577

|

|

Durbin-Watson stat

|

0.946583

|

Prob(F-statistic)

|

0.000000

|

Estimation 3 : sans les variables FGACTF et Risk

|

Dependent Variable: ROA1

|

|

Method: Least Squares

|

|

Date: 06/20/10 Time: 07:30

|

|

Sample(adjusted): 2001:4 2008:4

|

|

Included observations: 29 after adjusting endpoints

|

|

Variable

|

Coefficient

|

Std. Error

|

t-Statistic

|

Prob.

|

|

C

|

-2.10E-05

|

0.000565

|

-0.037133

|

0.9707

|

|

IHHP4

|

0.017287

|

0.008258

|

2.093443

|

0.0486

|

|

KXACTF2

|

0.080683

|

0.039455

|

2.044946

|

0.0536

|

|

LOGACTF7

|

-0.000696

|

0.000167

|

-4.173046

|

0.0004

|

|

INF

|

8.32E-05

|

2.66E-05

|

3.133760

|

0.0050

|

|

ACTFPIB

|

-0.006872

|

0.002436

|

-2.820886

|

0.0102

|

|

CONC4

|

5.39E-05

|

9.39E-05

|

0.574340

|

0.5718

|

|

PIB

|

0.000319

|

6.31E-05

|

5.060607

|

0.0001

|

|

R-squared

|

0.944410

|

Mean dependent var

|

-0.000185

|

|

Adjusted R-squared

|

0.925880

|

S.D. dependent var

|

0.000621

|

|

S.E. of regression

|

0.000169

|

Akaike info criterion

|

-14.30335

|

|

Sum squared resid

|

6.00E-07

|

Schwarz criterion

|

-13.92617

|

|

Log likelihood

|

215.3986

|

F-statistic

|

50.96655

|

|

Durbin-Watson stat

|

0.980516

|

Prob(F-statistic)

|

0.000000

|

Estimation 4 : sans la variable LOGACTF

|

Dependent Variable: ROA1

|

|

Method: Least Squares

|

|

Date: 06/17/10 Time: 19:28

|

|

Sample(adjusted): 2001:1 2008:4

|

|

Included observations: 32 after adjusting endpoints

|

|

Variable

|

Coefficient

|

Std. Error

|

t-Statistic

|

Prob.

|

|

C

|

0.000319

|

0.000832

|

0.383188

|

0.7051

|

|

IHHP4

|

-0.027168

|

0.005247

|

-5.178050

|

0.0000

|

|

KXACTF2

|

-0.074214

|

0.049493

|

-1.499476

|

0.1474

|

|

FGACTF3

|

0.843605

|

0.174279

|

4.840540

|

0.0001

|

|

INF

|

3.47E-05

|

3.59E-05

|

0.965160

|

0.3445

|

|

ACTFPIB

|

-0.005389

|

0.003418

|

-1.576571

|

0.1286

|

|

CONC4

|

0.000131

|

0.000132

|

0.991669

|

0.3317

|

|

PIB

|

0.000166

|

8.11E-05

|

2.047012

|

0.0522

|

|

RISK3

|

-0.474865

|

0.202210

|

-2.348372

|

0.0278

|

|

R-squared

|

0.895701

|

Mean dependent var

|

-0.000215

|

|

Adjusted R-squared

|

0.859423

|

S.D. dependent var

|

0.000697

|

|

S.E. of regression

|

0.000261

|

Akaike info criterion

|

-13.43074

|

|

Sum squared resid

|

1.57E-06

|

Schwarz criterion

|

-13.01851

|

|

Log likelihood

|

223.8919

|

F-statistic

|

24.68999

|

|

Durbin-Watson stat

|

0.942476

|

Prob(F-statistic)

|

0.000000

|

Estimation 5 : sans les variables LOGACTF et Risk

|

Dependent Variable: ROA1

|

|

Method: Least Squares

|

|

Date: 06/20/10 Time: 07:53

|

|

Sample(adjusted): 2001:1 2008:4

|

|

Included observations: 32 after adjusting endpoints

|

|

Variable

|

Coefficient

|

Std. Error

|

t-Statistic

|

Prob.

|

|

C

|

0.000507

|

0.000903

|

0.561180

|

0.5799

|

|

IHHP4

|

-0.029481

|

0.005617

|

-5.248060

|

0.0000

|

|

KXACTF2

|

-0.100312

|

0.052570

|

-1.908142

|

0.0684

|

|

FGACTF3

|

1.025676

|

0.170133

|

6.028674

|

0.0000

|

|

INF

|

3.83E-05

|

3.91E-05

|

0.979029

|

0.3373

|

|

ACTFPIB

|

-0.005886

|

0.003719

|

-1.582770

|

0.1266

|

|

CONC4

|

0.000141

|

0.000144

|

0.979898

|

0.3369

|

|

PIB

|

0.000138

|

8.74E-05

|

1.576316

|

0.1280

|

|

R-squared

|

0.870693

|

Mean dependent var

|

-0.000215

|

|

Adjusted R-squared

|

0.832978

|

S.D. dependent var

|

0.000697

|

|

S.E. of regression

|

0.000285

|

Akaike info criterion

|

-13.27831

|

|

Sum squared resid

|

1.94E-06

|

Schwarz criterion

|

-12.91188

|

|

Log likelihood

|

220.4530

|

F-statistic

|

23.08633

|

|

Durbin-Watson stat

|

1.037400

|

Prob(F-statistic)

|

0.000000

|

ANNEXE 5 : TEST D'HETEROSCEDASTICITE DES

ERREURS

|

White Heteroskedasticity Test:

|

|

F-statistic

|

1.491479

|

Probability

|

0.262734

|

|

Obs*R-squared

|

21.12954

|

Probability

|

0.272928

|

|

|

|

|

|

|

Test Equation:

|

|

Dependent Variable: RESID^2

|

|

Method: Least Squares

|

|

Date: 08/19/10 Time: 07:22

|

|

Sample: 2001:4 2008:4

|

|

Included observations: 29

|

|

Variable

|

Coefficient

|

Std. Error

|

t-Statistic

|

Prob.

|

|

C

|

-1.08E-06

|

2.53E-06

|

-0.425822

|

0.6793

|

|

IHHP4

|

-7.11E-07

|

4.21E-06

|

-0.169017

|

0.8692

|

|

IHHP4^2

|

0.000151

|

0.000406

|

0.372413

|

0.7174

|

|

KXACTF2

|

1.46E-05

|

8.23E-06

|

1.777133

|

0.1059

|

|

KXACTF2^2

|

-0.004568

|

0.007779

|

-0.587258

|

0.5701

|

|

FGACTF3

|

6.85E-06

|

3.61E-05

|

0.189501

|

0.8535

|

|

FGACTF3^2

|

-0.207467

|

0.170471

|

-1.217027

|

0.2515

|

|

LOGACTF7

|

-1.48E-07

|

9.68E-08

|

-1.529517

|

0.1571

|

|

LOGACTF7^2

|

-8.09E-08

|

1.57E-07

|

-0.516730

|

0.6166

|

|

INF

|

-5.96E-08

|

2.52E-08

|

-2.369706

|

0.0393

|

|

INF^2

|

1.12E-08

|

4.10E-09

|

2.735371

|

0.0210

|

|

ACTFPIB

|

1.43E-05

|

2.59E-05

|

0.551421

|

0.5935

|

|

ACTFPIB^2

|

-3.31E-05

|

6.28E-05

|

-0.526339

|

0.6101

|

|

CONC4

|

-3.93E-09

|

1.12E-08

|

-0.352585

|

0.7317

|

|

CONC4^2

|

7.66E-08

|

5.06E-08

|

1.513429

|

0.1611

|

|

PIB

|

-2.40E-07

|

1.69E-07

|

-1.418325

|

0.1865

|

|

PIB^2

|

3.68E-08

|

2.65E-08

|

1.388151

|

0.1952

|

|

RISK3

|

5.38E-06

|

3.80E-05

|

0.141457

|

0.8903

|

|

RISK3^2

|

0.075130

|

0.123655

|

0.607581

|

0.5570

|

|

R-squared

|

0.728605

|

Mean dependent var

|

1.88E-08

|

|

Adjusted R-squared

|

0.240093

|

S.D. dependent var

|

2.18E-08

|

|

S.E. of regression

|

1.90E-08

|

Akaike info criterion

|

-32.47771

|

|

Sum squared resid

|

3.60E-15

|

Schwarz criterion

|

-31.58190

|

|

Log likelihood

|

489.9268

|

F-statistic

|

1.491479

|

|

Durbin-Watson stat

|

2.839683

|

Prob(F-statistic)

|

0.262734

|

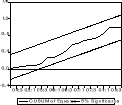

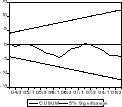

ANNEXE 6 : TEST DE STABILITE

Test de CUSUM square de l'estimation 1

Test de CUSUM de l'estimation 1

Table des matières

Dédicace i

Remerciements

.......................................................................................................................ii

Sommaire iii

Résumé

.....................................................................................................iv

Abstract

.....................................................................................................v

Liste des abréviations

...............................................................................................................

vi

Liste des tableaux

....................................................................................................................

vii

Annexes

........................................................................ .........................viii

Introduction générale

...................................................................................1

Première partie : la

diversification du portefeuille de crédits : une composante

importante de la rentabilité bancaire

....................................................................................................

10

Introduction première partie

............................................................................

11

Chapitre 1 : les déterminants de

la rentabilité bancaire

.............................................. 12

Section 1 : le portefeuille de crédits

diversifié : un déterminant managérial de la

rentabilité des banques

....................................................................................................

12

I - les éléments d'analyse de la gestion bancaire

.................................................................... 13

I 1 - le bilan bancaire : une présentation explicite du

portefeuille de crédits ......................... 13

I 2 - les opérations hors-bilan

.................................................................................................

15

I 3 - le compte de résultat

.......................................................................................................

15

II - les facteurs explicatifs de la rentabilité des

banques ........................................................ 17

II 1 - la gestion prudentielle et la taille de la banque comme

stimulant de la rentabilité bancaire

...................................................................................................................................

17

II 2 - l'explication de la rentabilité bancaire par les

éléments de la marge d'intermédiation bancaire

...................................................................................................................................

18

Section 2 : les déterminants

macroéconomiques et environnementaux de la rentabilité bancaire

...................................................................................................

20

I - les déterminants macroéconomiques

.................................................................................

21

I 1 - l'impact de la croissance économique

............................................................................

21

I 2 - les effets de l'inflation

....................................................................................................

22

II - les déterminants macro-financiers

....................................................................................

22

II 1 - la taille du secteur bancaire

...........................................................................................

23

II 2 - la concentration bancaire

...............................................................................................

23

Chapitre 2 : analyse théorique de

l'impact de la diversification du portefeuille de crédits sur la

rentabilité bancaire

................................................................................

25

Section 1 : la théorie traditionnelle du

portefeuille .................................................. 25

I - l'essence de la théorie de MARKOWITZ

......................................................................... 26

I 1 - l'idée de départ et les hypothèses

...................................................................................

26

I 2 - les études ultérieures

.......................................................................................................

26

II - l'application de la théorie de Markowitz au

portefeuille de crédits ................................. 28

II 1 - l'approche de la diversification géographique du

portefeuille de crédits ...................... 28

II 2 - la diversification par type de crédit et la

rentabilité bancaire ........................................ 30

Section 2 : la théorie de l'intermédiation

financière ................................................ 31

I - l'étude du marché bancaire

................................................................................................

32

I 1 - la banque comme gestionnaire délégué

du portefeuille de crédit ................................... 33

I 2 - le marché bancaire : marché contestable

et efficient ...................................................... 35

II - la gestion du portefeuille de crédits dans un

marché efficient ......................................... 36

II 1 - la réglementation bancaire en zone BEAC : un

outil en faveur de la division du risque sur le marché bancaire

camerounais

.......................................................................................

37

II 2 - la diversification du portefeuille de crédits pour

une réponse satisfaisante aux besoins de l'économie

...............................................................................................................................

38

Conclusion première partie

............................................................................

40

Deuxième partie : la

diversification du portefeuille de crédits : une composante

insuffisante de la rentabilité bancaire au Cameroun

.................................................................... 41

Introduction deuxième partie

.............................................................................................

42

Chapitre 3 : les effets de la

diversification du portefeuille de crédits sur la rentabilité

bancaire au

Cameroun .........................................................................................................................

43

Section 1 : la démarche

économétrique et l'aspect analytique

.................................... 43

I - Présentation du modèle d'analyse retenu

...........................................................................

44

I 1 - le modèle de régression multiple

....................................................................................

44

I 2 - les outils statistiques d'analyse

.......................................................................................

45

II - cadre d'analyse du modèle

...............................................................................................

46

II 1 - la définition des variables

..............................................................................................

46

II 2 - présentation des données et exposé du

modèle .............................................................

48

Section 2 : Appréciation des facteurs explicatifs de

la rentabilité bancaire au Cameroun ..... 50

I - prolongement de la période et test de normalité

des variables du modèle ........................ 51

I 1 - présentation de l'indice de Hirschman-Herfindal

........................................................... 51

I 2 - trimestrialisation des données annuelles et test de

normalité ......................................... 52

II - stationnarité des variables et estimation du

modèle de la rentabilité bancaire ................. 53

II 1 - les résultats des tests de stationnarité

............................................................................

54

II 2 - l'analyse des résultats et de

l'intérêt de la prise en compte des frais généraux

dans le modèle

.....................................................................................................................................

55

Chapitre 4 : la sensibilité des

résultats bancaires à la taille des banques

............................. 59

Section 1 : l'impact de la taille des banques sur les

vertus de la diversification du portefeuille de crédits au Cameroun

.................................................................................

59

I - présentation des résultats et

appréciation des différents coefficients

................................ 59

I 1 - les résultats de l'estimation de l'équation

de la rentabilité bancaire .............................. 59

I 2 - Appréciation des signes des coefficients

........................................................................ 61

II - la capacité des différentes variables

à expliquer la rentabilité bancaire au Cameroun en absence de la

variable taille des banques

................................................................................

62

II 1 - l'effet des variables managériales

.................................................................................

62

II 2 - l'impact des facteurs macroéconomiques et

macro-financiers sur la rentabilité

bancaire....................................................................................................................................

63

Section 2 : les enseignements du modèle de la

rentabilité bancaire au Cameroun ................. 64

I - les vertus de la bonne tenue des éléments de

la marge d'intermédiation et la rentabilité bancaire au Cameroun

.............................................................................................................

65

I 1 - L'attitude de la rentabilité bancaire face à

la diversification du portefeuille de crédits...65

I 2 - la contribution des charges d'exploitation bancaire

....................................................... 67

II - le rationnement du crédit et l'efficience du

marché bancaire camerounais ..................... 67

II 1 - l'efficience allocationnelle ou fonctionnelle

................................................................. 68

II 2 - diversification du portefeuille de crédits et

réduction du risque.................................... 69

Conclusion deuxième partie

....................................................................................................

70

Conclusion générale

.....................................................................................

71

Bibliographie

................................................................................................

75

|