From the figures above, it appears that the unit cost

is 474 F for the week under consideration using the absorption costing

technique. This figure represents one of the mean that will be compared during

the process of testing our hypotheses.

Since we are dealing with job costing, the best method of

determining that unit cost is through the use of a Job cost Sheet like the

following:

|

JOB COST SHEET: Absorption

costing

|

|

|

Job number: 1

|

|

Start date: 01st august 2002

|

|

|

|

|

|

Department: printing

|

|

Delivery date: 05th august 2002

|

|

|

|

|

|

Item: Five-day production of CT

|

|

Units completed: 50 000

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Direct Materials

|

|

|

|

|

|

|

|

Requisition N°

|

Amount

|

type of labour

|

ticket

|

Hours

|

Amount

|

|

|

|

|

|

paper 100

|

6 158 250 F

|

direct labour for pre-printing

|

1

|

39,5

|

237 000 F

|

|

|

|

|

|

black ink 101

|

700 000 F

|

direct labour for copy

|

2

|

9,8

|

24 500 F

|

|

|

|

|

|

blue ink 102

|

100 000 F

|

direct labour for soaking

|

3

|

14

|

84 000 F

|

|

|

|

|

|

red ink 103

|

|

150 000 F

|

direct labour for printing works

|

4

|

14

|

630 000 F

|

|

|

|

|

|

yellow ink 104

|

100 000 F

|

direct labour for edition

|

5

|

35

|

510 000 F

|

|

|

|

|

|

photographic sheet 104

|

2 500 000 F

|

Total C/F

|

|

|

1 485 500 F

|

|

|

|

|

|

photographic film 105

|

300 000 F

|

|

|

|

|

|

|

|

|

|

Sheet Developer 106

|

396 000 F

|

EXPENSES

|

|

|

Manufacturing Overheads

|

|

|

Film developer 107

|

45 000 F

|

Description

|

Amount

|

|

Type

|

Hours

|

Rate

|

Amount

|

|

|

Film fixing liquid 108

|

45 000 F

|

fixed admin. Exp.

|

2 500 000 F

|

|

water

|

80

|

845 F

|

67 600 F

|

|

|

sheet proofreader 109

|

10 800 F

|

variable admin. Exp.

|

1 350 000 F

|

|

electricity

|

80

|

2 625 F

|

210 000 F

|

|

|

eraser 110

|

|

16 000 F

|

variable selling exp.

|

950 000 F

|

|

depreciation

|

80

|

55 962 F

|

4 476 921 F

|

|

|

soaking solution 111

|

120 000 F

|

fixed selling exp.

|

500 000 F

|

|

spare parts

|

80

|

5 162 F

|

418 000 F

|

|

|

sheet cleaner 112

|

62 400 F

|

Total C/F

|

5 300 000 F

|

|

Total C/F

|

|

|

5 172 521 F

|

|

|

tracing paper 113

|

50 000 F

|

|

|

|

|

|

|

|

|

|

|

photocopy paper A4 114

|

90 000 F

|

|

|

|

|

|

|

|

|

|

|

photocopy paper A3 115

|

17 500 F

|

Job cost Summary

|

|

|

|

|

|

|

transparent sellotape 116

|

1 400 F

|

Direct materials

|

11 761 950 F

|

|

|

|

|

|

|

|

packaging sellotape 117

|

5 600 F

|

Direct Labour

|

1 485 500 F

|

|

|

|

|

|

|

|

packaging string 118

|

13 500 F

|

Manufacturing Overheads

|

5 172 521 F

|

|

|

|

|

|

|

|

white glue 119

|

3 500 F

|

Selling and Admin. Exp.

|

5 300 000 F

|

|

|

|

|

|

|

|

industrial rag 120

|

70 000 F

|

Total Cost

|

23 719 971 F

|

|

|

|

|

|

|

|

soap paste 121

|

3 000 F

|

Unit product cost

|

474 F

|

|

|

|

|

|

|

|

toner cartridge HP1200 122

|

720 000 F

|

|

|

|

|

|

|

|

|

|

|

toner cartridge HP5000 123

|

54 000 F

|

|

|

|

|

|

|

|

|

|

|

toner cartridge HP8500-black124

|

6 000 F

|

|

|

|

|

|

|

|

|

|

|

toner cartridge HP8500-blue 125

|

6 000 F

|

|

|

|

|

|

|

|

|

|

|

toner cartridge HP8500-Red 126

|

6 000 F

|

|

|

|

|

|

|

|

|

|

|

toner cartridgeHP8500-yellow 127

|

6 000 F

|

|

|

|

|

|

|

|

|

|

|

drummer KitC4153A 128

|

6 000 F

|

|

|

|

|

|

|

|

|

|

|

Total C/F

|

|

11 761 950 F

|

|

|

|

|

|

|

|

|

|

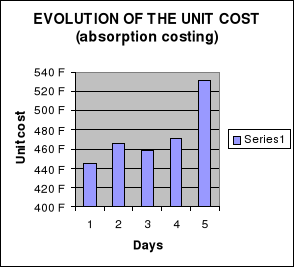

Graphically, the data on the daily unit costs could be presented

as such:

Figure 1-2 Evolution of the unit cost (absorption

costing)

Source: the author

We also need the standard deviation of the daily unit cost and

this can be obtained from the formula:

SD=(?Xi-A1)/N1

Xi: daily unit cost

A1: Mean unit cost

N1: number of production days

Again, using the spreadsheet,

|