The use of job costing as a tool for the pricing and cost control decisions in the printing industry: the case of Société de Presse et d'Editions (SOPECAM)( Télécharger le fichier original )par Christian Kuiate Sobngwi University of Buea - Bachelor of Science 2003 |

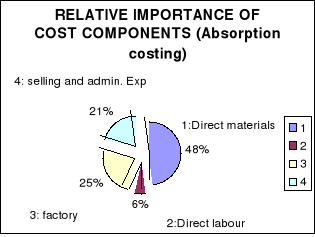

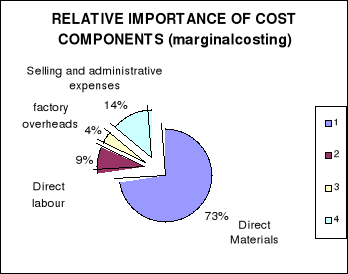

CHAPTER FIVE:SUMMARY OF FINDINGS, CONCLUSION AND RECOMMENDATIONSI. SUMMARY OF FINDINGSAs we are heading towards the end of the study entitled «The use of Job costing as a tool for the pricing process», it seems necessary to recall its objectives. This study was conducted for the sake of coming out with a reliable unit cost figure for the newspaper «Cameroon Tribune»; it was also designed to help in the determination of a good allocation basis for the company overhead costs and finally, while engaging in this research work, we wanted to improve the pricing and cost control processes at SOPECAM. The research, as mentioned above was conducted at SOPECAM, a State-owned enterprise, responsible of the publishing of the newspaper Cameroon Tribune. Data have been collected from primary and secondary sources constituted by the results of interviews conducted at the company premises with its executives and data gathered from the financial and accounting statements of the company. These data were analysed using job costing associated to the absorption and marginal costing techniques. The results of this analysis were interpreted using the Student's -T- test. It was found that under absorption costing, the unit cost of the newspaper is FCFA 474, while under marginal costing, it was estimated at FCFA 325. After having tested the hypotheses of the study, we came to the conclusion that the two costing techniques used namely marginal and absorption costing, cannot be used for the same purposes. In Marginal costing, the company is only concerned with the costs directly related to the product, the fixed production and non-manufacturing costs are not taken into account, it is therefore preferable to use this technique when trying to control the costs associated with a particular product. It must as such be used for the cost control programmes instead of the pricing decisions. Concerning Absorption costing, with this technique, all the costs incurred when manufacturing a product are taken into account, this costing technique enables the company to ascertain with accuracy what it cost the entire organisation to make a particular product. It relates to the overall profitability of the company and for this reason, we must use this technique for the pricing decision. II. CONLUSIONSAfter having reviewed the results of the study, we must normally derive a conclusion from the information obtained. This conclusion will stem from some remarks we have made throughout the study. The first point to mention at this level is that the newspaper under study is currently being sold at FCFA 300, which means from our findings, that the company is under-pricing its product. The second point to mention is that, although the production of the newspaper is divided into three stages as explained in the previous chapter, the method of allocating the manufacturing costs of the product using hourly rates as done by the company seems not to be very adequate for this product. The third point of interest concerns the overhead allocation bases. In the company, labour hours are used to assign and allocate overhead costs to the various products, but from the observation of the researcher, it seems as if the labour hours rarely change and can be treated as fixed costs; This is mainly due to the fact that the company workers are all salaried worker and none of them is employed on an hourly basis, thus the labour hours are not a good yardstick as far as the spreading of overhead costs over production units is concerned. Another element of consideration in the analysis concerns the cost structure of the company. When we decided to determine the unit cost of this product it was not just for the sake of having a unit cost figure, but it was also to examine the various components of that unit cost and their relative importance as this may help us in determining the real cost centres of the enterprise. From the analysis performed in the previous chapter, the following results have been obtained: Figure 5-1 Relative importance of the cost components in SOPECAM's cost Structure (absorption costing).

Source: the author Figure 5-2 Relative importance of the cost components in SOPECAM's cost structure (marginal costing).

Source: the author Having outlined our points of interest, we can now draw some conclusions as far as our study is concerned. One of the initial goal of this study was the determination a reliable unit cost figure for the newspaper Cameroon tribune, it has appeared using absorption costing that the unit cost could be estimated at FCFA 474 which as mentioned above is greater than the selling price of the product. As such, it appears that the company is not following a profit-maximisation goal when producing Cameroon Tribune, its main focus appears to be the provision of daily, reliable and accurate information to the Cameroonian population; and for this to be done, instead of maximising their profit, or taking advantage of their position of leader of the market because they are the only daily newspaper in Cameroon with the exception of the newspaper «Mutations», they prefer to achieve a Goodwill preservation objective by making sure that they remain at the level of the mean-income earner in Cameroon. This goal of goodwill and image preservation is identified by Harper (1989)25(*) as strategy Pricing; the firm goal here is not so much profit maximisation but the achievement of the long-term goal of the firm from the marketing point of view, that is the satisfaction of the customer. This situation may lead us to question ourselves about the survival of the company, but since Cameroon Tribune is not the only product manufactured at SOPECAM, and since SOPECAM is benefiting from the Sate endowments and subsidies, we can say that the company is not supposed to face a situation of jeopardy because of the production of Cameroon tribune. Another objective of the study was the determination of the right allocation basis for the overhead costs of the company. As previously mentioned, the company currently uses the labour hours as allocation rates for the company costs, and also it is important to mention the absence of a managerial accounting department in the company which should have taken care of such a problem; from our study, we realised that most of the processes depend a lot on the effective functioning of specific machines and most of the labour costs incurred by the company are quite fixed since all the employees of the company are salaried workers and not wage earners. As such, it seems advisable to make use of the machine-hours instead of the labour-hours as the basis for the allocation of the overhead costs in the company. Concerning the cost structure of SOPECAM, it appears from the results of our study that the company should continuously monitor the materials costs as they appear to be the most important component of the unit cost, they represent 48%and 73% of the total cost when using absorption and marginal costing respectively. The company management should also take into consideration the relatively small share of the labour cost (6% and 9%) in the cost structure. This quite small share may be a good indicator of the declining importance of that cost in the company, which may lead the management to make decisions about the overhead allocation bases. These appreciations the current functioning of SOPECAM directly introduce into the next heading, which is about the recommendations that we could make in order to improve the processes at SOPECAM. * 25 Harper, W.M. (1989): Management Accounting (3rd edition), Pitman Publishing, London |

|