4.6. Test for

stationary

The footstep of this analysis is to determine whether the

series are stationary or not. The ADF was used to test for stationary of these

series as it provides a superior test to DF, especially in case the residuals

of the regression could be serially correlated. The lag length has been

automatically selected by AIC from eleven proposed lags and all three

possibilities have been tested: neither intercept nor trend, intercept but no

trend and both intercept and trend.

TABLE 4.1: Money Stock

stationary (MT)

|

ADF Test Statistic

|

5.023678

|

1% Critical Value*

|

-2.7411

|

|

|

5% Critical Value

|

-1.9658

|

|

|

10% Critical Value

|

-1.6277

|

|

*MacKinnon critical values for rejection of hypothesis of a unit

root.

|

|

|

|

|

|

|

|

|

|

|

|

Augmented Dickey-Fuller Test Equation

|

|

Dependent Variable: D(MT)

|

|

Method: Least Squares

|

|

Date: 07/20/11 Time: 09:07

|

|

Sample(adjusted): 1996 2010

|

|

Included observations: 15 after adjusting endpoints

|

|

Variable

|

Coefficient

|

Std. Error

|

t-Statistic

|

Prob.

|

|

MT(-1)

|

0.159544

|

0.031758

|

5.023678

|

0.0002

|

|

R-squared

|

0.322881

|

Mean dependent var

|

30.25333

|

|

Adjusted R-squared

|

0.322881

|

S.D. dependent var

|

33.05061

|

|

S.E. of regression

|

27.19644

|

Akaike info criterion

|

9.508390

|

|

Sum squared resid

|

10355.05

|

Schwarz criterion

|

9.555593

|

|

Log likelihood

|

-70.31292

|

Durbin-Watson stat

|

1.871053

|

As /ADF/ is greater than /5%/

critical value, MT is stationary at lag 0, level and function

of none.

TABLE 4.2: Inflation Gap

stationary (IG)

|

ADF Test Statistic

|

-4.663015

|

1% Critical Value*

|

-4.0113

|

|

|

5% Critical Value

|

-3.1003

|

|

|

10% Critical Value

|

-2.6927

|

|

*MacKinnon critical values for rejection of hypothesis of a unit

root.

|

|

|

|

|

|

|

|

|

|

|

|

Augmented Dickey-Fuller Test Equation

|

|

Dependent Variable: D(IG)

|

|

Method: Least Squares

|

|

Date: 09/19/11 Time: 11:40

|

|

Sample(adjusted): 1997 2010

|

|

Included observations: 14 after adjusting endpoints

|

|

Variable

|

Coefficient

|

Std. Error

|

t-Statistic

|

Prob.

|

|

IG(-1)

|

-2.059676

|

0.441705

|

-4.663015

|

0.0007

|

|

D(IG(-1))

|

0.347099

|

0.247617

|

1.401760

|

0.1886

|

|

C

|

-1.341209

|

1.262206

|

-1.062591

|

0.3107

|

|

R-squared

|

0.796606

|

Mean dependent var

|

-0.105357

|

|

Adjusted R-squared

|

0.759626

|

S.D. dependent var

|

9.320982

|

|

S.E. of regression

|

4.569890

|

Akaike info criterion

|

6.064265

|

|

Sum squared resid

|

229.7229

|

Schwarz criterion

|

6.201206

|

|

Log likelihood

|

-39.44985

|

F-statistic

|

21.54115

|

|

Durbin-Watson stat

|

1.603652

|

Prob(F-statistic)

|

0.000157

|

As /ADF/ is greater than all

critical values especially /5%/, IG is stationary at lag 1,

level and function with intercept.

Table 4.3: Output Gap

stationary

|

ADF Test Statistic

|

-4.887496

|

1% Critical Value*

|

-4.1366

|

|

|

5% Critical Value

|

-3.1483

|

|

|

10% Critical Value

|

-2.7180

|

|

*MacKinnon critical values for rejection of hypothesis of a unit

root.

|

|

|

|

|

|

|

|

|

|

|

|

Augmented Dickey-Fuller Test Equation

|

|

Dependent Variable: D(YG,3)

|

|

Method: Least Squares

|

|

Date: 09/19/11 Time: 12:11

|

|

Sample(adjusted): 1999 2010

|

|

Included observations: 12 after adjusting endpoints

|

|

Variable

|

Coefficient

|

Std. Error

|

t-Statistic

|

Prob.

|

|

D(YG(-1),2)

|

-2.449332

|

0.501143

|

-4.887496

|

0.0009

|

|

D(YG(-1),3)

|

0.595279

|

0.284900

|

2.089433

|

0.0662

|

|

C

|

-1.073325

|

9.702328

|

-0.110626

|

0.9143

|

|

R-squared

|

0.832995

|

Mean dependent var

|

-4.231833

|

|

Adjusted R-squared

|

0.795882

|

S.D. dependent var

|

74.27310

|

|

S.E. of regression

|

33.55613

|

Akaike info criterion

|

10.07663

|

|

Sum squared resid

|

10134.12

|

Schwarz criterion

|

10.19786

|

|

Log likelihood

|

-57.45980

|

F-statistic

|

22.44524

|

|

Durbin-Watson stat

|

1.843834

|

Prob(F-statistic)

|

0.000318

|

As /ADF/ is

greater than all critical values especially /5%/, YG is

stationary at lag 1, second difference and function with intercept.

TABLE 4.4: Variation of

Exchange stationary

|

ADF Test Statistic

|

-4.393650

|

1% Critical Value

|

-4.1366

|

|

|

5% Critical Value

|

-3.1483

|

|

|

10% Critical Value

|

-2.7180

|

|

*MacKinnon critical values for rejection of hypothesis of a unit

root.

|

|

|

|

|

|

|

|

|

|

|

|

Augmented Dickey-Fuller Test Equation

|

|

Dependent Variable: D(DEXCH,3)

|

|

Method: Least Squares

|

|

Date: 09/19/11 Time: 12:16

|

|

Sample(adjusted): 1999 2010

|

|

Included observations: 12 after adjusting endpoints

|

|

Variable

|

Coefficient

|

Std. Error

|

t-Statistic

|

Prob.

|

|

D(DEXCH(-1),2)

|

-1.616566

|

0.367932

|

-4.393650

|

0.0013

|

|

C

|

17.89631

|

23.68642

|

0.755552

|

0.4673

|

|

R-squared

|

0.658752

|

Mean dependent var

|

14.17417

|

|

Adjusted R-squared

|

0.624627

|

S.D. dependent var

|

133.8383

|

|

S.E. of regression

|

81.99966

|

Akaike info criterion

|

11.80232

|

|

Sum squared resid

|

67239.43

|

Schwarz criterion

|

11.88314

|

|

Log likelihood

|

-68.81391

|

F-statistic

|

19.30416

|

|

Durbin-Watson stat

|

1.534741

|

Prob(F-statistic)

|

0.001348

|

As /ADF/ is

greater than all critical values especially /5%/, DEXCH is

stationary at lag 0, second difference and function with intercept.

TABLE 4.5: Previous Money

Stock stationary

|

ADF Test Statistic

|

-3.699480

|

1% Critical Value*

|

-4.1366

|

|

|

5% Critical Value

|

-3.1483

|

|

|

10% Critical Value

|

-2.7180

|

|

*MacKinnon critical values for rejection of hypothesis of a unit

root.

|

|

|

|

|

|

|

|

|

|

|

|

Augmented Dickey-Fuller Test Equation

|

|

Dependent Variable: D(M1,3)

|

|

Method: Least Squares

|

|

Date: 09/19/11 Time: 12:20

|

|

Sample(adjusted): 1999 2010

|

|

Included observations: 12 after adjusting endpoints

|

|

Variable

|

Coefficient

|

Std. Error

|

t-Statistic

|

Prob.

|

|

D(M1(-1),2)

|

-1.159214

|

0.313345

|

-3.699480

|

0.0041

|

|

C

|

0.034242

|

8.436719

|

0.004059

|

0.9968

|

|

R-squared

|

0.577812

|

Mean dependent var

|

0.391667

|

|

Adjusted R-squared

|

0.535594

|

S.D. dependent var

|

42.88315

|

|

S.E. of regression

|

29.22374

|

Akaike info criterion

|

9.738851

|

|

Sum squared resid

|

8540.268

|

Schwarz criterion

|

9.819669

|

|

Log likelihood

|

-56.43311

|

F-statistic

|

13.68615

|

|

Durbin-Watson stat

|

2.076159

|

Prob(F-statistic)

|

0.004112

|

As / ADF/ is greater than / 5%/

critical value, M1 is stationary at lag 0, second difference

and function with intercept.

TABLE 4.6: Previous Inflation

Gap stationary

|

ADF Test Statistic

|

-4.663015

|

1% Critical Value*

|

-4.0113

|

|

|

5% Critical Value

|

-3.1003

|

|

|

10% Critical Value

|

-2.6927

|

|

*MacKinnon critical values for rejection of hypothesis of a unit

root.

|

|

|

|

|

|

|

|

|

|

|

|

Augmented Dickey-Fuller Test Equation

|

|

Dependent Variable: D(IG)

|

|

Method: Least Squares

|

|

Date: 09/19/11 Time: 11:40

|

|

Sample(adjusted): 1997 2010

|

|

Included observations: 14 after adjusting endpoints

|

|

Variable

|

Coefficient

|

Std. Error

|

t-Statistic

|

Prob.

|

|

IG(-1)

|

-2.059676

|

0.441705

|

-4.663015

|

0.0007

|

|

D(IG(-1))

|

0.347099

|

0.247617

|

1.401760

|

0.1886

|

|

C

|

-1.341209

|

1.262206

|

-1.062591

|

0.3107

|

|

R-squared

|

0.796606

|

Mean dependent var

|

0.105357

|

|

Adjusted R-squared

|

0.759626

|

S.D. dependent var

|

9.320982

|

|

S.E. of regression

|

4.569890

|

Akaike info criterion

|

6.064265

|

|

Sum squared resid

|

229.7229

|

Schwarz criterion

|

6.201206

|

|

Log likelihood

|

-39.44985

|

F-statistic

|

21.54115

|

|

Durbin-Watson stat

|

1.603652

|

Prob(F-statistic)

|

0.000157

|

As /ADF/ is

greater than all critical values especially /5%/, IG1 is

stationary at lag 1, level and function with intercept.

Table 4.7: previous Output

Gap stationary

|

ADF Test Statistic

|

-5.810852

|

1% Critical Value*

|

-4.1366

|

|

|

5% Critical Value

|

-3.1483

|

|

|

10% Critical Value

|

-2.7180

|

|

*MacKinnon critical values for rejection of hypothesis of a unit

root.

|

|

|

|

|

|

|

|

|

|

|

|

Augmented Dickey-Fuller Test Equation

|

|

Dependent Variable: D(YG1,3)

|

|

Method: Least Squares

|

|

Date: 09/19/11 Time: 12:27

|

|

Sample(adjusted): 1999 2010

|

|

Included observations: 12 after adjusting endpoints

|

|

Variable

|

Coefficient

|

Std. Error

|

t-Statistic

|

Prob.

|

|

D(YG1(-1),2)

|

-1.539314

|

0.264903

|

-5.810852

|

0.0002

|

|

C

|

1.842228

|

10.71345

|

0.171955

|

0.8669

|

|

R-squared

|

0.771512

|

Mean dependent var

|

0.864250

|

|

Adjusted R-squared

|

0.748663

|

S.D. dependent var

|

74.01819

|

|

S.E. of regression

|

37.10790

|

Akaike info criterion

|

10.21655

|

|

Sum squared resid

|

13769.96

|

Schwarz criterion

|

10.29737

|

|

Log likelihood

|

-59.29929

|

F-statistic

|

33.76600

|

|

Durbin-Watson stat

|

2.583075

|

Prob(F-statistic)

|

0.000170

|

As /ADF/ is greater than all

critical values especially /5%/, YG1 is stationary at lag 0,

second difference and function with intercept.

Table 4.8: Previous Variation

of Exchange stationary

|

ADF Test Statistic

|

-5.187147

|

1% Critical Value*

|

-4.1366

|

|

|

5% Critical Value

|

-3.1483

|

|

|

10% Critical Value

|

-2.7180

|

|

*MacKinnon critical values for rejection of hypothesis of a unit

root.

|

|

|

|

|

|

|

|

|

|

|

|

Augmented Dickey-Fuller Test Equation

|

|

Dependent Variable: D(DEXCH1,2)

|

|

Method: Least Squares

|

|

Date: 09/19/11 Time: 12:36

|

|

Sample(adjusted): 1999 2010

|

|

Included observations: 12 after adjusting endpoints

|

|

Variable

|

Coefficient

|

Std. Error

|

t-Statistic

|

Prob.

|

|

D(DEXCH1(-1))

|

-1.469962

|

0.283386

|

-5.187147

|

0.0004

|

|

C

|

1.485446

|

10.59132

|

0.140251

|

0.8912

|

|

R-squared

|

0.729045

|

Mean dependent var

|

2.302500

|

|

Adjusted R-squared

|

0.701949

|

S.D. dependent var

|

67.19665

|

|

S.E. of regression

|

36.68534

|

Akaike info criterion

|

10.19364

|

|

Sum squared resid

|

13458.14

|

Schwarz criterion

|

10.27446

|

|

Log likelihood

|

-59.16186

|

F-statistic

|

26.90649

|

|

Durbin-Watson stat

|

2.085680

|

Prob(F-statistic)

|

0.000409

|

As /ADF/ is greater than all

critical value /5%/, DEXCH1 is stationary at lag 0, first

difference and function with intercept.

Table 4.9: Error Term

stationary

|

ADF Test Statistic

|

-4.335477

|

1% Critical Value*

|

-4.1366

|

|

|

5% Critical Value

|

-3.1483

|

|

|

10% Critical Value

|

-2.7180

|

|

*MacKinnon critical values for rejection of hypothesis of a unit

root.

|

|

|

|

|

|

|

|

|

|

|

|

Augmented Dickey-Fuller Test Equation

|

|

Dependent Variable: D(E)

|

|

Method: Least Squares

|

|

Date: 07/20/11 Time: 09:46

|

|

Sample(adjusted): 1999 2010

|

|

Included observations: 12 after adjusting endpoints

|

|

Variable

|

Coefficient

|

Std. Error

|

t-Statistic

|

Prob.

|

|

E(-1)

|

-1.299467

|

0.299729

|

-4.335477

|

0.0015

|

|

C

|

16.62786

|

9.471546

|

1.755559

|

0.1097

|

|

R-squared

|

0.652734

|

Mean dependent var

|

1.986182

|

|

Adjusted R-squared

|

0.618007

|

S.D. dependent var

|

49.59723

|

|

S.E. of regression

|

30.65385

|

Akaike info criterion

|

9.834405

|

|

Sum squared resid

|

9396.583

|

Schwarz criterion

|

9.915223

|

|

Log likelihood

|

-57.00643

|

F-statistic

|

18.79636

|

|

Durbin-Watson stat

|

1.976710

|

Prob(F-statistic)

|

0.001477

|

As /ADF/ is

greater than /5%/ critical value, error term is stationary at 0 lag, level and

function with intercept.

Notes: all tests of stationary are done in Eviews 3.1

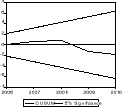

CUSUM TEST

Source of basic data: BNR, NISR and MINECOFIN

As the line of cusum does not get out of the corridor, means that

the parameters of the regression model are stable.

M = 48.62344 + 0.996100M1 + 1.492988IG + 2.824734IG1 - 0.549954YG

+ 0.099609YG1 -

P (0.001) (0.003) (0.002)

(0.000) (0.02) (0.007)

0.088485EX - 0.311933EX1.

(0.0045) (0.01)

F table = 4.7 Fcritical =

38.02

R2 = 0.98 dw = 2.46

As dw is greater than R2, the estimated model is

correctly specified.

DW and BREUCH-GODFREY TEST show that there is no autocorrelation

because the

DW is the zone of none autocorrelation zone and nR2

> ÷2 for LM (Lagrangian Multiplier or

Breuch-Godfrey Test)

nR2=31.36 > X2 =9.88623

R2 is coming from estimation of errors.

All coefficients have an econometric sense explained by

Fcritical that is greater than Ftable , means that the

concerned variables have an effect on current money stock aggregate.

After testing stationary for all variables and model

specification, now interpretation.

|