Determinants of private sector financing in sub saharan Africa: case study of Burkina Faso project( Télécharger le fichier original )par Brahima BANDAOGO Université de Namur - Advanced Master in International and Development Economics 2018 |

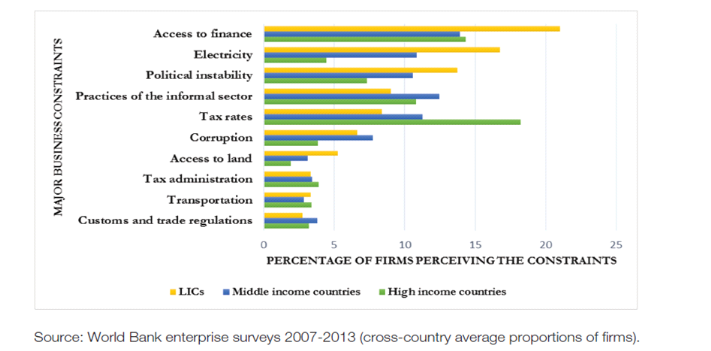

AbstractThe aim of this thesis was to identify the determinants of firm access to finance in Burkina Faso. For this purpose, we employ an ordered logit model to analyze data coming from the World Bank enterprise survey collected in 2009 on the activities of non-agricultural formal firms in the country. By using an objective measure of access to finance proposed by Kuntchev et al. (2013), our findings suggest that firm's access to finance is determined by factors like firm's size, firm's legal status, firm's export status and firm's performance measured by labor productivity. Indeed, firm's size and performance have positive effect on the likelihood of having access to finance. Also, being a firm, which exports its production compared to firms that produce only for the national market increases the likelihood of having access to finance. Sole proprietor firms meet also difficulties in having access finance compared to firms belonging to several owners. Besides, robustness analysis that uses a subjective measure of firm's access to finance (based on their perception) confirms partially our findings in a sense that the positive and significant effect of firm's size and legal status on the likelihood of having access to finance are robust. However, firm's performance and export statusbecome not significant in explaining firm's access to finance while foreign ownership of the firm becomes significant with a positive effect on firm's likelihood of having access to finance. Finally, we recommend that SMEs should join Business Associations and seek credit schemes. This association should promote credit information among potential borrowers as a way of reducing information asymmetry in the credit market. Second, sole proprietor firms need to look for partnership in order to change their legal status and create for instance, partnership companies or shareholding companies, so that they could have a better access to financing. Third, low performing firms need to increase their performance if they want to be less credit constraint. Fourth, non-exporting firms need to learn from exporting firms so that they will know how to position themselves for institutional borrowing. IntroductionPrivate sectoris believedto play an important role ineconomic development of Africa. For instance, Stampini et al., (2011) analyzing data from African Economic Outlook on fifty1(*) African countries, pointed that private sector accounted for over 80?% of production, two-thirds of investment, three-fourths of credit to the economy and fourth-five of consumptionover the period 1996-2008. In the same way, the African Development Report2(*)in 2011 indicates that the private sector (informal sector included)contributes to about 90?% of jobs for the employed working age population in Africa. In Burkina Faso, the important role played byprivate sector in its economy is also well established. Indeed, private sector investment in Burkina Faso increased from 43% of total investment during the period 1996-2002 to 61% over the period 2003-2008 (Stampini et al, 2011).Besides, this sector is dominated by the micro, small and medium-sized enterprises (MSMEs). According to the World Bank (2015), MSMEs represented approximately 84.3% of total firms in 2009. Despite the important role played by the private sector in SSA economies, this sector has been facing many constraints. Indeed, during the period 2007-2013, the five main constraints to the growth of private sector in Low Income Countries (LICs) are difficulties to access to external finance, electricity supply shortage, political instability, practices of informal sector, high tax rates and corruption. In particular, access to finance was particularly problematic for the private sector in these economies as we can observe in figure 1. Figure 1: Access to finance as a major Constraint to the growth of firms in Low Income Countries

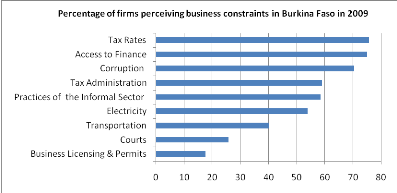

Note: This graph is from Dayé et al. (2016), page 12. In Burkina Faso, tax rates, access to finance and corruption are the first three major business constraints to growth of firms in 2009 (see figure 2). Indeed, according to the World Bank data, 75.7%, 75% and 70.5% of the firms in Burkina Faso in 2009, perceived respectively tax rates, access to finance and corruption as a constraint to their growth in 2009 (see figure 2). Figure 2: Major business constraints in Burkina Faso in 2009

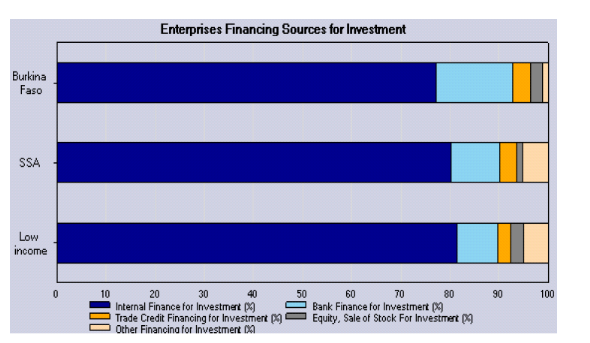

Source: Author based on World Bank data (Africa Development Indicators) This high proportion of firms perceiving «access to finance» as their second major constraint in Burkina Fasorepresent one of the highest proportionamong West African Economic and Monetary Union (WAEMU) countries. For instance, the proportion of firms that perceived «access to finance» as a major constraint in 2009 was 66.6%, 48.1% and 58.6% respectively for Cote d'Ivoire, Mali3(*) and Togo (World Bank, enterprise survey 2009 and 2010). In the same period, the average for SSA was 44.9%.In addition, according to the World Bank enterprise survey firms in Burkina Faso face serious credit rationing. Indeed,out of 85% of firms having expressed needs for financing only 28%reported having a loan or credit line. To satisfy their financial needs firms may have the choice between two sources of financing which are internal financing and external financing. Among those sources of financing, external financing is less accessible for MSMEs than internal financing in developing countries and particularly in Burkina Faso. Figure 3 shows that the main source of financing for enterprises in LICs or SSA as well as in Burkina Faso is internal financing. It represented in 2009respectively for non-agricultural formal firms from Burkina Faso, SSA, and LICs more than 75%, 80% and 81% of their financing needs (World Bank, 2009). Not only, the excessive use of internal financing by firms showsa sign of potentially inefficient financial intermediation, but also a sign that firms are externally credit-constraint in Burkina Faso. Indeed, the percentage of non-agricultural formal firms with bank loans or line of credit in 2009 was only 28.4% compared to 21.6% for SSA (World Bank, 2009). Figure 3: Enterprises financingsources

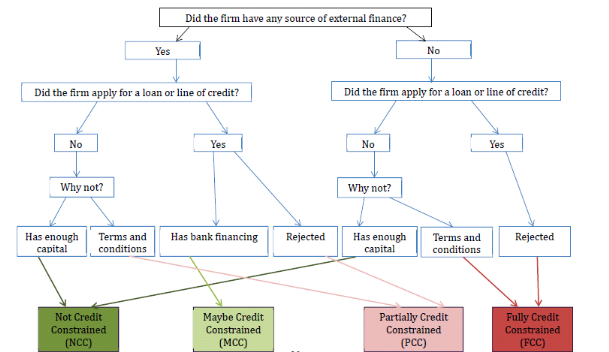

Source: World Bank (2009), Burkina Faso Country profile, enterprise Survey. Page 11 Moreover, the share of working capital financed by external financing for non-agricultural formalfirms in 2009 represented 25.8% whereas it was 26.5% and 25.1% respectively for SSA and LICs (World Bank, 2009). The lower share of external financing in 2009, could be explained in part by the high value of collateral needed (as a share of the loan amount) which represented 175.5% and washigher than the average for SSA which was 142.6% (World Bank, 2009). The existence of financing gap for the private sector in Africa for MSMEs has been shown by Sowa et al. (1992) for Ghana and Daniels and Ngwira, (1993) for Malawi. For instance, forDaniels and Ngwira (1993), reports that access to credit since start-up operation is low in the MSME sector and more than 80% ofall MSMEs have never received any loans in Malawi. Moreover, only1.2% of MSMEs have received loans from a formal credit institution.Aryeetey et al. (1994) observed that 38% of SMEs surveyed mention credit as a constraint while Hansen et al. (2012) found that about 39.9%, 18.3% and 8.5% of small firms in Ghana, Kenya and South Africa cited access to finance as a barrier for their growth. For Bani, (2003) most of SMEs loan applicants in Africa are not granted. Bigsten et al. (2000) reported that 90% of small firms are denied credit from the formal financial sector due to their inability to fulfill conditions such as collateral security. Working on six African countries, Bigsten et al. (2003) among those firms which applied for a loan, small firms are unlikely to have a loan from banks. More recently, Berg and Fuchs (2013) reported that the share of SME lending in the overall portfolios of banks in five Sub-Saharan African countries (Kenya, Nigeria, Rwanda, South Africa and Tanzania)is between 5% and 20%. As outlined above, not only private sectorhas been playing an important role in SSA economies in general and particularly in Burkina Faso but also faces mainlythe constraint of access to finance that impairs its contribution to the economy. These stylized facts motivate to studythe determinants of private sector access to finance in Burkina Faso. Specifically, the thesis aims to address the following research questions: · do firms' characteristics like age, size, performance, legal status and ownership status affect their likelihood of having access to external financing? · do the characteristics of the top manager (education, gender and experience) affect firms' likelihood of havingaccess to external financing? The contribution of the current thesis is to help fill the gap of the lack of papers dealing with private sector's access to finance in Burkina on one hand, and to use an innovative approach of measuring firm's «access» to finance developed by Kuntchev et al. (2013)on the other hand.Moreover, not only it is important to study the determinants of private sector access to finance for the sake of a better understanding of this issue, but also for its policies implications related to the alleviation of this constraint in order to improve the contribution of private sector to economic growth in the country. To examine the determinants of private sector«access to finance», we estimatean ordered logit regression model using the World Bank enterprise survey data on private non-agricultural formal firms. In particular, our dependent variable takes up to four modalities according to the measure proposed by Kuntchev et al. (2013). Our findings suggest that firm's access to finance is determined by factors like firm's size, firm's legal status, firm's export status and firm's performance measured by labor productivity. Indeed, firm's size and performance have positive effect on the likelihood of having access to finance. Also, being a firm which exports its production compared to firms that produce only for the local market increases the likelihood of having access to finance. Sole proprietors meet also difficulties in accessing finance compared to firms belonging to several owners. Besides, robustness analysis that uses a subjective measure of firm's access to finance (based on their perception) supports partially our findings in a sense that the positive and significant effect of firm's size and legal status on the likelihood of having access to finance are robust. However, firm's performance and export statusbecome not significant in explaining firm's access to finance while foreign ownership of the firm becomes significant with a positive effect on firm's likelihood of having access to finance. The rest of the thesis is organized as follows. Section 2 reviews both the theoretical and empirical literature on private firms' access to finance. Section 3 presents the methodology used to investigate the determinants of firms' access to finance in Burkina Faso, but also discusses the data and variables used in the regression analysis. Section 4 discusses empirical results. Finally, Section 5 includesconclusions and policy recommendations. The theoretical literature dealing with access to finance can be divided into two sides. On one hand, we havetheoriesexplaining access to finance on the supply-side and on the other hand, theories explaining access to finance on the demand-side. On the supply-side, information asymmetry theory and credit rationing theory, help to understand the mechanisms behind the issue of private sector's access to external finance. The reluctance of lenders to provide finance to the private sector could be explained by information asymmetry theory by Akerlof, (1970). The decisions of lenders rely more on the quality of information needed to fund the firm's project. This information includes firm's financial statements, and the project's riskiness. The lower the quality of this information the more reluctant the lenders will be about financing the project and the higher will be the cost of the loan. This situation leads to the issue of «adverse selection» in which only most risky and bad quality projects will be funded instead of less risky and good quality projects. Therefore, to minimize the risk of selecting bad borrowers, lenders use a set of coping strategies that include screening mechanisms (Milde and Riley, 1988), collateral requirements, monitoring and incentives compatible debt contracts (Holmtrom and Tirole, 1997), and credit rationing (Stiglitz and Weiss, 1981). Moreover, the centralization of information at public credit registries and with private credit bureaus is a way to minimize the cost of information acquisition (Triki and Gajigo, 2003).Recently, this institution which did not exist before has been set up within the WAEMU countries in 2015. Even though financial institutions are guided by profit maximization objective, not all the firms who apply for financing are granted access. Thus, thesupply for credits does not adjust itself to the demand through the price mechanism. Firms may be denied credits even if they are willing to pay arbitrarily high interest rates. This phenomenon is known as credit rationing and it has been addressed theoretically by Stiglitz and Weiss (1981), who defined credit rationing as a situation in which there is an excess demand for commercial loans at the prevailing commercial loan rate. De Meza and Webb (1987) argue that the credit market is not like the normal market where demand is equivalent to supply as the borrowers who are willing to pay higher interest rates may find it difficult when it comes to repayments. Not only banks making loans are concerned about the interest rate they receive on the loan but also the riskiness of the loan. However, the interest rate a bank charges may itself affect the riskiness of the pool of loans by either: i) sorting potential borrowers which is «the adverse selection effect» or ii) affecting the actions of borrowers which is «the incentive effect» Stiglitz and Weiss (1981). Another factor that can explain private sector access to external finance on the supply-side is the structure of the credit market. The relationship between access to finance and the structure of the credit market is explained through two theories:market power theory and the information hypothesis theory. According to the market power theory, the effect of higher bank competition is double. On one hand, high bank concentration leads to lower costs and better access to finance (Besanko and Thakor, 1992; Guzman, 2000). On the other hand, in the presence of information asymmetries and agency costs, however, competition can reduce access by depriving banks of the incentive to build lending relationships (Petersen and Rajan, 1995). Other contributions point out that the quality of screening (Broecker, 1990; Marquez, 2002) and banks' incentives to invest in information acquisition technologies (Hauswald and Marquez, 2006) are higher in less competitive markets. Therefore, the information hypothesis theory shows that access to credit for opaque borrowers (most of the time MSMEs) can decrease when competition becomes tougher (Petersen and Rajan, 1995). On the demand-side, private sector access to external finance is explained by the relationship between the life cycle of the firm and its financial needs [Weinberg, (1994); Berger and Udell, (1998)]. During their life cycle, firms may experience three main stages of growth: start-up, growth and maturity. At the early stage of their growth, start-up firms are heavily dependent on initial insiderfinance, trade credit, and angel finance [see Sahlman (1990) and Wetzel, (1994)] because startupfirms are arguably the most informationally opaque and, therefore, have the most difficulty in obtainingintermediated external finance. Moreover, life-cycle pattern assumes that the ability of the manager which is low and uncertain for start-up firms is a relevant determinant of productivity and growth. However, over the time, as the firm survives and grows not only the ability of the manager improves by experience and becomes less uncertain, but also the quality of financial information statements improves. This pattern may explain why MSMEs have difficulties in accessing external finance but at a later stage of their growth the use of external financing by larger firms is not evident as at this stage they have ample internal funds that can be used to finance their investment needs. The issue of firms' access to financing has been widely analyzed in the empirical economic literature. However, papers dealing only with a country case study are very sparse. To our knowledge, we didn't find anyacademic paperdealing with the problem of private sector's access to financing in Burkina Faso. Thus, our review of the empirical literature is focused mostly on the papers dealing with SSA countries. To investigate the issue of the private sector access to finance, some papers made just an analyzing of both the supply side and the demand side of the problem based on the financial data available whereas some conducted more rigorous analysis by using qualitative econometric models. According to Aryeetey et al. (1994), Gockel and Akoena(2002), MSMEs access to finance in SSA is undermine by several factors belonging both to the supply side and the demand side such as inadequate finance, lack of managerial skills, equipment and technology, poor access to capital market, among others. The methodology used by these two papers was just based on an analyzing of the data of the financial system of Ghana. In the same vein using the same methodology, Sacerdoti, (2005) found that the inability to provide adequate financial statements and quality collateral reduce the chance of SMEs of accessing financial institutions. In addition to that the absence of credible credit reference bureaus in most countries in SSA and its attendant effect of interest rates could explain the chances of SMEs gaining access to finance (see Bass and Schrooten, 2005). Moreover, Buatsi, (2002) pointed out that Small and Medium-sale exporters in Ghana meet difficulties in accessing to finance because of the high level of interest rate, collateral and maladjustment of financial institutions financing products. Indeed, financial institutions prefer granting short-term credit to medium or long-term credit, and investing in government treasury bills and bonds rather than lending to SMEs firms.More recently, Ghandi and Amissah, (2014) examining the different options of financing for SMEs in Nigeria showed that inadequate collateral by SMEs operators, weak demand for the products of SMEs as a result of the dwindling purchasing power of Nigerians, lack of patronage of locally produced goods, poor management practices by SMEs operators and Undercapitalization explain why financial institutions are reluctant to extend credit to SMEs. The major issue encountered in the empirical literature is the oneof measurement of firms' «access» to finance.We meet two types of measurement in the empirical literature: subjective measures and objective measures. The subjective measuresare based on firms' perceptions of «access to finance»whilst the objective measuresare derived from financial statementslike for instance the shares of internal and external financial resources of working capital, and alsofrom hard data instead of perceptions data.Objective measures in developing countries are almost impossible because financial data is limited. Indeed, in developing countries SMEs are not required to file detailed financial reports as they don't raise equity or debt from public markets. Moreover, the use of aggregate measures of financial development is problematic as they do not provide the distribution of financing among such firms. That is why for Claessens and Tzioumis (2006) «the only way to investigate firms' problems accessing finance is trough tailored firm-level surveys directly addressing the issue of financing constraint» (page 6). Consequently, this explains the use of the World Bank Enterprises survey data for the current study. Kuntchev et al. (2013), using data from the World Bank's Enterprise Survey for 119 countries worldwide developed a new measureof credit-constrained status for firms using hard data instead of perceptions data.The paperclassifies firms into four ordinal categories: Not Credit Constrained (NCC), Maybe Credit Constrained (MCC),Partially Credit Constrained (PCC), and Fully Credit Constrained (FCC) to understand the characteristics ofthe firms that fall into each group. The paperfirst showed by using both statistical and econometrical (ordered logit and simple logit) methods, that SMEs are more likely to be creditconstrained (either partially or fully) than large firms.Moreover, SMEs tend to finance their working capital and investment using trade credit and informalsources of finance more frequently than large firms. Second, size is a significant predictor of theprobability of being credit constrained, firm age is not. Third, high-performing firms, asmeasured by labor productivity, are less likely to be credit constrained. Fourth, countries with highprivate credit-to-gross domestic product ratios, firms are less likely to be credit constrained. Finally, according to their findings, in developing countries access to credit is inversely related to firm size but positivelyrelated to productivity and the country'sfinancial deepening. Wang (2016) showed by using the Enterprise Survey data from the World Bank which covers data from 119 developing countries that SMEs perceive access to finance as the most significant obstacle which hinders their growth. The determinants among firms' characteristics(demand-side theory factors) are size, age and growth rate of firms as well as the ownership of the firm. This paper used an orderedprobit model and a subjective measure of access to financing based on firm's perception of the severity of access to financing. From the supply-side theory the paper pointed out that the main barriers to external financing are high costs of borrowing and a lack of consultant support. More recently, Quartey et al. (2017),using data from the World Bank's Enterprises Survey on the ECOWAS countries, examines the determinants of SMEs' access to finance both at the at the Sub-regional level and at the country-level. This paper used the two different measures of «access» to finance for the sake of robustnesschecking. They found that access to finance at the sub-regional level is strongly determined by factors such as firm size, ownership, strength of legal rights, depth of credit information, firm export orientation and experience of the top manager. At the country level, they found important differences in the correlates of firms' access to finance.It is worth noting that these findings at the country level considered only six countries that are Ghana, Mali, Senegal, Gambia, Guinea and Cote d'Ivoire. Burkina Faso as many other countries has been excluded because of data suitability and the 2014 ranking of «getting credit» distance to the frontier index of the countries in West Africa in 2014 according to the authors. As we can noticed the issue of access to finance has been widely discussed in the empirical literature. Most of the studies were interested in SMEs that is why they focused on the difficulties that SMEs face in their daily operations. Moreover, these studies used both objective and subjective measure of access to financing and analyzed the determinants of access to finance by using multinomial choice models like Ordered logit or ordered probit. In this thesis, in order to investigate the determinants of firm's access to financing, the objective measure proposed by Kuntchev et al. (20013) is used to estimate an ordered logit model. For robustness check, a subjective measure of firm's access to finance based on their perception is used. As mentioned in the empirical literature review, the main issue in assessing the determinants of private firms' access to finance is how to construct the access to finance variable. We use here the measure developed byKuntchev et al. (2013). This paper classified firms into four ordinal categories:i) Not Credit Constrained (NCC), ii) Maybe Credit Constrained (MCC),iii) Partially Credit Constrained (PCC), and iv) Fully Credit Constrained (FCC) in order to understand the characteristics ofthe firms that fall into each group. The conditions to be fulfilled by each firm aresummarized in the following Figure 4. Figure 4: Correspondence between Credit-Constrained Groups and Questions in Enterprise Surveys

Source:Kuntchev et al. (2013), Page 20 We can also summarize the description of each category in the following table 1. Table 1: measurement of access to finance measure as proposed by Kuntchev et al. (2013)

Source:Kuntchev et al. (2013), pages 9-11 By defining access to finance in such a way, the empirical modelsthat fit to analyze the determinants of private firms' access to finance in Burkina Faso are obviously ordinal choice models. The structural form of these models can be written as follows:

Where

Hence, the probability of observing the event of access to

finance is defined for each value of the dependantvariable · For

· For

· For

· For

where F(.) is the Cumulative Distribution Function (CDF) of

the error term As explained in the theoretical review, firm's access to financing is explained both by the demand-side and supply-side factors. In our case, firm's access to financing is a function of its own characteristics and those of the top manager. Firm's characteristics and those of the top manager capture the demand-side factors that can explain their access to financing. Due to the nature of our data (cross section) it is not possible to include in our model the supply-side variables that can affect firm's access to financing. Since the business environment and the financial market in Burkina Faso are common for every firm, it does not really matter not to take them into account in our model. Then the expression of our model is as follows:

Where Data are from the World Bank Enterprises Survey.This survey has been conducted in Burkina Faso from 15 May 2008 to 10 October 2009. The database containsinformation on 394 non-agricultural formal firms observed during this period. The whole population, or the universe, covered in the Enterprise Surveys is the non-agriculturaleconomy. It comprises all manufacturing sectors according to the ISICRevision 3.1 group classification (group D), construction sector (group F), services sectorgroups G and H), and transport, storage, and communications sector (group I). Note that this population definition excludes financial intermediation (group J), real estate and renting activities (group K, except sub-sector 72, IT, which was added to thepopulation under study), and all public or utilities-sectors. Our sample shows that SMEs dominates in Burkina Faso. Indeed, the proportion of Small, Medium and Large firms among non agricultural private firms in Burkina Faso represented respectively 59.14%, 30.96% and 9.9% (see appendix 1). SMEs represented 90.1% of non agricultural private firms and this is consistent with the general figure (84.3%) we gave above in section 1. Formal non agricultural firms in Burkina Faso were operating in 2009 mostly in the service sector especially in the retail sector (31.73%). The second sector is the whole sale sector with 13.96%. Construction, other manufacturing, hotel and restaurant, and transport represent respectively 9.64%, 8.12%, 6.35% and 6.09%.Information about the sectors in which these firms are operating are summarized in appendix 2. Appendix 3indicates the major business constraints for our sample on 394 private non-agricultural firms in Burkina Faso. Access to finance is perceived as the major constraints for these firms before tax rates and practices of competitors in informal sectors. According to the methodology of Kuntchev et al. (2013), the proportions of firms considered to be PCC, FCC, NCC and MCC are respectively 48.22%, 28.87%, 15.99% and 10.91% (see appendix 4). There are three main reasons why some firms did not apply for a loan are: (i) they don't need because they have enough capital (25.65%), (ii) collateral requirements are too high (19.92%), (iv) interest rates are not favorable (17, 89%) and (v) application procedures for loans or line of credit are complex (14.23%) (Seeappendix 5). According to these figures, the reasons why firms in Burkina Faso don't apply for a loan or credit line are mainly due to the financial system. Table 2 summarizes the description of each variable of the empirical model. It shows how each of them is measured and also gives thecategory of variables into which each variable falls. Table 2: Description of the variables

Source: Author

The results of the regression show that firm's size, firm's legal status, firm's performance measured by labor productivity and firm's export status have a negative and significant effect on the non agricultural private firms' likelihood to be credit constraint in Burkina Faso. Indeed, the bigger the firm most likely it is to be «non credit constraint» (NCC) and have access to finance. Moreover, the high performing the firm is most likelyit is to be «non credit constraint» and have access to finance. Also, Firms that produce for exportation are more likely to have access to finance compared to firms that produce only for the national market. Besides, sole proprietor firms are most likely to be fully credit constraints (FCC) and to meet difficulties in having access to finance. Our results on the effect of the firm's size and firm's performance are consistent with the findings of Quartey et al. (2016) for Ghana and Maliand also with those of Kuntchev et al. (2013) for sub-Saharan Africa. These finding are also consistent with the theory of firm's life cycle [see Weinberg, (1994); Berger and Udell, (1998)].On the contrary, while firm's legal status has a significant effect on the likelihood of firms to have access to financeKuntchev et al. (2013)found no significant effect of this variable. The same is true for the export status of the firm. Quartey et al. (2016) didnot find any significant effect of the export status on firm's access to finance at the regional level in ECOWAS. The results are summarized in the following table3. Table3: ordered logit (dependent variable: Access to finance, credit constraint status)

Dependent variable: access to finance (NCC=1, MCC=2, PCC=3, FCC=4). Robust standard errors in parentheses. *** indicates significance at 1% (p < 0.01) ** indicates significance at 5% (p < 0.05) * indicates significance at 10% (p < 0.10) In terms of magnitude, an increase of 10 percent of the firm size increases the likelihood of the firm to be Non Credit Constraint «NCC» by 0.26 percentage point, ceteris paribus. Similarly, an increase of 10 percent of the firm size decreases the probability of the firm to be Fully Credit Constraint «FCC» by 0.35 percentage point, ceteris paribus. Being a sole proprietor firm decreases the likelihood of the firm to be NCC by 7.2 percentage point. Sole proprietor firms are 9.2 percent more likely to be Fully Credit Constraint compared to the others, ceteris paribus. An increase of 10 percent of firm's performance increases the likelihood for this firm to be Non Credit Constraint by 0.23 percentage point. Also, an increase of 10 percent of the firm performance decreases the likelihood of the firm to be Fully Credit Constraint by 0.32 percentage point, ceteris paribus. Being an exporter firm increases the likelihood to be credit constraint by 6.9 percentage points, ceteris paribus. It also, decreases the likelihood of being Fully Credit Constraint by 7.4 percentage point. In a nutshell, our results have identify four determinants of access to finance for non agricultural formal firms in Burkina Faso that are firm's size, firm's legal status, firm's performance and firm's export status. We found those results by using an objective measure of access to finance proposed by Kuntchev et al. (2013). Are those findings in the case of Burkina Faso robust if we use a subjective measure of firm's access to finance based on their perception?In the following part of this section we make a robustness analysis. For the robustness check, we estimate another ordered logit model on the same independent variables, but we replaced the dependent variable by a subjective measure of firm's access to finance which is based on their perception.The subjective measure of access to finance is taking 5 modalities representing firm's perception of whether access to finance is an obstacle or not. Then the variable will take the values: 0=No obstacle, 1= Minor obstacle, 2= Moderate obstacle, 3= Severe obstacle, 4= Very severe obstacle. Firm's size matters for access to finance.Indeed, the effect is positive and statistically significant (see table 4). Compared to SMEs, large firms do not perceive access to finance as an obstacle because it is easier for them to raise money for their working capital and/or investment. This finding is consistent with the demand-side theory on firm's life cycle and robust in a sense that it confirms also our previous finding. Table4: ordered logit (dependent variable: degree of firm's perception of access to finance as a constraint)

Dependent variable: access to finance (No obstacle = 0, Minor obstacle = 1, Moderate obstacle = 2, Severe obstacle = 3, Very severe obstacle = 4). Robust standard errors in parentheses. *** indicates significance at 1% (p < 0.01) ** indicates significance at 5% (p < 0.05) * indicates significance at 10% (p < 0.10) Besides, firm's legal status is also statistically significant in explaining access to finance in a sense that sole proprietor firms are most likely to declare access to finance as very severe obstacle compared to partnership or shareholding firms. This result is also robust since it confirms previous finding. On the contrary, firm's performance does not have a significant effect on their perception on access to finance. Export status of the firm here has not a significant effect on the perception of firm access to finance as it was the case in the previous regression (table3). Moreover,a new finding here is that foreign owned firms are less likely to perceive access to finance as an obstacle. In terms of magnitude, an increase of 10 percent of the firm's size increases the likelihood of perceiving access to finance as not an obstacle by 0.043 percentage point. Similarly, an increase of the firm's size by 10 percent lead to a decrease in the likelihood of perceiving access to finance as very severe obstacle by 0.54 percentage point. Being a sole proprietor firm increases the likelihood of perceiving access to finance as a very severe obstacle by 9.24 percentage points. Also, being a foreign owned firm decreases the likelihood of perceiving access to finance as a very severe obstacle by about 21 percentage points. * 1The sample of Stampini et al., 2011 covered 50 African countries (all but Zimbawe, Somalia and Eritrea). * 2 Chapter 1 :The Role of the Private Sector in Africa's Economic Development, P.21 * 3 For Mali the proportion is measured in 2010. |

| |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

is alatent variable measuring access to finance for the firm i,

is alatent variable measuring access to finance for the firm i,

represents a vector of variables that capture firm's characteristics

and those of the top manager.

represents a vector of variables that capture firm's characteristics

and those of the top manager.

is a vector of parameters to be estimate and

is a vector of parameters to be estimate and

stands for the error term.As

stands for the error term.As

is unobservable, we defined

is unobservable, we defined

that takes the values 1, 2, 3 and 4 respectively when the firm falls in

the NCC category, MCC category, PCC category and FCC category. Thus, we can

define the choice rule as:

that takes the values 1, 2, 3 and 4 respectively when the firm falls in

the NCC category, MCC category, PCC category and FCC category. Thus, we can

define the choice rule as:

:

:

. If we assume that

. If we assume that

is normally distributed, then we run an ordered probit model. On the

contrary, if we assume that the distribution of

is normally distributed, then we run an ordered probit model. On the

contrary, if we assume that the distribution of

is the logistics one, then we run an ordered logit model. In this

thesis, logisticsdistributionis assumed.

is the logistics one, then we run an ordered logit model. In this

thesis, logisticsdistributionis assumed.

is the dependantvariable measuring access to finance for the firm i and

taking the values, 1 for NCC, 2 for MCC, 3 for PCC and 4 for FCC. The dependent

variable

is the dependantvariable measuring access to finance for the firm i and

taking the values, 1 for NCC, 2 for MCC, 3 for PCC and 4 for FCC. The dependent

variable

is a function of firm's characteristics (Firm's age, Firm's size,

legal status, sector of activity, export status labor productivity and Foreign

ownership), and those of the top manager (Top manger education, Top

manger experience and gender). The parameters to be estimated are

is a function of firm's characteristics (Firm's age, Firm's size,

legal status, sector of activity, export status labor productivity and Foreign

ownership), and those of the top manager (Top manger education, Top

manger experience and gender). The parameters to be estimated are

with i= 1, 2, 3... 10. The error term is represented by

with i= 1, 2, 3... 10. The error term is represented by

.

.