Modeling and forecasting inflation in Rwanda (1995-2009)( Télécharger le fichier original )par Ferdinand GAKUBA Kigali Independent University - Degree in economics 2009 |

My dear parents. uman beings who are the most to me dear: Nothing in the world could compensate the sacrifices you have

made for my Thank you for your help, your support and your patience. I

dedicate this modest work

I would like to express my gratitude and respectful appreciation to everyone who helped me close or far in the achievement of this work, and more particularly to: Honorable Senator Professor Dr. RWIGAMBA BALINDA, Founder and President of ULK, for his initiative and innovation for the development of education in our country. We also wish to thank the Rector of ULK Dr. Alphonse NGAGI and Faculty of ULK more specially those of the Faculty of Economics and Management, especially those of the Economics Department for the scientific support we receive from them. My gratitude will also to CCA Mme Brigitte GAJU, my direct supervisor for the follow-up given to the conduct of this work: I am very grateful have framed me, lead this work and to ensure its development in not gentle your time or your advice. Be ensured, expensive Supervisor, yours and have my deep respect. To my classmates of the 4th year in economics at ULK, promotion 2008 / 2009. We spent of pleasant brotherhood, of camaraderie, effort and perseverance, I hope you all will have one long career in economics and a better life both in terms Professional staff. To all those showing me their sympathy and that I consider as friends full. Besides my project, I really enjoyed my stay at the NBR, appreciated all the people I worked with and spent good moments with them. That's why I also thank Mr. Boniface MUTABAZI manager of middle office and Pascal MUNYANKINDI for all kind of help. Can God bless you and enables you to perform all your projects and your aspirations! Ferdinand GAKUBA

ADF: Augmented Dickey Fuller AER: Average Exchange rate ARCH: Autoregressive Conditional Heteroskedasticity BNR: National bank of Rwanda CCI: Continuous commodity index CIF: Cost, insurance and freight COLA: Cost of Living Allowance COLI: Cost of living index CPI: Consumer price index CRB: Commodity research bureau ECI: Employment cost index ECM: Error correction model EURO: European Money GBP: Great Britain Pound GDP: Gross domestic production IMF: International Monetary Fund LR: Likelihood ratio MINECOFIN: Ministère de la finance NSSF: National social security fund OLS: Ordinary Least square PCEPI: Personal consumption expenditure price index PPI: Producer price index RBD: Real bill doctrine RWF: Rwanda franc ULK: Université Libre de Kigali ULC : Unit labour cost. USA: United State of America VAR: Vector autoregressive VECM: Vector error correction model

Table 2: ADF Statistics for Testing for a Unit Root in all Time Series 34 Table 3: Cointegration analysis in the mark-up model 35 Table 4: Results using OLS 36 Table 5: Properties of VAR residuals 37 Table 6: Standardized adjustment coefficients 38 Table 7: Properties of cointegration vector 38 Table 8: Results for long run inflation model 40 Table 9: Heteroskedasticity test 41 Table 10: Ramsey RESET test 42 Table 11: White test 48 Table 12: ARCH test 48 Table 13: Breusch -Godfrey Test 48 Table 14: Ramsey test 2 49 Table 15: Diagnostic test 52 Table 16: Prevision results 59

Figure 1: Evolution of Inflation in Rwanda 25 Figure 2: Evolution of money supply and CPI 26 Figure 3: Evolution of import prices and domestic prices 27 Figure 4: Evolution of Output and inflation 29 Figure 5: CUSUM Test 42 Figure 6: CUSUM squared test 43 Figure 7: CUSUM stability test (Brown, Durbin, Ewans) 49 Figure 8: CUSUM squared stability test 49 Figure 9: Residuals test 52 Figure 10: Cusum test for Engle- Granger ECM 53 Figure 11: Cusum of squared test for Engle- Granger ECM 53 Figure 12: Inflation forecasting criteria 54 Figure 13: Response function of variables on LIPC 57

Appendix 1: Data description Appendix 2: Data Appendix 3: Residuals properties Appendix 4: VECM results Appendix 5: Variance decomposition Appendix 6: Recursive coefficient test Appendix 7: ECM with Hendry results Appendix 8: ECM with Engle- Granger results

Acknowledgment iiList of acronyms and abbreviations iiiLIST OF TABLE iv LIST OF FIGURE v LIST OF APPENDIX v TABLE OF CONTENTS vii Abstract 1 GENERAL INTRODUCTION 2

CHAPTER I LITERATURE REVIEW 8 1.1. Introduction 8 1.1.1 Inflation 8 1.1.2 Modeling inflation 9 1.1.3 Forecasting inflation 9 1.1.4 Measures of inflation 9 1.2. .Theory of inflation 10 1.2.1 Keynesian view 11

13 ons theory 14 1.2.4 Austrian theory 14 1.2.5 The theory of real bills doctrine 15 1.2.6. Anti-classical or backing theory 16 1.3 The tools for controlling the inflation 16 1.3.1. Monetary policy 16 1.3.2 Fixed exchange rates 17 1.3.3 Wage and price controls 17 1.3.4 Cost-of-living allowance 18 1.4 The history of modeling and forecasting inflation process 19 1.4.1 Some critical issues for modelling 22 1.4.2 Overview of forecasting 22 1.4.2.1 Monetary transmission 23 1.4.2.2. Flexible price equilibrium 24 CHAPTER II. INFLATION MODELLING AND CONCEPTUAL FRAMEWORK 25 2.1. Rwanda's inflation experience 25 2.1.1. Foreign factors 27 2.1.2 Domestic factors 28 2.2. Conceptual framework 29 2.2.1. LONG- RUN RELATIONSHIPS 30 2.2.1.1. Mark up 30 2.2.1.2 Money supply determinants 31 2.2.2. Data descriptions 32 2.3. Estimation of inflation models 33 2.3.1. Mark up 33 2.3.1.1 Integration 33 2.3.1.2. Cointegration 34 2.3.2 Excess money supply 37 2.4 THE LONG RUN MODEL OF INFLATION 38 2.4.1 Interpretation of coefficients 41 2.4.2 Classical Tests 41 CHAPTER III FORECAST INFLATION OF RWANDA USING ECM 45 3.1 Introduction 45

inflation 45 45 3.2.1.1 Long run and short run elasticity 46 3.2.1.2 Significativity of error correction model 47 3.2.2 The ECM with Engle - Granger 50 3.2.2.2 The model properties 52 3.3. Forecasting inflation using VECM 55 3.3.1 Why a VECM? 55 3.3.2. Forecasting performance 56 3.3.2.1 The variance decomposition 58 .3.3.2.2 Forecast results 58 General conclusion 59 Discussion 63 References 64 APPENDIX 67

Inflation constitutes one of the major economic problems in emerging market economies that requires monetary authorities to elaborate tools and policies to prevent high volatility in prices and long periods of inflation. Analysis of inflation and its relationship with the important macroeconomic indicators is an arduous task due to data problems (availability, measurement errors, biases, etc.) and complexity of the transition process experienced by the economy of Rwanda. In order to model inflation dynamics we use the general-to-specific approach. The advantage of this approach is its ability to deliver results based on underlying economic theories of inflation, which are also consistent with the properties of the data. A three steps procedure is followed. In the first step, the long-run sectoral analysis of inflation sources is conducted, yielding long-run determinants of inflation (excess money, nominal effective exchange rate, nominal wages expressed as unit labor cost, import prices, oil prices index and the nominal GDP). In the second step, we estimate an equilibrium error correction model first of all by following Hendry procedures, then building ECM by Engle Granger and compare forecasting criteria of inflation deploying among other variables of interest for the long-run solutions derived in the first step. Lastly, equilibrium error correction model obtained will serve for structural model-based inflation forecasting. Forecasting performance of the model will be compared to other models often utilized for forecasting inflation suggests that markup and excess money relationships are very important for explaining the short-run behaviour of inflation, as well as the output, nominal effective exchange rate, oil prices and import prices in Rwanda.

1. Interest and choice of subject 1.1. ChoiceThe aim of this paper is to construct a quarterly inflation model and forecasts quarterly-year ahead inflation for Rwanda. Inflation is considered to be a major economic problem in transition economies and thus fighting inflation and maintaining stable prices is the main objective of monetary policy makers. The negative consequences of inflation are well known. Inflation can result in a decrease in the purchasing power of the national currency leading to the aggravation of social conditions and living standards. High prices can also lead to uncertainty making domestic and foreign investors reluctant to invest in the economy. Moreover, inflated prices worsen the country's terms of trade by making domestic goods expensive on regional and world markets. To develop an effective monetary policy, central banks should possess information on the economic situation in the country, the behaviour and interrelationships of major macroeconomic indicators. Such information would enable the central bank to predict future macroeconomic developments and to react in a proper way to shocks the economy is subject to. Thus, studying inflationary processes is an important issue for monetary economists all around the world. However, it is not an easy task, especially in developing countries, where economic processes are highly unstable and volatile. Moreover, the macroeconomic data on developing countries can be unreliable due to many reasons: measurement error, imperfect methods of measuring, etc. Nevertheless, there exist a number of empirical studies on inflation factors in developing countries. Since inflation is a phenomenon that characterizes almost all economies as it is developed or not, but particularly developing countries including our country is, within this framework that we considered relevant to the topic, hence the rationale for choosing this subject.

At academic level, this work will constitute an important source of data, both theoretical and practical, researchers, students from different faculties, professors, and all the whole community who will look for modelling and forecasting inflation in their research. This topic has the interest to deepen our understanding of inflation models and its prediction in the context of developing economy and make our contribution to science. This topic has the interest to know the relationship of inflation with others macroeconomic variables

Since Rwanda covered its monetary sovereignty the monetary policy followed was with a direct character thus straightforwardly to manage the banking function this means that the development of its activities was to be contained within the limits deemed compatible with the overall trend of discounting the economy to avoid any risk of deviation1. This policy has been unchanged until the end of the Eighties years but like almost everywhere in the world, managed finance proved in Rwanda inefficient and its prevalence has violated not only the conditions of financing the economy but also, and especially, the allowance of the financial resources available and hence two major consequences could appear; the absence of optimal allowance of the financial resources available and sometimes even by monetary creation ex nihilo (excess 1 Ia politique monétaire au Rwanda; une mutation constante pour une efficience accrue, juin, 2003

g 1990 its was the first foreground of structural chanism started coming into force then replace the procedures of administrative management. The direct control operated before on both sides by the concerned official structures thus had to disappear gradually and free plan of the supply and the demand were to allow the determination of the different price level of the various markets. The monetary policy of Rwanda was the subject of a deep change with the imminent emergence of new instruments of the monetary policy which had some modification of the structure to even giving a more and more accentuated at indirect character. Final objective is the price stability (ultime objective) but the achievement of this objective is conditioned by another intermediate objective that constitutes a walking point which is a vital crossing point of the action of central bank initiated in this context. It acts in the case of Rwanda by controlling the evolution of money supply expressed in a broad sense (M2). Achieving the goal also requires an intermediate operational target which in the context of Rwanda is the monetary base by considering the multiplier stable. Monetary management ensured by the central Bank of Rwanda still faced major obstacles which affecting more the quality of the results obtained because the lack of a management model that can serve as tool for projecting future, this hampers monetary policy and reach on the price volatility persistence which is his ultimate goal. The aim of this study is to build a model for the money supply and to build a model of inflation which can be used to forecast the future uncertain. This allows as formulating the following assumptions;

4. HYPOTHESIS A hypothesis is an early response to questions that arose in the problem and must be confirmed to achieve a result.

hypotheses: d by excess money supply, However there are other factors like, low level of production, high wages, high level of import rising market prices, nominal exchange rates, and macroeconomic instability, etc.

Some Keynesian economists also disagree with the notion that central banks fully control the money supply, arguing that central banks have little control, since the money supply adapts to the demand for bank credit issued by commercial banks20. This is known as the theory of endogenous money, and has been advocated strongly by post-Keynesians as far back as the 1960s. It has today become a central focus of Taylor rule advocates. This position is not universally accepted banks create money by making loans, but the aggregate volume of these loans diminishes as real interest rates increase. Thus, central banks can influence the money supply by making money cheaper or more expensive, thus increasing or decreasing its production. A fundamental concept in inflation analysis is the relationship between inflation and unemployment, called the Phillips curve. This model suggests that there is a trade-off 17 http://www.bized.co.uk/virtual/bank/economics/mpol/inflation/causes/theories1.htm,Retrieved 1/11/2009 18 Encyclopedia Britannica, "The cost-push theory" 19 http://en.wikipedia.org/wiki/Built-in_inflation, Retrieved 1/11/2009

oyment. Therefore, some level of inflation could be minimize unemployment. The Phillips curve model described the U.S. experience well in the 1960s but failed to describe the combination of rising inflation and economic stagnation (sometimes referred to as stagflation) experienced in the 1970s21 1.2.2 Monetarist view Monetarists believe the most significant factor influencing inflation or deflation is the management of money supply through the easing or tightening of credit. They consider fiscal policy, or government spending and taxation, as ineffective in controlling inflation22. Monetarists assert that the empirical study of monetary history shows that inflation has always been a monetary phenomenon. The quantity theory of money, simply stated, says that the total amount of spending in an economy is primarily determined by the total amount of money in existence. This theory begins with the identity: Where; M is the quantity of money. V is the velocity of money in final expenditures; P is the general price level; Q is an index of the real value of final expenditures; In this formula, the general price level is affected by the level of economic activity (Q), the quantity of money (M) and the velocity of money (V). The formula is an identity because the velocity of money (V) is defined to be the ratio of final expenditure to the quantity of money (M). Velocity of money is often assumed to be constant, and the real

value of output is 20 Gordon, Robert J. (2000), "Does the 'New Economy' measure up to the great Inventions of the Past?", Journal of Economic Perspectives 14 (4): 49-74 21 Mankiw 2002,Macroeconomics principles, p. 65-77

f the change in the general price level is changes in nstant velocity, the money supply determines the value of nominal output (which equals final expenditure) in the short run. In practice, velocity is not constant, and can only be measured indirectly and so the formula does not necessarily imply a stable relationship between money supply and nominal output. However, in the long run, changes in money supply and level of economic activity usually dwarf changes in velocity. If velocity is relatively constant, the long run rate of increase in prices (inflation) is equal to the difference between the long run growth rate of money supply and the long run growth rate of real output23. 1.2.3. Rational expectations theory Rational expectations theory holds that economic actors look rationally into the future when trying to maximize their well-being, and do not respond solely to immediate opportunity costs and pressures24. In this view, while generally grounded in monetarism, future expectations and strategies are important for inflation as well. A core assertion of rational expectations theory is that actors will seek to "head off" central-bank decisions by acting in ways that fulfill predictions of higher inflation. This means that central banks must establish their credibility in fighting inflation, or have economic actors25 make bets that the economy will expand, believing that the central bank will expand the money supply rather than allow a recession. 1.2.4 Austrian theory The Austrian School asserts that inflation is an increase in the money supply, rising prices are merely consequences and this semantic difference is important in defining inflation26 Austrian economists believe that there is no material

difference between the 22 Lagassé, Paul (2000).Columbia encyclpedia,ISBN-10 0787650153 page 556-558 23 Mankiw 2002, Macroeconomics principles, pp. 81-107 24 Dowyer,J.and R. Lam (1994), Economic and Financial Research in the Reserve Bank in 1994 25 Sargent, Thomas J. Rational Expectations and Inflation. New York: Harper and Row, 1986. 26 Shostak, Ph. D, Frank (2002-03-02). "Defining Inflation". Mises Institute. http://mises.org/story/908. Retrieved 2009-10-10 lculating the growth of new units of money that are change, that have been created over time27.

This interpretation of inflation implies that inflation is always a distinct action taken by the central government or its central bank, which permits or allows an increase in the money supply28. In addition to state-induced monetary expansion, the Austrian School also maintains that the effects of increasing the money supply are magnified by credit expansion, as a result of the fractional-reserve banking system employed in most economic and financial systems in the world29 Austrians argue that the state uses inflation as one of the three means by which it can fund its activities (inflation tax), the other two being taxation and borrowing. Various forms of military spending is often cited as a reason for resorting to inflation and borrowing, as this can be a short term way of acquiring marketable resources and is often favored by desperate, indebted governments30. 1.2.5 The theory of real bills doctrine Within the context of a fixed species basis for money, one important controversy was between the quantity theory of money and the real bills doctrine (RBD). Within this context, quantity theory applies to the level of fractional reserve accounting allowed against specie, generally gold, held by a bank. Currency and banking schools of economics argue the RBD, that banks should also be able to issue currency against bills of trading, which is "real bills" that they buy from merchants. This theory was important in the 19th century in debates between "Banking" and "Currency" schools of monetary soundness, and in the formation of the Federal Reserve. In the wake of the collapse of the international gold standard post 1913, and the move towards deficit financing of government, RBD has remained a minor topic, primarily of interest in limited contexts, such as currency boards. It is generally held in ill repute today, with Frederic Mishkin, a governor of the Federal Reserve going so far as to say it had been "completely discredited." Even so, it has theoretical support from a few 27 Joseph T. Salerno, (1987), Austrian Economic Newsletter, "<a href=" http://www.mises.org/journals/aen Retrieved 2009-10-10 28 Ludwig von Mises Institute, "True Money Supply; page 456 29 Joseph T. Salerno, (1987),Quarterly Journal of economics Facts, Discussion Forum -356

at see restrictions on a particular class of credit as nciples of laissez-faire, even though almost all libertarian economists are opposed to the RBD. The debate between currency, or quantity theory, and banking schools in Britain during the 19th century prefigures current questions about the credibility of money in the present. In the 19th century the banking school had greater influence in policy in the United States and Great Britain, while the currency school had more influence "on the continent", that is in non-British countries, particularly in the Latin Monetary Union and the earlier Scandinavia monetary union31. 1.2.6. Anti-classical or backing theory Another issue associated with classical political economy is the anti-classical hypothesis of money, or "backing theory". The backing theory argues that the value of money is determined by the assets and liabilities of the issuing agency32. Unlike the Quantity Theory of classical political economy, the backing theory argues that issuing authorities can issue money without causing inflation so long as the money issuer has sufficient assets to cover redemptions. 1.3 The tools for controlling the inflation A variety of methods have been used in attempts to control inflation. 1.3.1. Monetary policy Monetarists emphasize keeping the growth rate of money steady, and using monetary policy to control inflation (increasing interest rates, slowing the rise in the money supply). Keynesians emphasize reducing aggregate demand during economic expansions and increasing demand during recessions to keep inflation stable. Control of aggregate demand can be achieved using both monetary policy and fiscal policy (increased taxation or reduced government spending to reduce 30 Ludwig von Mises, The Theory of Money and Credit, page23-56 31 Selgin, G. A, "The Analytical Framework of the Real Bills Doctrine",Journal of Institutional and Theoretical Economics, volume 145, (1989), p. 489. 32 Ron Paul, "The Case for Gold, page 45-56 l for controlling inflation is monetary policy. Most ping the federal funds lending rate at a low level.

1.3.2 Fixed exchange rates Under a fixed exchange rate currency regime, a country's currency is tied in value to another single currency or to a basket of other currencies (or sometimes to another measure of value, such as gold). A fixed exchange rate is usually used to stabilize the value of a currency, vis-à-vis the currency it is pegged to. It can also be used as a means to control inflation. However, as the value of the reference currency rises and falls, so does the currency pegged to it. This essentially means that the inflation rate in the fixed exchange rate country is determined by the inflation rate of the country the currency is pegged to. In addition, a fixed exchange rate prevents a government from using domestic monetary policy in order to achieve macroeconomic stability. Under the Bretton Woods agreement, most countries around the world had currencies that were fixed to the US dollar. This limited inflation in those countries, but also exposed them to the danger of speculative attacks. After the Bretton Woods agreement broke down in the early 1970s, countries gradually turned to floating exchange rates. However, in the later part of the 20th century, some countries reverted to a fixed exchange rate as part of an attempt to control inflation. This policy of using a fixed exchange rate to control inflation was used in many countries in South America in the later part of the 20th century (e.g. Argentina (1991-2002), Bolivia, Brazil, and Chile)33. 1.3.3 Wage and price controls Another method attempted in the past has been wage and price controls ("incomes policies"). Wage and price controls have been successful in wartime environments in combination with rationing. However, their use in other contexts is far more mixed. Notable failures of their use include the 1972 imposition of wage and price controls 33 Edwards, Sebastian. (2002) The Great Exchange Rate Debate after Argentina, The North American Journal of Economics and Finance, Volume 13, Issue 3, pp. 237-252 essful examples include the Prices and Incomes enaar Agreement in the Netherlands.

In general wage and price controls are regarded as a temporary and exceptional measure, only effective when coupled with policies designed to reduce the underlying causes of inflation during the wage and price control regime, for example, winning the war being fought. They often have perverse effects, due to the distorted signals they send to the market. Artificially low prices often cause rationing and shortages and discourage future investment, resulting in yet further shortages. The usual economic analysis is that any product or service that is under-priced is over consumed. However, in general the advice of economists is not to impose price controls but to liberalize prices by assuming that the economy will adjust and abandon unprofitable economic activity. The lower activity will place fewer demands on whatever commodities were driving inflation, whether labor or resources, and inflation will fall with total economic output. This often produces a severe recession, as productive capacity is reallocated and is thus often very unpopular with the people whose livelihoods are destroyed. 1.3.4 Cost-of-living allowance The real purchasing-power of fixed payments is eroded by inflation unless they are inflation-adjusted to keep their real values constant. In many countries, employment contracts, pension benefits, and government entitlements (such as social security) are tied to a cost-of-living index, typically to the consumer price index35. A cost-ofliving allowance (COLA) adjusts salaries based on changes in a cost-of-living index. Salaries are typically adjusted annually. They may also be tied to a cost-of-living index that varies by geographic location if the employee moves. Annual escalation clauses in employment contracts can specify

retroactive or future 34Richard Milhous Nixon (January 9, 1913 - April 22, 1994) was the 37th President of the United States (1969- 1974) and is the only president to resign the office. He was also the 36th Vice President of the United States (1953-1961). See bibliography USA president

colloquially referred to as cost-of-living adjustments se of their similarity to increases tied to externally-determined indexes. Many economists and compensation analysts consider the idea of predetermined future "cost of living increases" to be misleading for two reasons:

1.4 The history of modeling and forecasting inflation process Since inflation was an economic issue numerous attempt to model inflation in developed countries as well as developing countries was made. For example, Juselius (1992) in her seminal paper on inflation modeling in a small open economy studied the inflationary processes in Denmark. De Brower and Ericsson (1998) wrote an appealing paper on inflation modeling in Australia. Both studies serve as important theoretical and methodological references for our later empirical research in the field of macroeconomic modeling. Welfe (2000) modeled inflation in Poland, accounting for a number of important features that characterize a transition economy. Besides these, worth noting are Ramakrishnan and Vamvakidis (2002)who worked on a model to forecast inflation behavior in Indonesia, and Callen and Chang (1999) who conducted an empirical study on inflation in India. Most of the literature in the field constitutes empirical studies for modeling inflationary processes in different countries and inflation factors in general. These studies follow approaches based on different economic theories, choosing the most appropriate for the economy investigated. 35 DeLong, Brad.

«Why Not the Gold Standard?»

http://www.j-bradford-

nflation, the study by Loungani and Swagel (2001) s a starting point for understanding inflation in developing countries. The authors present stylized facts about inflation behavior in developing countries, focusing primarily on the relationship between the exchange rate regime and the sources of inflation. Another important study of inflationary processes was accomplished by Fischer, Sahay, and Végh (2002) on the experiences of hyper and high inflations in various countries. The authors found that there is a very strong relationship between money growth and inflation both in the long and short run. Golinelli and Orsi (2002) study the inflation processes in three new EU member countries: the Czech Republic, Hungary and Poland. All three countries possess a similar historico- conomic background and similar economic context: they were administrative economies before and have undergone major systemic changes during the transition to a market economy. Investigating inflationary processes in these countries is of great importance because all countries experienced high inflation episodes during the years of transition, and price stabilization policies played an important role in their successful transition to a new economic system. The authors follow a methodology very close to that of Juselius (1992) in modeling inflation behavior in the countries under consideration. They use the multivariate VAR approach, grouping together those determinants that belong to main inflation theories: cost pushed inflation, foreign prices and exchange rates, and excess money. Further, a vector equilibrium correction model specification is used since it enables capturing short-term dynamics by including stationary variables and past imbalances, i.e.the «gaps» detected by previous cointegrated relationships. In his study on the determinants of inflation in Ukraine, the author, Lissovolik (2003), studies the factors of inflation in Ukraine during the period from 1993 to 2002, the so-called «transition period». The most relevant stylized facts important for modeling inflation behavior in Ukraine appear to be domestic financial instability, external disequilibria, seasonality of the economy, and allowance for an increase in administered prices. The resulting equation of an inflation model is a version of a long-term markup of prices over wages, the exchange rate, administrative prices, short-term factors and dummy variables.

are concerned with the problem of significant dollarization in transition economies, and its impact on the money demand and inflation. In particular, the authors study the case of Russia, and illustrate that all the measures of money aggregates that exclude foreign currency are negatively correlated with the nominal depreciation rate. This could suggest that foreign currency has been an important substitute for domestic money. The authors estimate an equilibrium correction model (ECM) for inflation in order to identify how the short-term dynamics of inflation are affected by deviations from the long-term money demand equation. They found that inflation does not react significantly to the excess supply of monetary aggregates that exclude foreign currency. Payne (2002) explores inflationary dynamics in Croatia using vector auto regression over the period January 1992-December 1999. The VAR incorporated four variables: broad money supply, retail price index1, nominal net wage per employee and the nominal effective exchange rate36. The model results suggest that wage increase and currency depreciation are positively correlated with inflation rates. Building on Paynes model, BotriL and Cota (2006) model Croatian inflation dynamics using structural vector autoregression37. Thay found that terms of trade and balance of payment shocks have the strongest impact on prices. The authors find justification for such result in Croatia being a small open economy with high import dependency and uncompetitive economic structure. In order to contrast these findings, the authors also re-estimated Paynes model. While Paynes conclusion on influence of wages and currency depreciation on prices still holds, in newly estimated four-variable VAR positive correlation between broad money and prices and some inflation inertia also emerged. 36 Payne, James E., 2002, «Inflationary Dynamics of a Transition Economy: the Croatian Experience», Journal of Policy Modeling, 24(3), pp. 219-30. 37 Botri[I, Valerija and Boris Cota, 2006, «Sources of Inflation in Transition Economy: The Case of Croatia», Ekonomski pregled, 57(12), pp. 835-855.

The quantitative macroeconomic modelling fell out of favour during the 1970s for two related reasons: First, some of the existing models, like the Wharton econometric model and the Brookings model, failed spectacularly to forecast the stagflation of the 1970s. Second, leading macroeconomists levelled harsh criticisms of these frameworks. Lucas (1976) and Sargent (1981), for example, argued that the absence of an optimization-based approach to the development of the structural equations meant that the estimated model coefficients were likely not invariant to shifts in policy regimes or other types of structural changes. Similarly, Sims (1980) argued that the absence of convincing identifying assumptions to sort out the vast simultaneity among macroeconomic variables meant that one could have little confidence that the parameter estimates would be stable across different regimes. These powerful critiques clarified why econometric models fit largely on statistical relationships from a previous era did not survive the structural changes of the 1970s. 1.4.2 Overview of forecasting Forecasting inflation is clearly of critical importance to the conduct of monetary policy, regardless of whether or not the central bank has a numerical inflation target.There are many literatures about inflation forecast for example using the generalized Phillips curves (i.e. using forecasting models where inflation depends on past inflation, the unemployment rate and other predictors) developed by Dimitris K.(2009)38 This literature is too voluminous to survey here, but a few representative and influential papers include Ang, Bekaert and Wei (2007), Atkeson and Ohanian (2001), Groen, Paap and Ravazzolo (2008) and Stock and Watson (1999). The details of these papers differ, but the general framework involves a dependent variable such as inflation (or the change in inflation) and explanatory variables including lags of inflation, the unemployment rate and other predictors. Recursive,regression-based methods, have had some success. However, three issues arise when using such methods. 38Gary K. and Dimitris K.(2009); Forecasting Inflation Using Dynamic Model Averaging, University of Strathclyde, June 2009

edictors can change over time. For instance, it is commonly thought that the slope of the Phillips curve has changed over time. If so, the coefficients on the predictors that determine this slope will be changing (Stock and Watson, 1996). Second, the number of potential predictors can be large. For instance, Groen, Paap and Ravazzolo (2008) consider ten predictors. Researchers working with factor models such as Stock and Watson (1999) typically have many more than this. The existence of so many predictors can result in a huge number of models. Third, the model relevant for forecasting can potentially change over time. For instance, the set of predictors for inflation may have been different in the 1970s than now or some variables may predict well in recessions but not in expansions. This kind of issue further complicates an already difficult econometric exercise39. Among other things, we describe the key differences with respect to the earlier generation of macro models. In doing so, we highlight the insights for policy that these new frameworks have to offer. In particular, we will emphasize two key implications of these new frameworks. 1.4.2.1 Monetary transmission Monetary transmission depends critically on private sector expectations of the future path of the central bank's policy instrument, the short-term interest rate. Ever since the rational expectations revolution, it has been well understood that the effects of monetary policy depend on private sector expectations. This early literature, however, typically studied how expectations formation influenced the effect of a contemporaneous shift in the money supply on real versus nominal variables (for example, Fischer, 1977; Taylor, 1980). In this regard, the new literature differs in two important

ways. First, as we discuss 39 Stock, J. and Watson M., 1999. Forecasting inflation: Journal of Monetary Economics 44, 293-335.

er the structural equations, since these aggregate king decisions by individual households and firms. As a consequence, the current values of aggregate output and inflation depend not only on the central bank's current choice of the short-term interest rate, but also on the anticipated future path of this instrument. The practical implication is that how well the central bank is able to manage private sector expectations about its future policy settings has important consequences for its overall effectiveness. Put differently, in these paradigms the policy process is as much, if not more, about communicating the future intentions of policy in a transparent way, as it is about choosing the current policy instrument. In this respect, these models provide a clear rationale for the movement toward greater transparency in intentions that central banks around the globe appear to be pursuing. 1.4.2.2. Flexible price equilibrium The natural (flexible price equilibrium) values of both output and the real interest rate provide important reference points for monetary policy and may fluctuate considerably. While nominal rigidities are introduced in these new models in a more rigorous manner than was done previously, it remains true that one can define natural values for output and the real interest rate that would arise in equilibrium if these frictions were absent. These natural values provide important benchmarks, in part because they reflect the (constrained) efficient level of economic activity and also in part because monetary policy cannot create persistent departures from the natural values without inducing either inflationary or deflationary pressures. Within traditional frameworks, the natural levels of output and the real interest rate are typically modeled as smoothed trends. Within the new frameworks they are modelled explicitly. This book has two broad goals. The first goal is to present econometric evidence on which type of monetary policy rule is likely to be both efficient and robust when used as a guideline for the conduct of monetary policy in Rwanda. The second goal is to answer several current monetary policy questions such as the effects of uncertainty about potential GDP growth or the role of the inflation rate in the setting of interest rates that are most naturally addressed within a framework of monetary policy rules.

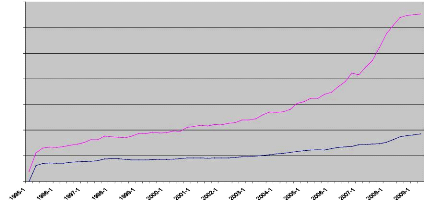

ELLING AND CONCEPTUAL FRAMEWORK A main objective of this chapter is to find the relevant long- run relationships of inflation and economics variables which driver the Rwanda inflation and to examine whether we can come up with a reasonable inflation function by imposing these relationships as equilibrium corrections terms. This chapter will help to answer the first of assumption which state as; inflation is in Rwanda a monetary phenomenon? And what are the drivers it in Rwanda? 2.1. Rwanda's inflation experience Inflation in Rwanda over the past fifteen years has been mainly influenced by the excess money supply and the nature of import arrangement and the country's openness. Over these fifteen years ago the evolution of inflation has been notably similar to that in developed countries and some in developing countries in the region. Figure 1: Evolution of Inflation in Rwanda IPC

Source: Author plotting (see appendix 2) On the right side (axis) there evolution in year starting by 1995 until 2009 and on the left hand (absisse) are rate of increase by quarterly basis as we see on the figure 1 since the 1995 the inflation rise with a constant rate of 0.3% but during 2006 the rate change 0.6% which is high movement of change until 2009 this was due to first of all the increase in salaries in 2006 and 2008 the oil shocks.

in Rwanda started to rise in the middle of 2007 8 as result of the oils price shocks. However the rise observed in mid 1998 was due to genocide event which hit all economics sector and kill around one million of Rwandan people and demonetization process which took place during that period. Figure 2: Evolution of money supply and CPI

700.00 600.00 500.00 400.00 300.00 200.00 100.00 0.00 ipc M2 Source: Author plotting (data see appendix 2) On the right hand the evolution in year and on the left hand the increase of money supply. From 1995 the money supply was tie to economic activities and as the money supply increased, the inflation follow the speed of money supply until 2001 but after this period the CPI slope (red on up) become more positive compare to slope of money supply this mean that there other factor which come into force to explain the increase of price level among those for example is the decrease of national output and lack of food in many area such as Bugesera, and others. The close correspondence between domestic and foreign inflation points to the importance of foreign factors (the role of import arrangement) in underpinning Rwanda major inflationary episodes.

y and a variety of theoretical models give the result that for a small country; foreign inflation will be fully imported in the long run under a regime of fixed exchange rate. In effect, a small country with a fixed exchange rate has very little choice but to accommodate foreign shocks to price. Although since the Central bank hasn't this regime in Rwanda its use a range of tools which may ameliorate the effects of foreign price shocks the picture in Rwanda as in most other developing countries with similar institutions structures is of the shocks originating in the balance of payments and impacting through the exchange mechanism. With well over half of Rwanda goods and services imported there remains a close correspondence between foreign and domestic prices (see Figure 3). Figure 3: Evolution of import prices and domestic prices

T o some in thousand 4000000 2500000 2000000 3500000 3000000 1500000 1000000 500000 1995-1 1996-1 1997-1 1998-1 1999-1 2000-1 2001-1 2002-1 2003-1 2004-1 2005-1 2006-1 2007-1 2008-1 2009-1 0 I lower the import price IPC period in years port price price. Since 1995 until 1996 the quantity imported was very high and import price also was very big but at the same time the domestic price was not very high because at this period the most commodities imported was not for consumption. There were dominated by services and low materials to build and medical stuffs. After the 1998 the situation change first of all by lack of food because there was insecurity in whole country this impel people to cultivate and making there daily activities the high level of price was due of food products. Since the 2002 the speed in import price was is

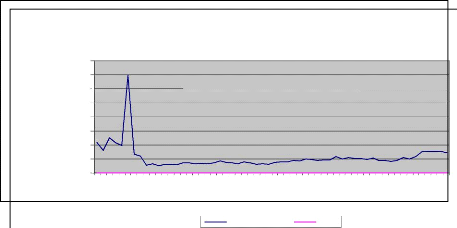

e level on domestic market. 2.1.2 Domestic factors Its have been seen foreign factors have played a dominant role, domestic factors also appear to have underpinned inflation over much of the period and have been particularly important during the keys period. The nominal wage grew at an average annual rate of over six percent over the past fifteen years while productivity grew on average of two percent. The result was sustained growth in nominal unit labor cost which effectively put a floor under domestic inflation( see Figure4) sharp increase in real wages particularly during the 2006 appear to have intensified price pressure at the time. Figure4: Evolution of nominal wage and CPI UUC 96 98 00 02 04 06 08

.018 .016 .014 .012 .010 .008 .006 2.0 0.8 0.6 1.8 1.6 1.4 1.2 1.0 96 98 00 02 04 06 08 IPC Source: Author plotting (data appendix1) One the right hand is the evolution in year and left hand the rate of change in nominal wage and the consumer price index for domestic goods. While broad movements in prices appear to have been largely caused by import prices and domestic labour costs, there also appears to have been a correlation with the cyclical pattern of output. Domestic business cycle fluctuations often reflect a misalignment of demand and the productive capacity of the economy. Excess demand is likely to generate price pressures in factor and product markets (see Figure 5)

nflation IIC 2.0 1.8 1.6 1.4 1.2 1.0 0.8 0.6 96 98 00 02 04 06 08 IIBC

Source: Author plotting (data appendix1) 1 The figure above show the correlation between the increase in out put on the right hand the two year evolution and the left hand the rate of price level increased the expectation here is that the increase of price was not due to increase of output but the output seems to be positive by the way the level of domestic demand was not compensated by domestic production this explain the need of import which was observed above. Macroeconomic theory suggests different way to explain the problem of inflation. The basic concept to be considered is the models suggested by Brouwer and Neil R.Ericsson which reconciles the effects of «demand-pull» and «cost -push» inflation theory. |

| |||||||||||||||||