A Critical Analysis of Effectiveness of Tax Offences Control Mechanisms Under Rwandan Law( Télécharger le fichier original )par Charles KABERA Kigali Independent University - LLB 2008 |

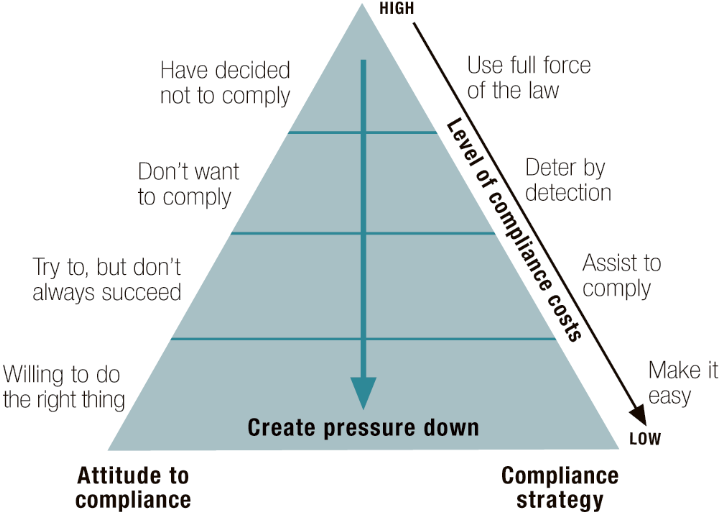

III.1.4 Application of adequate penalties66(*)Penalties for non-compliance are an essential element of a robust tax system67(*). The tax system can be expected to function smoothly and yield anticipated revenues only if adequate penalties are imposed for violations that strike at the heart of the tax system, such as failure to file returns and to pay on time. It is important that the interest provisions for late tax payment compensate the government for the time that the taxpayer has use of the government's revenue. The total interest cost for late tax payment should exceed the interest rate for borrowing money...it should be less costly for the taxpayer to borrow to pay taxes rather than to delay paying taxes as a way to obtain cheap financing from the government. In addition, if registration and other requirements critical for a smooth functioning tax system are adopted, adequate penalties should be applied for violation of these requirements as well. Probably the most traditional measure that has been used by the tax administration to deal with tax offenders is the application of fines or penalties, both administrative and criminal. For example, interest can be charged on tax owed; penalties can be levied for providing incorrect/false information; penalties can be imposed if an employer fails to withhold tax; and fines can be issued for late lodgement or non-lodgement. Penalties can also be issued on advisors. The idea is that the imposition of heavy penalties, coupled with the increased risk of detection and strong enforcement, reduces Tax offences. The general view is that for penalties to act as effective deterrents, they need to be compelling and applied consistently and quickly. At the same time, the penalty structure also needs to be realistic so that administrators are not actually reluctant to use them. For example, if the penalties are so severe and inflexible, they are hardly ever used! The clarity and fairness of penalty structures is also important. If a taxpayers make an honest mistake in their tax returns or if they could not pay their tax on time due to severe personal circumstances, there should be flexibility in the penalty structures to allow the tax administration to take these issues into account and either waiver the penalty and/or work with the taxpayer to arrange for ways the tax debt can be repaid. In both these circumstances, an inflexible penalty structure may have the effect of alienating the taxpayer and encouraging them to disappear altogether from the tax net, resulting in revenues that will never be recovered. The structure, severity and coverage, of penalties should increase with: (1) the potential revenue loss due to the tax offence; (2) the difficulty and cost of detecting the offence; (3) the effect of the offence on other taxpayers; (4) the offender's state of mind-a higher penalty should apply if the offence is deliberate and pre-planned; and (5) recidivism. Penalties for non-compliance should be inversely related to the ease of compliance. Best practice for promoting compliance Model68(*) Different attitudes to paying tax may require different responses to collecting tax. The tax administration should use this model to show how it meets different attitudes with different responses designed to encourage and support tax compliance. The model represents best practice in this area internationally.

The aim for this model is to move people who are not complying into a position where they are. The points discussed here are intended to help ease the transition to compliance for those willing to change. For those not willing to change, the full force of the law should then be applied, with the hardcore of offenders attracting the severest penalties. * 66 The Reform of Tax Administration, Vito Tanzi and Anthony Pellechio, IMF, Feb 1995 P. 13 * 67 Tax Compliance: Report to the Treasurer and the Minister of Revenue by Committee of Experts on Tax Compliance, December, 1998 * 68 Source: The way forward - achievements and future direction, Inland Revenue Department, August 2003 |

|