|

MASTER'S THESIS

ERP System: Implementation, Audit and

Control Risks

Supervisor:

Professor Jean Charles

Clément

Prepared by:

Borhen Habib Khatib

2009-2010

INSEEC

MSc Program in Audit and Control Management

Abstract:

Organizations implement Enterprise Resource Planning (ERP)

Systems in order to address the problems pose by disparate applications within

functional areas and to achieve competitive advantages. ERP systems typically

provide elegant technological solutions for organizations information needs

through radical changes in information processing orientation. Due to the

robust nature of these applications and the changes associated with the

implementation, auditors may need to adjust the audit processes and procedures

when auditing in such an environment.

The aim of this study is to present phases of an ERP systems

implementation and its impact on audit process in an organization. The focus is

to identify different phases of the implementation and how auditor can manage

this change. The research is conducted during my training on AS-Solar France

and the samples consist in the implementation of different module in CEGID ERP

System.

Table of contents

1. Introduction

...............................................................................................................

6

2. ERP System

.................................................................................................................

8

2.1. What is an ERP System?

2.2. ERP System Integration

3. Implementation of ERP System 10

3.1. The architecture of ERP project

3.1.1. Change management

3.1.2. Technical structure

3.2. ERP implementation phases

............................................................... ......11

3.2.1. Launch phase 11

3.2.1.1. Build the project and release the means

3.2.1.2. Confirm the objectives and identify the open

questions

3.2.1.3. Initiate information systems mapping

3.2.2. Design phase

..............................................................................

14

3.2.2.1. Validate options and close open questions

3.2.2.2. Define scope and structures

3.2.2.3. Identify and address specific risks

3.2.2.4. Define strategy and technical means

3.2.3. Implementation of the solution

............................... 18

3.2.3.1. Coordinate sub-projects

3.2.3.2. Organize the deployment

3.2.3.2.1. A deployment plan

3.2.3.2.2. Deployment teams organization

3.2.3.2.3. Training

3.2.3.2.4. Anticipate actions

3.2.3.3. Upgrading existing repositories

3.2.4. Integration phase 20

3.2.4.1. Prepare toggle plan

3.2.4.2. Validate integration

3.2.5. Production phase 23

3.2.5.1. Prepare the structure

3.2.5.2. Simulate actual operation

4. ERP System: Audit and Control of Risks 24

4.1. Reasons for implementation of Audit and control ERP System

24

4.1.1. High risks

................................................................................................

24

4.1.2. Higher Levels of Regulation 24

4.1.3. Efforts to meet new regulatory requirements .......

26

4.1.3.1. Visibility

4.1.3.2. Control

4.1.3.3. Efficiency

4.1.4. Common mistakes

.................................................................................

29

4.1.4.1. Poor planning

4.1.4.2. Lack of focus

4.1.4.3. Auditors skills

4.1.4.4. Reliance on technology

4.2. What should be reviewed? 31

4.2.1. Hardware

4.2.2. Network

4.2.3. Software

4.2.4. Processes

4.2.5. users work

4.3. Required Action

5. ERP CEGID Implementation: Case AS-SOLAR FRANCE ..............

36

5.1. Introduction

5.1.1. AS-Solar, CEGID and evolution of the implementation 36

5.1.1.1. About CEGID ERP System

5.1.1.2. AS-Solar, evolution of the ERP implementation

5.2. Review management process 40

5.2.1. Audit

services

5.2.2. Audit Purchases Department

5.2.3. Audit Sales department

5.2.4. Recommendations

5.3. Implementation phases 44

5.3.1. launch phase 44

5.3.2. Design

phase...........................................................................................

44

5.3.3. Implementation of the solution

............................... 45

5.3.3.1. Coordinate sub-projects by service

5.3.3.2. Integration of two new module

5.3.4. Management process of the company after implementation

5.4. Test and control 47

Conclusion..............................................................................................................................

48

Reference..................................................................................................................................50

1. Introduction

ERP systems facilitate horizontal and vertical integration of

business processes across an organization via a synchronized suite of software

applications. ERP systems successfully implemented, can enable companies to

better manage supply chains, perform business reengineering and reorganize

their accounting processes along with different other functions. In addition,

observed that ERP systems are currently becoming a necessary tool for companies

to remain competitive in this new business environment rather than constituting

a new strategic move.

However, ERP systems are usually accompanied with changes in

business processes in companies. ERP systems bring about changes in internal

control, business process, and segregation of duties. Typically, organizations

may need to reengineer business processes and make essential changes for

successful implementation of ERP systems. Such changes brought about by ERP

systems affect the ways auditors perform their duties.

It is important to understand how this ERP environment is

affecting auditors work and responsibility. What makes this topic interesting

is because several researchers are quick to point out the need for auditors to

adapt to changes brought about with ERP evolution, yet understanding how these

changes affect auditors have not been adequately investigated.

Structure of the Study

This study is divided into five chapters. The first chapter

covers the introduction and structure of the study.

Chapter two, will review briefly enterprises resource planning

(ERP) systems. This will help to present a clear understanding of ERP System

Implementation.

Chapter three discusses enterprises resource planning (ERP)

systems, their technical characteristics and their architecture. It will

present a detailed understanding of ERP systems and phases of

implementation.

Chapter four will review briefly auditing and audit process.

This will help to present a clear understanding of audit approach and steps

performed by auditors in audit engagements.

Chapter five introduces the empirical part of this study.

Implementation of the ERP CEGID System with AS-Solar France team and present

how audit can effect implementation phases.

2. ERP System Implementation 2.1. What is an ERP

System?

ERP means "enterprise resource planning" and it is a computer

application. That enables the company to manage and optimize all of its

resources.

ERP provides availability of different modules that cover all

business needs such as undertaking, since commercial production, logistics,

finance, human resources, customer service, (all fields are present at an equal

level completeness). ERP System dependents on the different process and on the

different areas caused by the use of a common database.

ERP system provides the company with the enables to manage and

control several sites, languages and currencies simultaneously. Therefore, the

ERP system is fully recognized and used at international level.

Organizational and functional integration was built around the

knowledge of different management processes and interaction between different

services. The complexity of this integration is growing fast with the number of

areas covered and with the number of users, which itself is a technology that

is a set of techniques, expertise and practices.

- ERP technology

As the applications share the same information, the system must

be developed with

rules built inside the database. The development of the

screens and reports can be

minimized since each application does not require

duplication of share data update

capabilities. For instance, defining departments can be done in

one site and shared by all applications.

- Know-how and best practices

ERP systems require a big more effort in terms of planning and

resources implementation than stand-alone applications. Integration means that

all functional areas and business process's have to be considered prior to any

decision.

3. Implementation of ERP System

3.1. The architecture of the ERP project

The architecture of an ERP project consists in defining its

division into subprojects. The division into sub-projects is a breakdown into

different types of activity. Subprojects allow the implementation of the global

project, but each of them requires, for its realization, different techniques

involving specific skills. Project success depends on a good timing and

coordination between subprojects, which are the responsibility of the project

management.

Figure 1. Architecture of an ERP Project

3.1.1. Change management

The role of this subproject is related mainly to users

training, data preparation as well as to organizational change. This subproject

must be conducted in parallel with the implementation of the ERP and it is

essential for the transition phase.

Change management is conducted by operational users and

accompanied by external consultants.

3.1.2. Technical structure

This subproject reviews:

- The technical infrastructure needed to run the software.

Infrastructure refers to servers, networks, workstations that give users an

access to the ERP. This infrastructure consists in hardware but also in

software (operating system, database system, utilities). It will be necessary

first for the team project and then for the production phase.

- The operating environment of the ERP itself and all the

components that are necessary for the implementation: interfaces, conversions

and database.

- All the adjustments to the standard product that the company

decides to implement. The activities will be related to their definition,

design, implementation, testing and documentation

These adaptations depend on the specific functions that the

company decides to maintain and which are not provided by the ERP. This means

modifications or creation of states or screens with or without modifications on

the standard chaining screens.

3.2. ERP System implementation phases

These phases make the project progress by providing visible

landmarks and give a general layout of the project.

3.2.1. launch phase

Anticipating all necessary resources for an immediate

departure of the project is the key of success in this phase. This phase

requires a strong involvement of senior managers and economic objectives must

be known and shared.

The failure factors are due to a too fast start of the project

caused by a long decisional cycle and the consultants desire to gain the lost

time.

Key activities are:

3.2.1.1. Build the project and release means

This will require mobilizing the project team which is a

difficult step because after identifying the potential partners we must,

negotiate with those concerned their participation in the project, and convince

their superiors.

In this step difficulty is that for many operational users, it is

not obvious to leave their own structure and join the project team for one to

two years.

3.2.1.2. Confirm the objectives and identify the open

questions

Formalization of objectives and definition of exact needs are

the challenge for the project team. Indeed they can make concrete and visible

the project's contribution to the company goals by allowing needed

resources.

The objectives are first expressed in general terms and therefore

must be listed by the project management in more details:

- Organizational scope, which specifies the entities involved:

Business units,

services, profiles and number of users.

- Functional scope, which identifies functions / processes used

by prospective users and the modules and sub modules in the ERP.

- Integration scope, which details other applications with which

ERP data exchange.

By performing this exercise, we will detect "open questions" that

should be clarified during the design phase.

Key questions that a business should ask are: Who will lead our

implementation effort?

- Do we have the in house resources, skills and experience to

implement ERP?

- Should we build effective strategic partnerships?

- Have we considered how the implementation will differentiate

our business?

- Have we developed a business case for the ERP implementation

project?

- Do the features and functions meet our needs?

- Is the ERP package compatible with our business?

- Should we buy an integrated package from a single vendor or

best-of-breed

solutions from several vendors?

- How do we get started with the implementation?

- What steps do we take to ensure that the implementation is on

track? - How do we ensure that our people are accepting change?

- How do we integrate the ERP with our other legacy systems?

The Project team has to detect those under the responsibility of

the direction team.

Open questions will be resolved during the next phase.

However, if the questions are important, it will be advisable, before starting

the design phase, to take time and clarify the key points by a pre-focused

study.

3.2.1.3. Initiate information systems mapping

During this phase, the concern is to establish, or at least to

initiate the establishment of a mapping.

Mapping is related to existing applications, interfaces,

platforms and technologies that support the information flows around the

databases and allows in the next phase project team to assess the functional

context of integration between the ERP and other applications.

This will be made with computer services technical study, and

using functional to clarify the functions which are handled by existing

applications.

3.2.2. Design phase

The factors of success in this phase are related to the

clarification of structuring points. The purpose is to have a defined objects

solution.

However the failure factors are the difficulty in finding

«the right level of details» and miss some essential points.

3.2.2.1. Validate options and close open questions

As we saw during the previous phase in which we have

identified questions, also the work of the design phase will generate new

"opened points". The responses of all opened points will be mad during this

phase. This will be the role of project manager.

The decisional process will be related to:

· Operational modes and target organization. Identify

the differences or the similarities between existing organizational and change

needed to prepare new areas.

· The character of data bases and their administration.

This is typically the level of harmonization and centralization between

bases.

· Specific needs, the decisions on this point are either

accepts the cost of specific development and maintenance or to match

capabilities.

· Integration mode of the ERP, either to accept a

challenge and reduce functional scope or to agree with an important cost of

development and maintenance interfaces.

All Decisions are mainly produced by the ERP team project

which identify outstanding issues and take decisions. The project manager

should be reactive and must be able to responds to unsolved points.

After solving different questions, team project resume

decision and outstanding issues for the area studied. With this summary, they

can react immediately on such of opened points and ensuring integration between

the different areas.

This approach ensures the end of design decisions and start to

structure their solutions, which are identified, quantified and validated by

the steering bodies.

3.2.2.2. Define scope and structures

This is the main activity of ERP subproject. All

preoccupations are around the definition of an organizational structure, study

adequacy and integration between the ERP System and other applications.

For each domain / sub domain / process we will identify:

· Operating modes, which are defined by procedures

· Organizational structures; is the organization of work

(who does what) and circulation of information.

· Characteristics of repositories.

This classification will be done during workshop by the team

project.

The starting point is always running after a proposal from the

repository of the ERP. After that participants can identify differences with

their organizations.

The implementation of a functional scope guide allowed need two

aspects:

- Complexity of interfaces between the ERP System and other

information systems

- Impacts on integrate software package itself

3.2.2.3. Identify and address specific risk

It is important at this stage to identify specific functional

mode of the company. These characteristics could lead to a gap in coverage

between needs and capabilities of the ERP.

This identification is done during the study of adequacy

between desired functional modes and possibilities of the ERP System. It

focuses on a solution by seeking changes in the organization and removes

discrepancy without specific development and without compromising the original

goal.

? Avoid the specific development is the goal number one when

we chose a package solution.

These extensions should always be carefully validated, because

it reflects the choice of the company and extend existing operating capacity to

evaluate and stay in the standard options of the product.

3.2.2.4. Defining strategy and technical means

Technical project's still a poor factor in the implementation

of an ERP project. The importance of its components, architecture and other

operational management isn't perceived with sufficient acuity by the

manager.

The various levels that will guide the ERP project are:

- Implementation of technical infrastructure and procedures

support needs of project phase and prepare production environment. This step is

done during the design phase and project execution.

- Scalability of continuous services, which support change under

real conditions. This step occurs during the integration phase and into

production.

- Service continuous, provide needs and carry out any transfer of

competence in the internal teams.

Non-technical context or improperly mastered causes:

- Loss productivity of the project team and a lot of

nervousness. This may represent about 20% of potential team product and

therefore huge sums relative to cost techniques themselves.

- Dissatisfaction or even a rejection of the new information

system by users.

3.2.3. Implementation of the solution

The factor of success on this phase is to avoid external

disturbances. But factor of failure is the modest involvement of user's

resources on integration process.

Key activities are:

3.2.3.1. Coordinate sub-projects

During this phase ERP sub-projects; expansion and integration are

closely linked and must master the synergy between them.

The master of sub-project clarify during this phase management

rules; establish setting sheets, detailed specifications of programs interface

and extensions. It is from this point that the training of implementation is

elaborated. It is built around configuration, specific programs and interfaces.

The master of interactions requires above all a good balance communication

between functional and technical teams.

3.2.3.2. Organize the deployment

When deployment is expected we must build, establish strategy and

launch anticipatory action.

3.2.3.2.1. A deployment plan

The deployment steps should identify organizational various

entities that is deployed from the driver. The sequence should include:

o Functional constraints (such area must be installed before

another, two areas of different entities have to go into production at the same

time)

o Integration constraints (reuse of existing interfaces, don't

develop temporary

interfaces)

o Constraints of project objectives (project benefits may be more

urgent at any given location).

Functional and technical constraints are identified; we try to

go as soon as possible by establishing multiple deployments and allocate means

to ensure monitoring and supervision of the project.

3.2.3.2.2. Deployment teams organization

A team should be identified for each deployed unit. This team

is deployed to the entity for which installation of the ERP is a mini-project.

Skills of this local team are reinforced by a specific expertise from initial

project team or experts who have been specially trained for this purpose.

The identification of the local team will need at first to

choose a project manager and representatives of users on functional area.

User's choice depends on the complexity of key functional areas and on the

profile of user's representatives.

3.2.3.2.3. Training

Implementations of the various entities engage team manager to

prepare a shared guidance for local project team and especially for users.

3.2.3.2.4. Anticipate Actions

After solving opened questions during previous phases, several

actions can be launched from the middle of this phase to prepare the

deployment;

.. Inventory of local technical infrastructure; .. Identification

of local and central resources .. Identification of training means

3.2.3.3. Upgrading existing repositories

This subject is often critical in the middle of the

implementation phase when it wasn't allowed. Indeed at this stage project team

addressed a new framework, specifications of recovery programs and take actions

to upgrade existing files.

Harmonization of files is primarily the harmonization of

different codifications, cleansing data and their impacts in terms of

particular statistical treatment.

3.2.4. Integration phase

In this phase the key for success is monitoring carefully

coherence between ERP System interfaces and external systems.

Key activities:

3.2.4.1. Prepare toggle plan

During this step, project team, list all steps which conduct

changes between old and new systems.

These steps include rocking action preparation and it may start

several months earlier. Actions are relating to:

- Clean up data such as customer-supplier, articles, charts of

accounts, additional manuals before restart and additional manual after

recovery.

- Correlation tables used by conversion program

- Production environments which are performed by the new system.

Upgrade library of references, tables or specific data.

- Control static balance between old and new systems

- After data migration controls are necessary to validate

information related to current inventory, customer, supplier, balance and

production orders.

For all of these spots a schedule of responsibilities and roles

must be established.

To create this plan; team project need to use information from

testing data and from integration phase.

3.2.4.2. Validate integration

This step is essential; it is a part of testing process that

has been made in previous phases. At this stage it becomes possible to validate

integration as various components are completed.

- Contribution:

- This validation don't focus on setting up the ERP, but they

focus on the ERP

specific programs and interface between different programs, so

it's a validation of all components to the new information systems.

- Integrator execute much strong test sets on the real data, and

relevance of tests are encountered in reality.

- Tests must be done mainly by users and not only by

representatives of users as

it could be done in the previous phase.

It takes place in a real environment to test prototype and

functional tools. It is faced to the interaction between correcting and

testing.

In validation process this step is a key for functional and

technical success. Indeed,

behind project team, technical resources bring

position to exploit different interface.

Which allow them to review their operating procedures and

validate different aspects of technical performance.

- Honing means operating in real conditions.

This step allows execution to check with a final operating

platform and run in the landscape management system. This point is related to

transfers management between different development environments.

During this phase of integration that is revealed the risk of

technical structure. Indeed tests performed in a configuration close to the

operational reality. So this phase proved the performance often associated with

necessary adjustments between ERP and database manager used.

3.2.5. Production phase

The factor of success in this phase is to put in a real

situation; functional, technical and organizational measures to minimize

discoveries during production transition.

Key activities:

3.2.5.1. Prepare the structure

This phase is launched with the training of users. It includes a

theoretical and a practical part.

During the first months after the switch it is often desired

to implement local support. It is like a filter between user and help desk to

resolve problems that needs additional training.

3.2.5.2. Simulate actual operation These operations

simulate the final production scale.

It will therefore test the switch plan, based on real data,

get in position to do work expected daily, weekly, monthly. This simulation is

done by the most advanced resource projects (functional representatives and

consultant).

Beyond the switch test, this step allows to improve tools and

methods for controlling additional data.

4. ERP System Audit and Control Risks

4.1. Reasons for an ERP System Audit

ERP audits and reviews can be justified by outlining the

wide-ranging consequences of undertaking an ERP implementation. If implementing

a system can impact a company in a multitude of ways then there will be a need

to monitor and control such an implementation as well as ensure its continued

success. Implementing an ERP system will significantly increase risks which in

turn will require the establishment of mitigating controls and a mechanism for

monitoring such controls.

4.1.1. Increased Risk

Enterprise Resource planning systems use data from a wide

range of business areas to provide cross-departmental management and process

information. Such systems manage the core critical business processes of an

organization. Implementations can fail to deliver expected results if not

adequately managed and controlled. Furthermore, there are emerging trends and

changing technologies that support expanded use of ERP systems (such as,

web-enabled customer interfaces), which will increase the importance of the

security and control consideration for ERP. Hence, an ERP implementation will

have wide ranging impacts on the technology, people and processes of an

organization and its trading partners.

4.1.2. Higher Levels of Regulation

Perhaps the greatest justification for an ERP audit at this

point in time is the increasing

levels of regulation being imposed on

organizations. In the wake of corporate financial

scandals, governments and

regulatory agencies are responding to failing investor

confidence by implementing new regulations. In the United

States for instance, stricter reporting rules, such as those defined in the

Sarbanes-Oxley Act of 2002, require company executives to certify the accuracy

and legitimacy of corporate financial statements or face the possibility of

punitive and criminal action. European Union members are mandated to report

financial results as per the International Accounting Standard (IAS) by 1

January 2005. At that time, they also have to restate 2003 and 2004 results,

per the IAS. Further, IAS is going global. In addition to the EU, Hong Kong,

Korea, Singapore, Australia, Canada, and most recently, Russia have announced

either their support for, or adoption of the IAS. The U.S. Financial Accounting

Standards Board is conducting discussions with the IAS board on the

reconciliation of differences between the two standards. Multinational

corporations may have the added burden of complying simultaneously with the

Sarbanes-Oxley Act and the IAS, as well as a host of local regulations in the

countries in which they operate.

4.1.3. Efforts to meet new regulatory requirements

|

Compliance Challenge

|

Strategy

|

Enabler

|

|

CEOs and CFOs must personally certify Financial reports

|

Provide complete and accurate information with confidence

- Access information in real-time to proactively address issues

that may arise

|

Visibility

-Setup transparent integrated

processes across the enterprise -Enable executives to access

relevant and timely information

|

|

Disclosure of internal controls and processes for Financial

Reporting; Auditors must verify Adequacy

|

Setup better controls that work

and enable regulatory

compliance

Make audits easy, fast, and effective

|

Control

- Establish centralised internal audit processes and controls

across the enterprise that are documented, secure, and easily accessible

- Train employees and monitor skills to maximize compliance with

policies

and procedures

|

|

Aggressive deadlines for Financial reporting

|

Close books quicker

|

Efficiency

- Roll up and reconcile financial data quickly and accurately

- Implement centralised, low cost, error-reducing processes as

a

backbone to ensuring consistent, error-free data across the

enterprise

|

4.1.3.1. Visibility

Enterprise visibility is imperative to give you immediate

access to high-quality business information. In most companies, the best

information executives have about the state of their business comes from the

close of the preceding quarter. However, without access to the current state of

your business, you risk making decisions that solve yesterday's problems, not

today's. To exercise good governance and meet regulatory demands, you need

access to timely, relevant, and accurate information across your organization.

Only a business system with a complete set of integrated business intelligence

and analytics can provide managers with continuous, current, customised

information about their business which can enable them to:

- Access a complete and accurate view of financial data for

quicker reporting and meaningful disclosure.

- View global enterprise information that is timely, relevant,

consistent, and available in realtime. Obtain a complete view of your business

with global information from a single source of truth.

4.1.3.2. Control

Enterprise control is necessary to accurately provide

information based on standardised processes and procedures. With effective

control, you can avoid careless accounting actices, enable compliance through

documented business practices and procedures, implement your vision and

business strategies, and find and fix discrepancies proactively. To control

your enterprise more effectively, you need to centralise and secure policies,

processes, and procedures across your organisation. Business systems can help

you streamline the transparency of policies and procedures,

enforce them, reduce the risk of malfeasance and errors, and

improve confidence in your business data:

Support the audit department in enforcing corporate compliance

with documented policies and procedures, risk and process control management,

visibility to business process workflow, and improved project management.

Keep your employees informed - document and track critical

business processes, determine workflow, and develop and deploy applicable

training to ensure compliance. Manage and document corporate communications and

data with an integrated suite of enterprise level applications that focus on

managing all of the communications between individuals and teams, the content

they create, as well as the information for supporting them.

Centralise and automate processes and controls for information

consistency. Eliminate duplicate processes, reduce overhead, and cut costs.

4.1.3.3. Efficiency

To meet the reporting deadlines imposed by new legislation,

your organisation must operate at maximum efficiency. By removing the

complexity from your business applications you can confidently face new

governance demands. A truly efficient business system operates on a single data

model with data consolidated in one location. Integrated applications and

automated business flows quickly moves business data among global front and

back office operations. Data can be rolled up and reconciled accurately and

business processes run smoothly and quickly - %o

Eliminate bottlenecks and streamline the rollout of new internal

processes and procedures with self-service.

- Reduce the risk of malfeasance and accidental errors by

streamlining inter-user approvals and participation in review processes.

- Enable efficient execution of internal audits by providing

project team members complete visibility into audit data.

- Integrate enterprise data and business processes based on a

unified data

model to support global compliance.

4.1.4. Common mistakes 4.1.4.1. Poor planning

In many instances there is no concerted effort to ensure that

audit and review processes are embedded in the project life cycle. It is

essential during the initial planning of a project to ascertain who will be

performing audit and review activities as well as the duration and frequency of

such activities. At the outset of a project it is important that all parties

involved understand the scope of the activities to be performed.

4.1.4.2. Lack of focus

Even when audits and reviews are undertaken they often fail to

focus on the areas of an implementation that pose the greatest threat to

implementation success or organisational control. This to a large extent

relates to the previously mentioned point of planning. Implementation planners

should identify potential problem areas and

then determine how to adjust their audit and review approach to

deal with these concerns.

4.1.4.3. Competency of Auditors

In many instances the parties made responsible for audit and

review do not know the workings of ERP systems. They are often not aware of the

workings of the particular system they are auditing. In many instances the

financial auditors audit around the system using the «black box»

approach i.e. they rely on inputs and outputs and don't look at what happens in

between the ERP auditors must have at least a high level knowledge of how such

systems work and how the modules relate to each other. Certainly, they should

know the key features of the particular software they are working with and

ensure they ascertain whether the package has any problem areas. Being able to

query and pull out reports from the system is the ideal situation. This would

necessitate persons responsible for audit and review being included in

implementation activities such as training and testing.

4.1.4.4. Reliance on technology for the solution

All too often people have a tendency to believe that by

implementing a highly functional system, controls will automatically be taken

care of as there is a high degree of sophistication embedded in these systems.

However, this is not the case and care should be taken to ensure that all

business processes are carefully documented and users clearly understand what

components of a process require manual or human intervention.

4.2. What should be reviewed?

In any systems implementation, it is not just about the

software. There are many other components that make up a successful

implementation and these will be identified. Each of these areas may

necessitate specialised audit, as they require a unique level of knowledge and

skills set. Although I have mentioned each of these components separately, it

is important to understand that they all interact with each other and are part

of an organisational system.

4.2.1. Hardware

Each software vendor will provide the business with certain

minimum specifications that they should follow when determining the hardware

requirements of clients and servers. These requirements should be strictly

adhered to. Often these specifications will be based on statistics that the

auditors have provided the vendor with regarding volumes of transactions that

are to be processed. Every effort should be made to ensure that these

statistics are correct as this may result in sizing problems. The organisation

should ensure that they size the hardware in such a manner that it provides for

growth.

4.2.2. Network

There's nothing worse than going live and finding that

inadequate network speed brings the system to a screeching halt. Efforts should

be made to ensure that network speeds are tested and that all persons involved

in system operation have access to the network. Control should also be

maintained over the network to prevent unauthorised users gaining access.

4.2.3. Software

Every organisation has various layers of software upon which

their ERP systems reside as well other systems, both internal and external,

with which they interact - see figure 2. Audits should be conducted of software

subsystems within the organisational system. The following are key areas that

should be examined:

- Standard ERP parameters, including application controls,

authorisations and standard security configuration.

- Application security - to ensure processing occurs in an

efficient and controlled

manner, while protecting valuable data.

- Configuration decisions - to help provide reasonable assurance

of the integrity of business processes and application security.

- Design documentation - to ensure appropriate security and

control.

- The security administration process - to provide reasonable

assurance that access granted is appropriately identified, evaluated and

approved.

Many business processes may be extended out over the intranet,

extranet or Internet. The auditor should provide reasonable assurance that

security processes appropriately address these risks.

4.2.4. Processes

An audit of an ERP should provide assurance on the integrity

of processes in use by the business. Specifically, the following tasks relating

to audit and review should be undertaken.

- Identify control objectives for processes being implemented.

- Identify and assess potential business risks and financial

risks in the processes

being implemented.

- Develop and design the most effective and efficient ways of

controlling these risks (which implementers generally do not focus on or do not

have the expertise to develop).

- Perform an independent analysis of key business activities,

comparing organisation processes to leading practices and recommending process

improvements.

- Provide assurance that the controls within ERP are appropriate

and effective.

- Review the interfaces feeding into ERP from non-ERP systems

(such as, including legacy, web-based and mobile computing applications).

- Perform audit tests focusing on business process and

internal control. Many organizations reengineer business processes during ERP

implementation. Review business continuity plans and provide reasonable

assurance that they have been tested.

4.2.5. Users work

All implementations require a successful combination of the

elements of people, process and technology. It is essential that an audit be

conducted of the staff involved in the implementation as well as the way in

which their roles are structured in relation to the ERP software

implemented.

In particular the following tasks should be undertaken:

- Identify staff, their responsibilities and skills sets.

- Assess training and knowledge transfer requirements.

- Ensure staff is adequately trained and test knowledge

transfer.

- Determine roles and responsibilities for staff by mapping

existing staff complement to processes in the ERP systems.

- Ensure that appropriate segregation of duties is maintained.

4.3. Required Action

Wherever risk is increased, management should institute controls

which mitigate the risks posed.

The objectives of such controls would be to:

1. Safeguard all the assets of the enterprise

2. Ensure accurate and reliable accounting (and other)

information

- Validity - only valid items are allowed to enter a system

(authorisation)

- Completeness - all valid items are captured and entered into

system (number of items)

- Input accuracy - data that is entered into the system is

correct (data fields)

3. Improve operational effectiveness, efficiency and security

- Effectiveness - fulfils intended objective.

- Efficiency - prevents unnecessary waste of resources.

- Security - protection of resources from misuse or

destruction.

4. Promote adherence to managerial policies

It is imperative that when such controls are established,

continuous audit and review work be undertaken in order to assess the

effectiveness of these controls. The audit of an ERP system requires specific

knowledge and an understanding of the complex features and integrated processes

built into and required for the successful implementation, use and control of

specific vendor products. As financials audits require specialised audit skills

so do ERP audits. Not only should the auditors have specialised skills but the

methodologies they use should also be uniquely tailored to deal with the

different risks involved. Audit and Review guidelines should be developed which

provide a management-oriented framework and proactive control self assessment

specifically focused on:

- Performance measurement--How well is the IT function supporting

business requirements?

- IT control profiling--What IT processes are important? What are

the critical success factors for control?

- Awareness--What are the risks of not achieving the

objectives?

- Benchmarking--What do others do? How can results be measured

and compared?

With respect to IT control profiling in point 2 above, I

believe organisations should reassess the controls in place using the maturity

framework outlined in figure 3 and the subsequent text. For each control the

required level of maturity should be determined and where the control is not

found to be at that level, corrective action should be taken.

5. ERP CEGID Implementation: Case AS-SOLAR FRANCE 5.1.

Introduction

AS Solar is an internationally active German specialized

distributor and project developer for solar technology. Along with different

subsidiaries in Spain/Portugal, Benelux, France, Italy and Romania/Hungary it

is present on the most important global markets in the field of photovoltaics.

As SOLAR connects lasting market quality and the technical know-how with

outstanding service to give customers an unparalleled advantage.

5.1.1. AS-Solar, CEGID and evolution of the

implementation 5.1.1.1. About CEGID ERP System

Cegid Business Management V8.10

Encompasses all business management Processes from procurement

to sales, ensuring the right products are in the right stores at the right

price and right time. In real time, the retailer needs to access data on key

indicators, including turnover and productivity. All in a multi-channel sales

environment: stores, website, mail order, wholesale.

· End-to-end merchandise management: retail

referencing, procurement, manufacturing, merchandise allocation, goods

receipts, pricing, promotions, inventory, restocking and replenishment, sales,

customer relations, sales events etc.

· Integrated decision-making tools for every step of the

way: standard and personalised dashboards, statistical analysis (stock turn,

best sellers, margin monitoring etc), alerts, reports, etc. allowing management

to make the right decisions at the right time

· Industry best practices and international expertise

· Data base management: products, prices, suppliers

etc

· Assortment and range planning

· Monitoring and management of purchasing and imports

· Inventory management, replenishment optimisation and

management of procurement cycles

· Price optimisation, sales and discounts

· Promotions, CRM, sales events and marketing

· Multi-channel management

· Management of international locations: own-label stores,

concessions, agents, franchises etc

5.1.1.2. AS-Solar, evolution of the ERP

implementation

AS-Solar France started the implementation of CEGID ERP on

2007 by integrating CEGID Business Management. This Module manage all the

important processes that increase operational performance: range planning,

pricing and promotions, replenishment optimization, loyalty and CRM.

But this first implementation failed for these different

reasons:

1. Governance

Lack of a single person in charge who reports directly to

openly supportive senior executive accountable for the solution. Also,

ineffective steering body of cross-functional senior executives.

2. Scope Failure to align contract for services

with the requirements expectations.

3. Change Management Insufficient investment in

all facets of change Management

4. Skills

Team members lack a thorough understanding of the technical

capabilities of the solution or of the underlying business processes

5. Decision Making

Relying too much on consensus-based decision making, rather than

rapid evaluation of options

6. Communications

Lacking at all levels (executives, functional owners, across

team, with working level system users, external stakeholders, etc.)

7. Solution Architecture Lack of a solution

architecture or proven implementation methodology

8. Training Insufficient investment at all

levels (including executives)

9. Culture

Trying to force an integrated, enterprise-wide solution into

a stove-piped culture. Systemic resistance to change trying to force an

integrated, enterprise-wide solution into a stove-piped culture. Systemic

resistance to change.

10. Leadership

Lack of «public» leadership from senior, accountable

executive and/or lack of continuity in this leadership position.

After two years of testing CEGID ERP System and insufficient

investment in the solution; senior executive decide to invest more time and

more resources on the different application of CEGID. They fixed new objects

related to use of all application and option of the solution, and integrate tow

new module Settlement Monitoring and CRM.

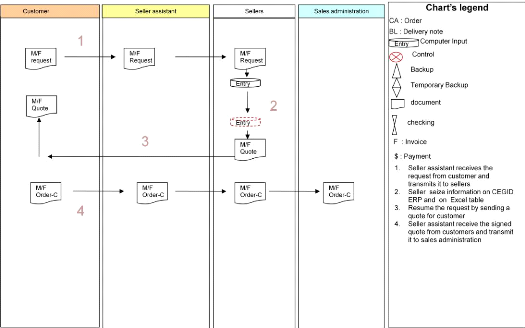

5.2. Review management process 5.2.1. Audit

services

|

Weaknesses

|

risks

|

· L1 Entering quotation on Excel and CEGID

|

Waste of time (double entry)

|

· L1 No verification and reconciliation between estimated

stock and available quantity for sale.

|

Customers not satisfied On-load of the work

|

· L1 Users don't use a dashboard to verify quantities in

stock before the generation

|

Loss of Margin

|

of the quote

|

Lost customers

|

· L1 There isn't sales manager who keeps

|

conflict between staff

|

track of customers

|

Lost customers

|

· L1 There is no control by a third person on charged

prices

|

|

· L1 Delivery date is not exhaustive

|

|

· L1 no follow-up margins by project

|

|

|

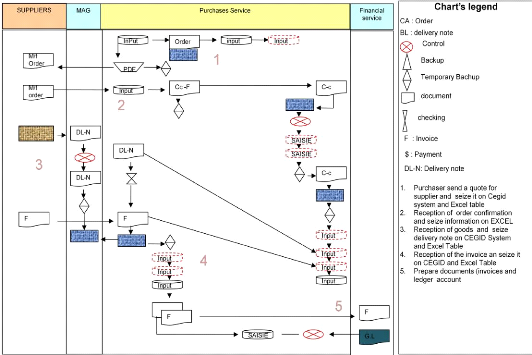

5.2.2. Audit Purchases Department

Weakness

|

Risks

|

|

' There is not a person who checks the ordered quantities

|

'

|

Lack or storage of stock

|

' There is not a third person providing stimulus and

|

'

|

|

followed orders

|

'

|

Input error

|

' Manage multiple tasks simultaneously with Excel Software

|

'

|

|

' Delivery note and order controlled by the same person

|

'

|

Waste of time

|

' Double data entry into Excel and CEGID

|

'

|

|

' Errors input between theoretical and physical input

|

'

|

Risk of theft

|

' No authorization for sending orders

|

|

|

|

5.2.3. Audit Sales department

Weakness

|

Risks

|

'LI There is no

third person who checks and monitors customers u pstream and

downstream.

|

Risk of error and omission Waste of time

|

'LI The lack of a manager who manage sales department and

ensure adequate segregation of

|

Difference between physical and

|

duties between staff

|

theoretical stock

|

'LI Difficulty to manage various tasks simultaneously

|

|

'LI No control over balances

|

|

'LI Removed from storage without Delivery note

|

|

'LI Lack of switchboard operator to manage calls

|

|

'LI Lack of clear and controlled procedures

to ensure the smooth operation between officers

|

|

'LI No restriction of access to corrections and changes

|

|

'LI Lack of control and weekly

reconciliation between CEGID and file management of warehouse

inventory

|

|

|

5.2.4. Recommendations

· L1 Remove tools provided by Excel

· L1 Set up and develop applications in CEGID ERP System

· L1 Establishment of clear procedures for each position

· L1 Assignment of responsibility for service with

well-defined objective

· L1 Limiting access to different module of CEGID as

required for each position

· L1 Impose control and completeness of data entered into

CEGID

· L1 Assigning a management

controller for the establishment and control procedures and

control margins

· L1 Separation of tasks and definition of jobs

· L1 The organization of the stock and imposition of a

monthly inventory with a screening of the causes of differences between actual

stock and theoretical stock

· L1 Appoint a director to monitor commercial customer

and prospect

· L1 Validation of purchase orders by the Financial

Officer

· L1 The introduction of visas that allow the control

and command generation

· L1 Configuration of the

tool to alleviate CEGID spots and avoid double entry in EXCEL

· L1 Development board tables to manage the project

margins

· L1 Manage clients and prospects to the aid of the CRM

module

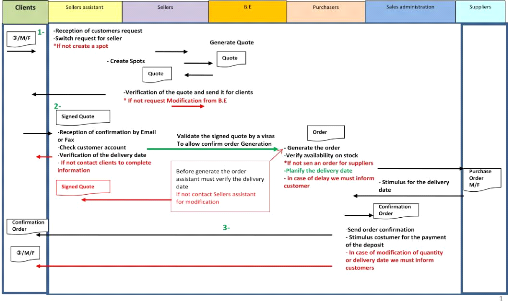

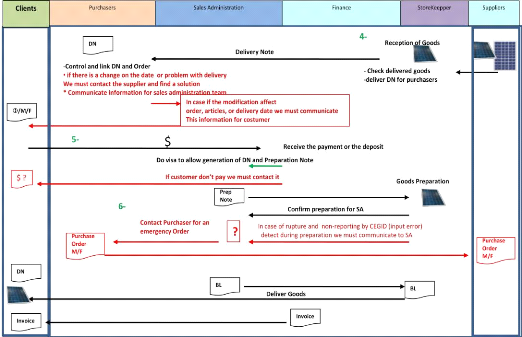

5.3. Implementation phases 5.3.1. launch phase

After auditing all service and identify weaknesses, we start

our planning by the establishment of clear procedures for each position and we

study this fundamental points:

- Who do what?

- Define roles and responsibilities

- Limit access and develop restriction - Drafted requirements

- Analyze working procedures

? By performing this exercise, we detect "open questions" that

should be clarified with the integrator.

5.3.2. Design phase

Clarifications of structuring points and we establish a plan to

define objective solution.

All Decisions are produced with the integrator of CEGID System

which identifies outstanding issues and review specific functional mode of the

company.

We focus on a solution by seeking changes in the organization

and removing discrepancy without specific development and without compromising

the original goal.

? The integrator analyze our draft requirements and give us

integration solution without a specific development

5.3.3. Implementation of the solution

5.3.3.1. Coordinate sub-projects by service

· Commercial service

On this department we set up and develop applications in

CEGID ERP System and simplify use of all application by creating a new

procedures and defining new rules. The objects on this sub-project and for this

department we avoided Excel Table and we get all information in one

database.

Create a dashboard to manage efficiently the stock

· Purchases Service

Set up and develop applications in CEGID ERP System to manage

Stock, and manage requested quantity.

We develop a clear procedure and simplify the use of the

application. All information saved in one date base, the CEGID System. And

purchaser can't generate an order without the authorization of the

accountant.

We develop a dashboard to manage quantity on stock and avoid

errors between theoretical and physical input

· Sales Administration

For this department we focus our improvement on developing

dashboards to manage delivery date for customers. Then, simplify application

concerning request payment of the deposit.

· Create new procedures toward save time and be more

productive.

? All procedures, applications and interfaces that we

developed on these different services are designed to simplify user entry and

manage more effectively their time.

5.3.3.2. Integration of two new module

. CRM Module

· The CRM module gives us a better insight into customers

and fosters a personalized approach for cultivating high value

relationships.

. Settlement Monitoring

· Allow us to be more effective on managing cash receipts

and disbursements.

· Develop new tools for fast debt collection.

· Schedule of payment tracks overall change in the cash and

we are more reactive to find solution

· After the due date of payment CEGID create an automatic

debt recovery letter. 5.3.4. Test and control

The end of implementation process was the test of all tools,

applications and interfaces by users.

This step is the most important because we test system on a real

condition.

5.4. Management process of AS-Solar company after ERP

implementation

Conclusion

The purpose of this study was to identify the phases and audits

related to the implementation of ERP systems in organizations.

An ERP implementation project is different from other systems

development projects. During the implementation of this project significant

risk factors was identified which include technological change, organizational

change and project complexity. These factors are the hallmarks of most (if not

all) ERP implementations.

Consequently, it is important to understand how these risk

factors can be mitigated. In this study, audits and management required to

minimize risks that organizations must control in an ERP system implementation

were identified.

Reference:

· Fred Kaplan (2007)/Best practices for an effective

ERP implementation / w w w . r e l e v a n t e . c o m

· Guy P. Lander(2004)/ What is Sarbanes-Oxley? Vol

0-07-143796-7 the mcGrawHill companies

· Henning Kagermann, William Kinney, Karlheinz Küting

; In cooperation with : Corinna Boecker, Julia Busch, Oliver Bussieck /

Internal audit handbook : management with SAP -audit roadmap /

· Jean-Luc Deixonne /Piloter un projet ERP :

transformer et dynamiser l'entreprise par un système d'information

intégré et orienté métier / Edition DUNOD

· Jennifer Hahn, Michael Juergens, Deloitte & Touche /

SAP: Business Process Controls and AIS / ISACA Spring Conference

· John Gunson, Jean-Paul de Blasis / THE PLACE AND KEY

SUCCESS FACTORS OF ERP IN THE NEW PARADIGMS OF BUSINESS MANAGEMENT/

· Jennifer Hahn, Deloitte & Touche/ ERP Systems:

Audit and Control Risks/ ISACA Spring Conference

· LORIN M. HITT, D.J. WU AND XIAOGE ZHOU / ERP Investment:

Business Impact and Productivity Measures/

· Michael Donovan /Successful ERP Implementation the

First Time/ Performance Improvement

· Nwankpa joseph kelechi (2007)/ the impact of erp

system on the audit process

· Richard Byrom (2003) /Audit Considerations for your

ERP implementation/ RPC Data Ltd

· Severin V. Grabski, Stewart A. Leech, Bai Lu, / Risks

and Controls in the Implementation of ERP Systems/ The International

Journal of Digital Accounting Research Vol. 1, No. 1, pp. 47-68

|