ANNEXE

ANNEXE 1 :

a) LES DONNEES UTILISEES

|

OBS

|

PIBK_A

|

SKP_A

|

SKH_A

|

PAO_A

|

|

1990

|

184,10

|

18,27

|

2,23

|

1,09

|

|

1991

|

199,00

|

18,34

|

2,32

|

1,13

|

|

1992

|

200,30

|

18,77

|

2,41

|

1,17

|

|

1993

|

220,60

|

18,85

|

2,62

|

1,18

|

|

1994

|

227,80

|

18,86

|

2,82

|

1,19

|

|

1995

|

241,00

|

19,06

|

3,02

|

1,20

|

|

1996

|

254,50

|

19,21

|

3,21

|

1,21

|

|

1997

|

270,00

|

19,23

|

3,40

|

1,22

|

|

1998

|

284,10

|

19,27

|

3,57

|

1,23

|

|

1999

|

301,10

|

19,27

|

3,74

|

1,24

|

|

2000

|

314,70

|

19,42

|

3,90

|

1,25

|

|

2001

|

334,80

|

19,50

|

4,04

|

1,26

|

|

2002

|

343,00

|

19,72

|

4,16

|

1,27

|

|

2003

|

350,70

|

19,56

|

4,28

|

1,29

|

|

2004

|

372,80

|

19,63

|

4,38

|

1,30

|

|

2005

|

369,70

|

19,78

|

4,49

|

1,31

|

|

2006

|

390,20

|

27,61

|

4,58

|

1,32

|

|

2007

|

406,70

|

36,71

|

4,67

|

1,33

|

|

2008

|

421,20

|

39,63

|

4,76

|

1,34

|

|

2009

|

431,75

|

30,69

|

4,84

|

1,35

|

PIBK_A : Produit Intérieur Brut à

prix constant du secteur primaire en milliards de FCFA (Source : comptes

nationaux INSAE)

SKP_A : Stock de Capital Physique du secteur

Primaire en milliards de FCFA (Source : Calcul auteur sur données du

MAPES)

SKH_A : Stock de Capital humain dans

l'agriculture en millions d'années d'instruction (Source : calcul auteur

sur données des RGPH1, RGPH2 RGPH3)

PAO_A : Population Active Occupée dans

l'Agriculture en millions d'emplois effectifs (Source : calcul auteur sur

données des RGPH1, RGPH2 et RGPH3)

b) Nom et libellés des variables

utilisées

|

Nom des variables

|

Libellés des variables

|

|

PIBK_A

|

Produit Intérieur Brut agricole à prix constant

|

|

SKP_A

|

Stock de Capital Physique dans l'agriculture

|

|

SKH_A

|

Stock de Capital Humain dans l'Agriculture

|

|

PAO_A

|

Population Active Occupée dans l'agriculture

|

|

PGF

|

Productivité Global des Facteurs

|

|

L+ Nom de variables

|

Logarithme naturel de la variable

|

|

G+ Nom de Variable

|

Taux de croissance de la variable

|

|

Nom de Variables + S ou Nom de Variables + FOR

|

Variables estimées ou variables simulées

|

ANNEXE 2 : TESTS DE RACINE UNITAIRE SUR LES SERIES a)

Tests de racine unitaire sur log (skh_a)

Null Hypothesis: D(LOG(SKH_A)) has a unit root Exogenous:

Constant, Linear Trend

Lag Length: 1 (Automatic based on SIC, MAXLAG=1)

t-Statistic Prob.*

Augmented Dickey-Fuller test statistic -8.889699

0.0000

Test critical values: 1% level -4.616209

5% level -3.710482

10% level -3.297799

*MacKinnon (1996) one-sided p-values.

Warning: Probabilities and critical values calculated for 20

observations and may not be accurate for a sample size of 17

Augmented Dickey-Fuller Test Equation Dependent Variable:

D(LOG(SKH_A),2) Method: Least Squares

Date: 09/28/10 Time: 21:58

Sample (adjusted): 1993 2009

Included observations: 17 after adjustments

|

Variable

|

Coefficient

|

Std. Error t-Statistic

|

Prob.

|

|

D(LOG(SKH_A(-1)))

|

-1.175281

|

0.132207 -8.889699

|

0.0000

|

|

D(LOG(SKH_A(-1)),2)

|

0.174435

|

0.110055 1.584981

|

0.1370

|

|

C

|

0.099417

|

0.010867 9.148629

|

0.0000

|

|

@TREND(1990)

|

-0.004612

|

0.000507 -9.103692

|

0.0000

|

|

R-squared

|

0.873369

|

Mean dependent var

|

-0.001117

|

|

Adjusted R-squared

|

0.844146

|

S.D. dependent var

|

0.012977

|

|

S.E. of regression

|

0.005123

|

Akaike info criterion

|

-7.507811

|

|

Sumsquaredresid

|

0.000341

|

Schwarz criterion

|

-7.311761

|

|

Log likelihood

|

67.81639

|

F-statistic

|

29.88681

|

|

Durbin-Watson stat

|

0.387358

|

Prob(F-statistic)

|

0.000004

|

b) Test de racine unitaire sur log (SKP_A)

Null Hypothesis: D(LOG(SKP_A)) has a unit root Exogenous: None

Lag Length: 0 (Automatic based on SIC, MAXLAG=0)

t-Statistic Prob.*

Augmented Dickey-Fuller test statistic -1.978645

0.0483

Test critical values: 1% level -2.699769

5% level -1.961409

10% level -1.606610

*MacKinnon (1996) one-sided p-values.

Warning: Probabilities and critical values calculated for 20

observations and may not be accurate for a sample size of 18

Augmented Dickey-Fuller Test Equation Dependent Variable:

D(LOG(SKP_A),2) Method: Least Squares

Date: 09/28/10 Time: 22:06

Sample (adjusted): 1992 2009

Included observations: 18 after adjustments

|

Variable

|

Coefficient

|

Std. Error t-Statistic

|

Prob.

|

|

D(LOG(SKP_A(-1)))

|

-0.497702

|

0.251537 -1.978645

|

0.0643

|

|

R-squared

|

0.175506

|

Meandependent var

|

-0.014407

|

|

Adjusted R-squared

|

0.175506

|

S.D. dependent var

|

0.123660

|

|

S.E. of regression

|

0.112286

|

Akaike info criterion

|

-1.481589

|

|

Sumsquaredresid

|

0.214337

|

Schwarz criterion

|

-1.432123

|

|

Log likelihood

|

14.33430

|

Durbin-Watson stat

|

1.107626

|

c) Test de racine unitaire sur log (PIBK_A)

Null Hypothesis: D(LOG(PIBK_A)) has a unit root Exogenous:

Constant, Linear Trend

Lag Length: 0 (Automatic based on SIC, MAXLAG=0)

t-Statistic Prob.*

Augmented Dickey-Fuller test statistic -8.720221

0.0000

Test critical values: 1% level -4.571559

5% level -3.690814

10% level -3.286909

*MacKinnon (1996) one-sided p-values.

Warning: Probabilities and critical values calculated for 20

observations and may not be accurate for a sample size of 18

Augmented Dickey-Fuller Test Equation Dependent Variable:

D(LOG(PIBK_A),2) Method: Least Squares

Date: 09/28/10 Time: 22:09

Sample (adjusted): 1992 2009

Included observations: 18 after adjustments

|

Variable

|

Coefficient

|

Std. Error t-Statistic

|

Prob.

|

|

D(LOG(PIBK_A(-1)))

|

-1.650782

|

0.189305 -8.720221

|

0.0000

|

|

C

|

0.097876

|

0.015334 6.382732

|

0.0000

|

|

@TREND(1990)

|

-0.002374

|

0.000882 -2.690150

|

0.0168

|

|

R-squared

|

0.835408

|

Meandependent var

|

-0.002950

|

|

Adjusted R-squared

|

0.813462

|

S.D. dependent var

|

0.042271

|

|

S.E. of regression

|

0.018257

|

Akaike info criterion

|

-5.017561

|

|

Sumsquaredresid

|

0.005000

|

Schwarz criterion

|

-4.869166

|

|

Log likelihood

|

48.15805

|

F-statistic

|

38.06714

|

|

Durbin-Watson stat

|

1.789591

|

Prob(F-statistic)

|

0.000001

|

d) Tests de racine unitaire sur log (PAO_A)

Null Hypothesis: D(LOG(PAO_A)) has a unit root Exogenous:

Constant

Lag Length: 1 (Automatic based on SIC, MAXLAG=1)

t-Statistic Prob.*

Augmented Dickey-Fuller test statistic -69.82077

0.0000

Test critical values: 1% level -3.886751

5% level -3.052169

10% level -2.666593

*MacKinnon (1996) one-sided p-values.

Warning: Probabilities and critical values calculated for 20

observations and may not be accurate for a sample size of 17

Augmented Dickey-Fuller Test Equation Dependent Variable:

D(LOG(PAO_A),2) Method: Least Squares

Date: 09/28/10 Time: 22:16

Sample (adjusted): 1993 2009

Included observations: 17 after adjustments

|

Variable

|

Coefficient

|

Std. Error t-Statistic

|

Prob.

|

|

D(LOG(PAO_A(-1)))

|

-0.968573

|

0.013872 -69.82077

|

0.0000

|

|

D(LOG(PAO_A(-1)),2)

|

-0.026147

|

0.014326 -1.825191

|

0.0894

|

|

C

|

0.008293

|

0.000161 51.53149

|

0.0000

|

|

R-squared

|

0.997137

|

Mean dependent var

|

-0.001425

|

|

Adjusted R-squared

|

0.996728

|

S.D. dependent var

|

0.005567

|

|

S.E. of regression

|

0.000318

|

Akaike info criterion

|

-13.10748

|

|

Sumsquaredresid

|

1.42E-06

|

Schwarz criterion

|

-12.96044

|

|

Log likelihood

|

114.4136

|

F-statistic

|

2438.294

|

|

Durbin-Watson stat

|

0.242785

|

Prob(F-statistic)

|

0.000000

|

ANNEXE 3 : ESTIMATION DES FONCTIONS DE

PRODUCTION

a) modèle de Solow à deux facteurs (capital et

travail)

Dependent Variable: LOG(PIBK_A)

Method: Least Squares

Date: 09/29/10 Time: 01:43

Sample(adjusted): 1991 2009

Included observations: 19 after adjusting endpoints

Convergence achievedafter 5 iterations

LOG(PIBK_A)=C(1)+C(2)*LOG(SKP_A)+(1-C(2))*LOG(PAO_A)

+[AR(1)=C(3)]+C(4)*D92+C(5)*D04

Coefficient Std. Error t-Statistic Prob.

C(1) 12.98178 0.615826 21.08026 0.0000

C(2) 0.040694 0.026417 1.540405 0.1458

C(4) -0.057142 0.009226 -6.193621 0.0000

C(5) 0.034323 0.009221 3.722272 0.0023

C(3) 0.967352 0.015784 61.28689 0.0000

R-squared 0.997989 Mean dependent var 26.43797

Adjusted R-squared 0.997414 S.D. dependent var 0.252289

S.E. of regression 0.012828 Akaike info criterion -5.653378

Sumsquaredresid 0.002304 Schwarz criterion -5.404841

Log likelihood 58.70709 F-statistic 1736.957

Durbin-Watson stat 1.374233 Prob(F-statistic) 0.000000

Inverted AR Roots .97

b) fonction de production de long terme

Dependent Variable: LOG(PIBK_A)

Method: Least Squares

Date: 09/29/10 Time: 00:52

Sample(adjusted): 1991 2009

Included observations: 19 after adjusting endpoints

Convergence achieved after 9 iterations

LOG(PIBK_A)=C(1)+C(2)*LOG(SKP_A)+C(3)*LOG(SKH_A)+(1-C(2)

-C(3))*LOG(PAO_A)+[AR(1)=C(4)]+C(5)*D91+C(6)*D04+C(7)*D01

+C(8)*D93

Coefficient Std. Error t-Statistic Prob.

C(1) 10.89271 0.299194 36.40683 0.0000

C(2) 0.045766 0.015026 3.045700 0.0111

C(3) 0.709734 0.107967 6.573621 0.0000

C(5) 0.034610 0.005269 6.568284 0.0000

C(6) 0.034452 0.005266 6.542007 0.0000

C(7) 0.017747 0.005270 3.367613 0.0063

C(8) 0.028672 0.005294 5.415967 0.0002

C(4) 1.042529 0.042849 24.33034 0.0000

R-squared 0.999445 Meandependent var 26.43797

Adjusted R-squared 0.999091 S.D. dependent var 0.252289

S.E. of regression 0.007606 Akaike info criterion -6.624276

Sumsquaredresid 0.000636 Schwarz criterion -6.226617

Log likelihood 70.93062 F-statistic 2827.809

Durbin-Watson stat 1.583911 Prob(F-statistic) 0.000000

Inverted AR Roots 1.04

Estimated AR process is nonstationary

c) Test de racine unitaire sur les résidus issus

du modèle de long terme (RESIDUSLT=résidus issus du modèle

de long terme)

Null Hypothesis: RESIDUSLT has a unit root

Exogenous: None

Lag Length: 0 (Automatic based on SIC, MAXLAG=3)

t-Statistic Prob.*

Augmented Dickey-Fuller test statistic -3.324892

0.0023

Test critical values: 1% level -2.699769

5% level -1.961409

10% level -1.606610

*MacKinnon (1996) one-sided p-values.

Warning: Probabilities and critical values calculated for 20

observations and may not be accurate for a sample size of 18

Augmented Dickey-Fuller Test Equation Dependent Variable:

D(RESIDUSLT) Method: Least Squares

Date: 09/28/10 Time: 22:59

Sample (adjusted): 1992 2009

Included observations: 18 after adjustments

|

Variable

|

Coefficient

|

Std. Error t-Statistic

|

Prob.

|

|

RESIDUSLT(-1)

|

-0.809578

|

0.243490 -3.324892

|

0.0040

|

|

R-squared

|

0.392209

|

Mean dependent var

|

0.000411

|

|

Adjusted R-squared

|

0.392209

|

S.D. dependent var

|

0.007688

|

|

S.E. of regression

|

0.005994

|

Akaike info criterion

|

-7.342212

|

|

Sumsquaredresid

|

0.000611

|

Schwarz criterion

|

-7.292747

|

|

Log likelihood

|

67.07991

|

Durbin-Watson stat

|

2.012627

|

d) Fonction de production de court terme

Dependent Variable: D(LOG(PIBK_A))

Method: Least Squares

Date: 09/29/10 Time: 00:55

Sample(adjusted): 1992 2009

Included observations: 18 after adjusting endpoints

D(LOG(PIBK_A))=C(1)+C(2)*D(LOG(SKP_A))+C(3)*D(LOG(SKH_A))

+(1-C(2)-C(3))*D(LOG(PAO_A))+C(4)*RESIDUSLT(-1)+C(5)*D94

+C(6)*D05+C(7)*D92+C(8)*D95+C(9)*D96+C(10)*D01+C(11)*D02

+C(12)*D03

|

Coefficient Std. Error t-Statistic

|

Prob.

|

C(1)

|

0.018414 0.003540 5.201111

|

0.0020

|

C(2)

|

0.033181 0.012612 2.630866

|

0.0390

|

C(3)

|

0.837787 0.097161 8.622634

|

0.0001

|

C(4)

|

-1.096157 0.280529 -3.907465

|

0.0079

|

C(5)

|

-0.053198 0.007363 -7.224597

|

0.0004

|

C(6)

|

-0.055084 0.006829 -8.065924

|

0.0002

|

C(7)

|

-0.049174 0.006900 -7.126597

|

0.0004

|

C(8)

|

-0.022990 0.007047 -3.262484

|

0.0172

|

C(9)

|

-0.019902 0.006845 -2.907747

|

0.0271

|

C(10)

|

0.014038 0.006409 2.190390

|

0.0710

|

C(11)

|

-0.016679 0.006553 -2.545354

|

0.0438

|

C(12)

|

|

-0.015372 0.006625 -2.320474

|

0.0594

|

|

|

R-squared

|

0.977421 Mean dependent var

|

0.043030

|

|

Adjusted R-squared

|

0.936026 S.D. dependent var

|

0.024018

|

|

S.E. of regression

|

0.006075 Akaike info criterion

|

-7.134564

|

|

Sumsquaredresid

|

0.000221 Schwarz criterion

|

-6.540983

|

|

Log likelihood

|

76.21108 F-statistic

|

23.61222

|

|

Durbin-Watson stat

|

1.937422 Prob(F-statistic)

|

0.000476

|

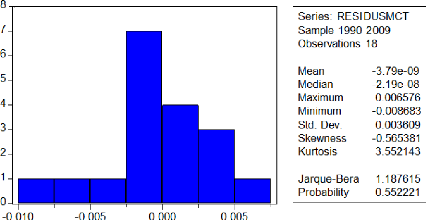

e) Test de normalité des résidus du

MCE

f) AUTOCCORELOGRAMME DES RESIDUS DU MODELE DYNAMIQUE DE

COURT TERME (test de bruit blanc)

Date: 09/29/10 Time: 18:05 Sample: 1990 2009

Included observations: 17

|

Autocorrelation

|

Partial Correlation

|

|

AC

|

PAC

|

Q-Stat

|

Prob

|

|

. **| . |

|

. **| . |

|

1

|

-0.278

|

-0.278

|

1.5561

|

0.212

|

|

. **| . |

|

.***| . |

|

2

|

-0.266

|

-0.372

|

3.0793

|

0.214

|

|

. *| . |

|

.***| . |

|

3

|

-0.073

|

-0.349

|

3.2034

|

0.361

|

|

. | . |

|

. **| . |

|

4

|

0.054

|

-0.307

|

3.2769

|

0.513

|

|

. |* . |

|

. **| . |

|

5

|

0.081

|

-0.243

|

3.4529

|

0.631

|

|

. | . |

|

. *| . |

|

6

|

0.035

|

-0.175

|

3.4888

|

0.745

|

|

. | . |

|

. | . |

|

7

|

0.059

|

0.014

|

3.6016

|

0.824

|

|

. | . |

|

. |* . |

|

8

|

-0.039

|

0.109

|

3.6567

|

0.887

|

|

. | . |

|

. |** . |

|

9

|

0.000

|

0.268

|

3.6567

|

0.933

|

|

. | . |

|

. |***. |

|

10

|

0.000

|

0.391

|

3.6567

|

0.962

|

g) Test d'homoscédasticité des erreurs

issues du MCE

ARCH Test:

F-statistic 0.420316 Probability 0.838464

Obs*R-squared 7.707749 Probability 0.462526

Test Equation:

Dependent Variable: RESID^2

Method: Least Squares

Date: 09/29/10 Time: 22:34

Sample(adjusted): 2000 2009

Included observations: 10 after adjusting endpoints

Variable Coefficient Std. Error t-Statistic Prob.

C 3.67E-05 4.14E-05 0.886533 0.5382

RESID^2(-1) -0.433900 0.903671 -0.480152 0.7150

RESID^2(-2) -0.501441 0.862769 -0.581200 0.6648

RESID^2(-3) -0.290359 0.490098 -0.592450 0.6595

RESID^2(-4) -0.151288 0.474166 -0.319061 0.8034

RESID^2(-5) -0.326557 0.436317 -0.748441 0.5910

RESID^2(-6) -0.355151 0.486007 -0.730752 0.5982

RESID^2(-7) 0.191870 0.494793 0.387778 0.7645

RESID^2(-8) -0.177400 0.521098 -0.340435 0.7911

R-squared 0.770775 Mean dependent var 1.11E-05

Adjusted R-squared -1.063026 S.D. dependent var 1.59E-05

S.E. of regression 2.28E-05 Akaike info criterion -19.04260

Sumsquaredresid 5.20E-10 Schwarz criterion -18.77027

Log likelihood 104.2130 F-statistic 0.420316

Durbin-Watson stat 2.689257 Prob(F-statistic) 0.838464

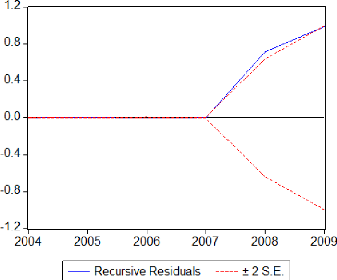

h) Résidus récursives

|