Assessing the viability of a rural microfinance network: the case of FONGS Finrural( Télécharger le fichier original )par Oniankitan Grégoire AGAI Solvay Brussels School of Economics and Management, Université Libre de Bruxelles - Advanced Master in Microfinance 2012 |

CHAPTER THREE: BACKGROUND OF THE MICROFINANCE INDUSTRY IN SENEGAL3.1 A growth led by savings and credit unionsThe microfinance industry in Senegal is a growing sector marked by the prominence of numerous MFIS, NBFIs and Savings and Credits Cooperatives or Mutuals. Three wide periods determine the microfinance growth in Senegal (Fall, 2012): § The First period was characterized by the financial crisis of eighties along with the creation of the first credit and savings institutions. During that period, a temporary framework related to the conditions of organizing, licensing and functioning of Savings and Credit Mutuals (decree n° 1702 of 23-02-1993) was set up and admitted 120 MFIs to be licensed. However no disposition of that law addressed the regulation issue of the «Groupements d'Epagrne et de Crédit (GEC)»10(*). § The second period (1993-2003) was marked by the enforcement of the legal framework on Decentralized Financial Systems (so called PARMEC law). That period was mainly influenced by the growth of the industry and the creation of MFIs' networks such as Unions, Federations, and Confederations which appeared as apex or umbrella institutions. § The Third period (2003-nowadays) is mainly dominated by the commercialization and the professionalization of the industry. During that period, MFIs are more focused on risks management issues and the reinforcement of the supervision of the industry. Especially, one observes a professional management of institutions, an effective control of network staff, and a focus on a good financial and institutional equilibrium.11(*) As of December 2010, the microfinance industry in Senegal was composed as depicted in the figure 1. Figure 1: Evolution of MFIs' juridical forms 2005-2010

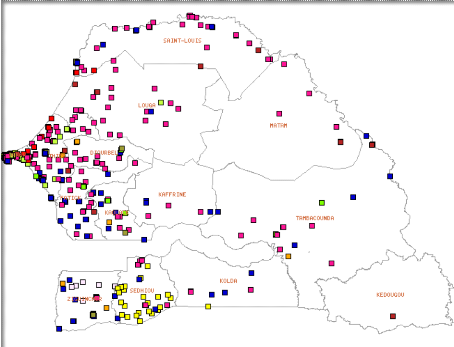

Source: Built from MEF/DRSSFD (2010, p.2) It appears through the figure 1 that savings and credit groups which dominated the industry between 2005 and 2007 recorded a decrease since 2007 due to the new regulation. Concurrently one witnesses the growth of isolated savings and credit cooperatives and mutuals as well as MFIs' networks. On the other hand, commercial non bank microfinance institutions are entering the sector whereas under convention non bank financial institutions are dropping out. Nonetheless, the industry is still dominated by the savings and credits unions which provide the essential in microfinance services. For example the seven most renowned savings and credit unions networks of Senegal network concentrate about 70% of the clients/members, 88% of deposits and 82% of outstanding loan portfolio of the industry since 2005 onwards (Daouda, 2006 quoted by SOS FAIM, 2007). 3.2 Rural areas are still under banked and underservedAs of December 2010 the number of services points of MFIs was 976 with an individual outreach of 12% (MEF/DRSSFD, 2010) representing more than 21% of services points, 24% of loan portfolio and 22% of deposits of the total finance sector (Diao, 2006). Despite the increase in number of MFIs in the number of clients, the microfinance in Senegal is still more urban and sub-urban than rural. The figure 2 shows the geographical outreach of microfinance industry in 2010. Figure 2: Number of MFIs services points as of December 2010

Source: MEF/DRSSFD (2010, p.3) The figure 2 reveals that more than 70 % of the MFIs operating in Senegal and their branches are located exclusively in urban areas including Dakar, Thiès and someway Kaolack, Fatick, Sedhiou and Saint Louis. As consequence, poor people living in rural and remote areas remain still unbanked. The other 30% MFIs, most often created from farmers and rural development organizations, are struggling to reduce the gap, allowing poor people having access to finance even with tiny amount of credit. * 10 The GEC (Savings and Credit Groups) are basic or primary associations which are not regulated as basic financial institution but operate based on the single authorization of the Finances Ministry. * 11 See http://www.microfinance.sn/page-250-1.html |

|