Microfinance and street children: is microfinance an appropriate tool to address the street children issue ?( Télécharger le fichier original )par Badreddine Serrokh Solvay Business School - Free University of Brussels - Management engineer degree 2006 |

General Board (21members)Consist of 21 MemberExecutive Committee (8 members) Monitoring Cell President Executive Director ED's Secretariat Director (Agriculture & Marketing) Director (Operations) Audit Division Training Division Manager (Finance & Accounts Division) Manager (HR & Admin Division) Program Manager (Education, Child Development & Gender Division) Program Manager (Health , Population, Nutrition & Sanitation Division) Program Manager (Agriculture & Marketing Division) Manager (Research, Planning and Program Development Division ) Program Manager (Micro Finance Division) Reporting and Supervision ------------------------------------ Communication, Coordination and Support B. Padakhep and Microfinance In the beginning of the 90's, the microfinance movement started its expansion, and Padakhep decided to do the same. In 1993, Padakhep launched a microfinance program which became, now, its major intervention: one of the «pillar» of the organisation, as Iqbal Ahammed likes to emphasize. As a starting point, they replicated the Grameen Bank model and, soon later, developed their own microfinance program. The main goal of the program is the strengthening and the empowerment of the poor. To do so, Padakhep chose to follow a holistic approach, providing financial services along with various other services, keeping a special emphasis on underprivileged women. This microfinance program is structured around 3 kinds of products: Micro Credit; Micro Savings and Micro Insurance. Here is a sample of their main products: Agriculture credit Hardcore poor credit Disaster management credit Urban credit: street children & adults Microentreprise Voluntary One time Weekly

From Padakhep (nd (b)) First, regarding microcredit, each product targets a particular segment of the poor population, as well as the less poor, with a particular emphasis on the extremely poor. The terms and conditions attached to their financial products depend upon the type of product. (see BOX) The size of the credit ranges generally from 2000 TK (30 US $) to 10000 TK (150 US $). The loan terms are of 1 year and Padakhep followed a weekly repayment strategy.

In order to deliver adequately its products and services, Padakhep has a network of more than 100 branch offices all throughout the country. Concerning the delivery methodology, Padakhep first identifies the beneficiaries (i.e. the target population with socioeconomic homogeneity) and then organizes them into small groups, ranging from 15 to 20 members. They attend weekly meetings, deposit their savings, and discuss socio-economic issues. Padakhep observes the group's performance during a couple of months before providing them credit and other services (e.g. skill development training, nutrition services, farm input, etc). Every group member is entitled to the credit, the group acting therefore as a guarantor. Parallel to this group-lending methodology, Padakhep uses progressive lending in order to reduce its risks. Moreover, training is provided along with credit for income generating activities management, in order to guarantee a good investment and therefore a good repayment. 28324 20906 57124 49688 71033 66233 0 10000 20000 30000 40000 50000 60000 70000 80000 2002-2003 2003-2004 2004-2005 Members Borrowers The microcredit program of Padakhep is in constant growth. The following figure gives the status of the members and the borrowers for the three last financial years88(*). It shows that the MFI has experienced a growth of more than 100 percent between July 2003 and June 2004, and that the growth rate between July 2004 and June 2005 has been equal to 33%.

From Padakhep (2005)

From Padakhep (2005) The savings scheme of Padakhep is a very important part of their microfinance activities and the savings mobilization is increasing over time. The following figure gives the savings mobilization (in millions TK) distribution for the three last financial years. From Padakhep (2005) 30.82 66.98 111.79 0 20 40 60 80 100 120 2002-2003 2003-2004 2004-2005 Savings Mobilization

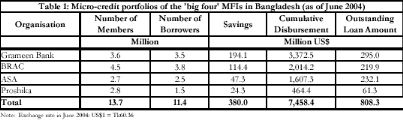

Finally, Padakhep is also running a microinsurance program ducts since 2000, which consists of a welfare fund. The beneficiaries deposit, before disbursing the main credit, a charge of 1% in the Welfare Fund. This amount can not be refunded during the beneficiary's lifetime, but only in case of any member's death. This fund has now accumulated more than 10 millions Taka. We need also to mention that Padakhep has developed a detailed computerized Management Information System which allowed to keep data for the majority of its microfinance projects. Comparing Padakhep to the Bangladeshi Microfinance industry, we could say that it is a middle range MFI. Indeed, the microfinance market in Bangladesh is dominated with the big four: Grameen Bank, BRAC, ASA and Proshika. This small table illustrate their main characteristics:

From Zaman, (nd) As Zaman highlights , «After the big four, the next largest NGO has 0.7 million clients and there are only ten NGOs who have more than 100,000 borrowers. The bottom line is that the majority of the MFIs are small (less than five thousand borrowers) and that the bulk of the access to microcredit is supplied by the four large MFIs». So, Padakhep, with its almost 70 thousands borrowers, can be characterized as a top medium Bangladeshi MFI; and, if following the same growth pattern than the previous financial year (i.e. 33 percent), could enter the top 15 MFI in Bangladesh in 2 years. C. Padakhep and street children «There is one population neglected by everybody and who needs our close attention: the street children» (Iqbal Ahammed, Executive Director of Padakhep) Our chapter 2 has highlighted the disaster of street children facing Bangladesh. In 1998, Padakhep, witnessing this disaster, was wondering how to contribute to the well-being of street children. Having no previous experience on that field, they decided to launch an exploratory study in order to assess the street children' needs and especially their vulnerability regarding sexual transmitted diseases, particularly HIV/AIDS. The conclusions of the report pointed out two main features: First was the global vulnerability characterizing those children, especially regarding sexually transmitted diseases, as well as the lack of basic services needed to their development. Secondly, the study team discovered that many street children were earning money through different income generating activities (IGA), but were facing two important constraints: first was the lack of a safe place in which to deposit their tiny earnings; and second was the lack of access to capital in order to start their own income generating activities. Therefore, the report highlighted two main recommendations which designed the roots of Padakhep' future intervention strategy: 1. Social interventions: The need to address street children with various developmental services which target their basic needs (psychological counselling, medical care, recreational activities, non-formal education, etc.) 2. Economic interventions: The need to strengthen street children on the labour market and to reduce their vulnerability as child workers by providing them financial services, along with other economical interventions. Following those recommendations, Padakhep started, the same year, a street children intervention program, with a special emphasis on STD/HIV/AIDS. As many street children had no landmark, a drop-in-centre (DIC) was first established in Mohammadpur area in 1998 and different developmental services were progressively provided. The panels of those social services includes many interventions, such as psychological counselling, health interventions, recreational activities and non-formal education and were financed thanks to Padakhep's own budget and the assistance of Action Aid Bangladesh. However, Padakhep considered that service provision and savings facilities alone can not help children reintegrate the society and stand «on their own feet». The NGO launched therefore, in a parallel process, an economic insertion intervention. After benefiting from basic social services and completing their non formal education, street children were provided with vocational training, which is twofold: 1. In house vocational training (i.e. in the DIC): trainings on tailoring, embroidery, boutique, packet making, candle making 2. Formal training (through two formal training centres of Dhaka city: Dhaka Ahsania Mission and UCEP-Bangladesh Training Centre): trainings on electrical works, pipe fitting, plumbing, beauty parlour activities etc, in order to ensure a safe job placement rather than hazardous jobs. After finishing their vocational training, street children are sent to shops, organizations, or firms. However, this program was facing a major constraint. Indeed, many children who followed this training did not want to work as employees - as pointed in our chapter 1, this may be due to the harassment faced by their previous employers - and some expressed their desire to run their own business. But to be able to do so, a capital was needed and no access was available to them. Having at this time 5 years of experience in microfinance all over Bangladesh, Padakhep decided to lend them some money as a pilot project, and to analyse the success and effectiveness of such scheme. From 1999 to 2000, only 25 children received credit. This small number was due to the newness of the project and the relative lack of funds. To expand this program, Padakhep needed the assistance of a donor. It is in that context that the NGO applied, in 2000, to the pro poor innovation challenge launched each year by CGAP -Consultative Group to Assist the Poor (CGAP/World Bank). The proposed activity was to open a Credit Branch Office for street children in Dhaka city. Thanks to the innovation of the project, Padakhep was selected among the winners and was awarded, in July 2001, US$ 50,000. In the same process, Padakhep got the assistance of other partners which allowed the expansion of its activities. The main partner organisation is the UNDP, through the ministry of Social Welfare. Indeed, Padakhep is one of the nine partner NGOs engaged in implementation of the ARISE program (Appropriate Resources for Improving Street Children's Environment), since April 2000. Thanks to this support, Padakhep has been able to create two more drop-in-centers in Dhaka city (in Mirpur and Kawran Bazar area), allowing therefore a deeper outreach. Here is a listing of all their projects targeting street children, as of January 2006:

From Padakhep (2005) Until now, Padakhep has delivered its services to approximately 15 000 children, through 3 drop in centres, 15 satellite centres, and 60 Centre based Schools/Open Air Schools. Padakhep provides all those services through its 3 drop-in-centres: one in Mirpur area (DIC 1); the second, DIC2, in Kawran Bazar (Tejgaon area); and the third, DIC 3, in Mohammadpur area (near Padakhep head office).90(*)

DIC under ARISE DIC 2 DIC 3 DIC 1

http://www.discoverbangladesh.com This map indicates how far those DIC are from each others. However, in terms of proximity with Padakhep head office, DIC 1 is better placed than DIC 2. But the latter is based in a particularly sensitive pocket area of street children, because it is close to a vegetable and a fish market, and to one of the most luxurious hotel of Dhaka city (Sonargaon). The following tables and figures indicate how many street children have transited through those DIC from January to December 2005 (classed by category). Remember... Category 1 SC - work and live on the street day and night without their family Category 2 SC - work and live on the street during the daytime and return to their family at night Category 3 SC - work on the street during the daytime and return at night to relatives Category 4 SC - work and live on the street and return to their family

We see that DIC 3 (Mohammadpur) has a majority of category 3 and 4 street children, i.e. children who are living either with their parents Analysed from Padakhep SPSS database We see that DIC-3 (Mohammadpur) has a majority of category 3 and 4 street children, i.e. children who are living either with their parents or with some members of their families. Regarding DIC-1 and DIC-2, things are a bit different. Indeed, DIC 2 has a majority of category 1 street children (i.e. the most vulnerable), and some children of category 2. DIC 1 (Mirpur) is largely dealing with category 2 street children, but has a larger «mixture» of categories than the other DIC. Another interesting fact is the total number of street children enrolled in each DIC. DIC Mohammadpur has enrolled 72% of all children enrolled in Padakhep. This is due to many reasons. First, we must recall that DIC 1 and DIC2 is part of ARISE project (UNDP). This project emphasizes the most vulnerable children (i.e. category 1 and 2) and provides also night shelter.

DIC Mohammadpur has enrolled more street children, but on a less permanent basis as it does not provide night shelter. Moreover, as pointed out by Ms. Farhana Prity Islam, the program officer of Padakhep's child development division, the proximity to slums is one major factor explaining this high enrolment, as DIC Mohammadpur is welcoming children from 4 slums areas.

Regarding gender, the majority of street children enrolled during this year are boys. Here is the distribution of boys and girls among the 3 DIC. Combining all these percentages, we find that 69% of the children enrolled are boys, and only 31% are girls. As pointed by Prity Islam, this small number may be due to the fact that Padakhep stopped providing night shelters to girls, as this has created some problems (between boys and girls) before. E. Padakhep and microfinance for street children As mentioned previously, Padakhep started its microfinance for street children program in the beginning of its activities with street children with a first focus on savings. Then, in 1999, credit was offered but the program was still small. Its expansion started with the CGAP's award fund in July 2001. The US$ 50,000 received has been allocated as followed:

This donation allowed a branch to start in Mohammadpur area, at 300 meters from DIC 3. This credit branch had double objectives: to provide street children with financial services, and to be the trigger of the urban microfinance program. First, savings and credits facilities were centralized in the branch. However, as it was not very convenient for the children (which had to move from the DIC to the Branch office in order to deposit or collect their money, and then coming back to the DIC for other activities), and desiring to give the best incentives to them to save a maximum, the system was decentralized and the savings facilities transferred to the DIC in July 2004. However, this decentralization was partial. Indeed, credit facility keeps being managed by the branch. When interviewing the staff about the reason(s) behind this, all pointed out the fact that they did not want to be in charge of credit services because they want to keep good relations with the children; and managing credit may create some tensions between them and the children. This microfinance program, based in Mohammadpur and partially linked to the branch, can be characterized as the «formal microfinance for street children program», and even if based in Mohammadpur, the credit facility was accessible to all street children from the other DIC. However, a problem appeared. Indeed, because of the long distance separating DIC 1 and DIC 3 from the branch office, children from those DIC had difficulty to come there in order to take a loan. Some staff members were first doing that for the children, but this was taking too much of their time and was not convenient at all. Two solutions appeared to the DIC managers. First was to keep credit only for children of Mohammadpur area, but this was unjustified (and even injust) as the demand for credit of other children was quite high. Second was to try to offer financial services to the children and to manage it «as best as they could», the revolving loan fund being taken from other budgets. This lead therefore to the progressive creation of an «informal microfinance for street children program, based in the DIC and without any link with the branch office Our two next sub-sections are aimed at highlighting the main characteristics of these formal and informal programs. § Formal program characteristics Regarding the formal program, children are first organized in «groups» (called «samity» in Bengali). As part of a group, children can then benefit from the two financial products offered to them by Padakhep: savings and credit. However, when discussing a bit deeply with Padakhep's management staff, we found that the group structure was not having a «real» function in the microfinance program. Indeed, children do meet in groups for awareness sessions, but do not discuss and manage savings and credit in group. After being part of a group and if interested to enter the microfinance program, children must pay 5 TK ($US 0.05) as a registration fee to receive their savings passbook. After, they begin to save (in the DIC) and each transaction is being recorded in their passbook. In a parallel process, the DIC staff records those data in a register book for administrative reasons. Padakhep has two types of savings products in their portfolio: 1. Voluntary savings: the children deposit and withdraw any amount of money «at anytime» (however, not possible after the staff leaves the office, i.e. 5 pm) 2. Weekly savings are compulsory savings. When the child receives a credit, he has to save at least 5 TK a week. Padakhep was providing, until June 2005, 7% interest on their

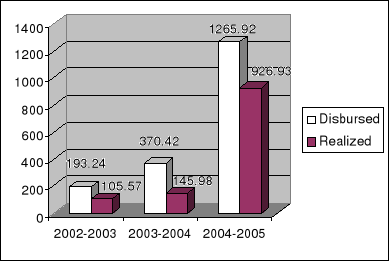

savings. They are now providing 6%. ELIGIBILITY CRITERIA § Attendance of the child? (day and night time) § Do they save money regularly? § Did they pay instalments of their previous credit? § Are they aware of the rules and regulations of the organization?Do they see their future IGA as profitable? If the child meets those criteria, the credit is disbursed. Regarding the loan sizes, it does generally range from 1000 TK to 5000 TK. Generally, loan repayment time is 1 year, but many children repay it after 6 months and children return the loan fund with 10% service charge a year. The following table illustrates the process for a 6-month term credit:

Children then invest the money in different income generating activities like vending tea, flower, dry food stuff; run small grocery hawking, shoe shining, etc. However, one of the core elements of the formal microfinance program for street children is the linkage with the guardians of the street children. Indeed, the beneficiaries of the formal program are children of category 3 and category 4, which means that all of them are living in slums with their family or relatives. Considering this point, Padakhep chose to link the guardians of the street children who were too young to benefit from a credit, hoping that the benefits of the credit will flow from the guardians to the street children. The children concerned by this form of credit were aged between 8 and 12 years old. When the guardian wants a credit, the DIC refers him or her to the branch. The guardians can get from 1000 to 5000 TK, and even more, depending on the cost of his/her business project. The following table summarizes all the products being offered by the branch.

§ Informal program characteristics The informal microfinance program, managed by DIC Mirpur and Kawran Bazar, has its own characteristics. The savings facilities are also centre based, the children depositing their money whenever they want (here too, up to 5 PM). Concerning interest rates, DIC Mirpur is providing an interest of 7% on deposits, whereas DIC Kawran Bazar is providing no interest. The recording system is different from the one of Mohammadpur. Indeed, children do not have a personal saving passbook. As explained by the DIC managers, children did not want to pay 5 TK for a passbook which will have a high probability to be lost in the street. So, the recording is being made in a global register book by the register officer. Regarding credits, the two DIC are managing it with their own funds (i.e. with the money taken from vocational training budgets). The terms and conditions are different: · DIC Mirpur is taking 10% a year of service charge on the loan amounts; DIC 2 (Kawran Bazar) is providing free interest loans. The loan conditions are quite «abstract» and rely mainly on the way staff perceives the children. This whole issue will be discussed in our next section. · Concerning the loan amounts, DIC Mirpur provides the same range of loan amounts than the formal program (i.e. from 1000 TK to 5000TK), whereas DIC Kawran Bazar is providing much smaller loan amounts, as those loans are more related to seasonal business creations rather than long term business. Therefore, we could say that DIC Mirpur program has quite similar characteristics than the formal program, the only differences being the passbook for savings, and the independence towards the credit branch for providing credit. § Microfinance for street children program and our comprehensive microfinance plus framework Seemingly, Padakhep follows our comprehensive microfinance plus framework: they provide financial services, vocational training and social services. However, this statement is rejected if we take a closer view on each component and their relationship. First, financial services are provided in an unorganised and differentiated way. First, the product design is inadequate and varies among DIC. Second, the eligibility criteria are either incomplete (for the formal program: no connection with vocational training), either abstract or inexistent such (for the informal program: no clear criteria). Moreover, the credit disbursement is poorly linked to vocational training. The following figure does illustrate Padakhep's holistic framework, and highlights an unclear flow of activities regarding savings, credit and their link with vocational training.

* 88 The difference between the total number of borrowers and the total number of members is one indicator of the additional services that are provided to the members (i.e. people benefit from various developmental services in their groups- such as awareness raising, etc - without taking a loan. * 89 From Padakhep (2005) * 90 The numbers attached to the DIC have no link with their creation date. * 91 Since July 2005 before the rate was at 15%. |

| |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||