Microfinance and street children: is microfinance an appropriate tool to address the street children issue ?( Télécharger le fichier original )par Badreddine Serrokh Solvay Business School - Free University of Brussels - Management engineer degree 2006 |

2.4.2. Program Effectiveness

Now that we know the profile of Padakhep's microfinance program, and that we have highlighted that this does not follow our model, we need to move to our second step of analysis, namely the program effectiveness. In order to be rigorous and complete in our analysis, we will evaluate both the formal and the informal programs, by trying, for each of them, to highlight the effectiveness of financial services provision. 1. Methods In order to evaluate the effectiveness of the intervention, we practiced individual in-depth interviews. As pointed in our methodology section, the children who did receive a loan were selected from the focus group discussions. In total, we proceeded to 19 individual in-depth interviews, among the 4 categories of children in the three DIC. The finality was not to make a comprehensive impact assessment, but just to capture the diversity of impacts. 2. Research questions #177; Regarding savings Our demand analysis underlined that street children need savings in order to better plan their personal and/or family future expenditures which are of three kinds: life-cycle, emergencies and opportunities. As a consequence, a saving program will be effective if it helps them accumulate large lump sums of money in order to meet those future expenditures. In order to do so, a saving scheme must be reliable, convenient and flexible in order to attract street children to set-up saving deposits. This statement leads therefore to ask three questions whenever analysing the effectiveness of Padakhep' street children saving scheme: 1. Do street children use the saving services made available to them? 2. Does Padakhep program help the children accumulate large lump sums of money? Those two questions will enable us to analyse whether Padakhep program provides reliable, convenient and flexible deposit services to street children. #177; Regarding credit Our demand analysis highlighted that some street children do need credit for their own income generating activities (IGA) or for their families IGA. The question to be addressed in terms of effectiveness measurement is whether access to credit has protected the child from hazardous economic activity and gave him/her the opportunity to launch a successful business. 3. Data analysis

Shreiner (1999) points out an interesting thing: «if they (customers) do not use it (saving services) repeatedly, they must be doing better elsewhere. For customers, good performance is measured by repeated use». This means that if street children do not use savings services made available to them, the program is simply not matching their demand. Let us therefore analyse it for each of the DIC. A. DIC Mohammadpur (FP)92(*) In order to assess whether street children are frequently using savings services, we need to make a zoom on the total saving deposits and withdrawal. The following table shows monthly deposits and withdrawal at the DIC from July 2004 to December 200593(*).

It demonstrates that street children use very actively the saving scheme, deposit and withdraw money whenever needed. This is a clear indicator of how street children value those services. The program accounted, in December 2005, a total of 381 members (including 53 guardians) and this number has been in constant growth since July 2004 (a growth of 157%, from 60 to 381 members).94(*)

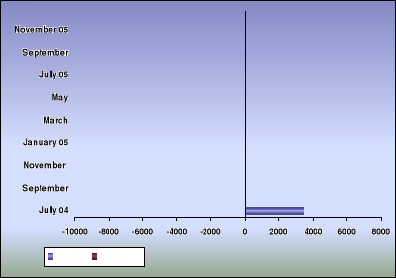

Those two indicators underscore how street children value saving services. Moreover, this satisfaction is highlighted further, qualitatively through our different participative sessions, where children pointed out how useful and needed was this service for them. B. DIC Mirpur (IFP)95(*) Street children of Mirpur do also use savings services made available to them. The following figure does illustrate it but tends to show that, even if children deposit and withdraw money whenever they want, the withdrawal seems to be higher than in Mohammadpur DIC. Indeed, the total deposits between July 2004 and December 2005 has been equal to 67,360 TK (990 US$) and the total withdrawal equal 68616 TK (1010 US$), which leads to a loss of 1256TK (20 US$). This deficit is, of course, due to the interest rate of 7% provided to street children on street children deposit accounts. Deposits and withdrawal (July 04 to Dec 05) TAKA

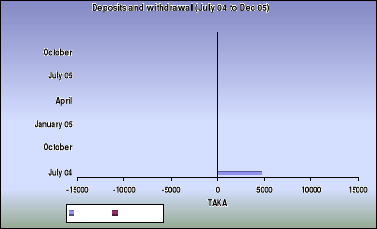

C. DIC Kawran Bazar (IFP) This program is also attracting savings, children depositing and withdrawing money frequently. Children have deposited, from July 2004 to December 2005, a total of 93,805 TK (1380 US$) and withdrawed 81,791 TK (1200 US $). The cumulative number of savers is equivalent to 402, all of them being boys. The following figure illustrates the total frequency of deposits and withdrawal.

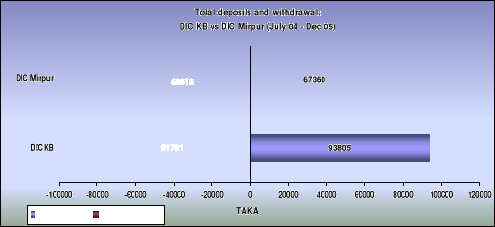

D. Consolidated analysis Let us now compare those 3 DIC. Our next figure shows that street children of Kawran Bazar DIC are the ones who deposit the more money, but also the ones who withdraw the most. We must recall here, whenever talking of DIC Kawran Bazar, that this IFP is not providing interest on saving, but is still in first position in terms of saving collection.

However, as this could be due to a higher number of savers, we found interesting to segregate those data and analyse the average deposit and withdrawal per street child.

The figures are clear: street children of Kawran Bazar (welcoming a majority of category 1 street children) have the most frequent use. In other words, those children deposit frequently money, but withdraw it also frequently. Finally, all those data do show that street children are using frequently their saving accounts, sign that Padakhep is offering them reliable, convenient and flexible savings services. Centre-based savings allows them to deposit some amount of money whenever they need it. However, as we did point in our section 2.3., monetary returns do not seem to be of considerable importance to street chidren, as DIC Kawranbazar, providing no interest, is the first program in terms of deposits collection.

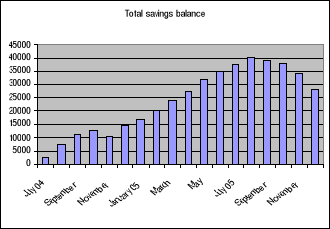

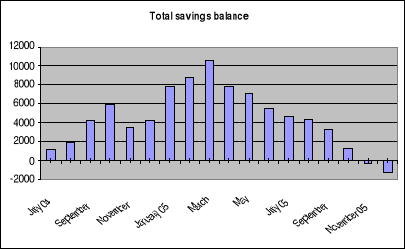

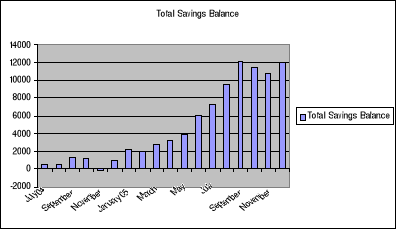

Our previous point indicated how street children use repeatedly saving services made available to them, a clear indicator of how they value such service. However, one of the core objectives of Padakhep saving scheme is to help street children accumulate large lump sums of money in order to plan their future expenditures (i.e. life-cycle, emergencies and opportunities). This section aims at enlightening this, by looking at two indicators: the evolution of the savings balance of the programs, and the personal saving accounts of the children. A. DIC Mohammadpur (FP) Regarding the total savings balance, the following figure demonstrates that this balance is in constant growth since the beginning of the program, with a slight reduction since September 200596(*).

However, even it shows that more money is being accumulated in the savings accounts of children (and their guardians), we need to examine in depth the saving pattern of the street children in order to get a more precise idea on how children do accumulate these large lump sums and in order to try to look whether this increase in the saving balance is not only due to an increase in the number of members. The savings books collected give a diverse picture on the amounts saved:

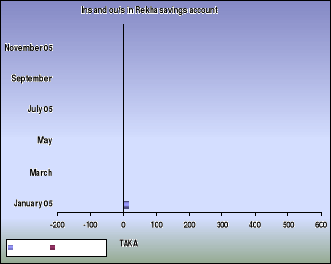

Let us now make a zoom on two of those children to see how they did accumulate those lump sum of money. § Case 1: Rekha Rekha, a girl of 13 years old, left her village with her parents when she was very young. Her father wanted to find a job in Dhaka city and started to work as a rickshaw puller. Besides, her mother found a job as a domestic helper. However, their combined salary was still very small (+- 30 to 40 Tk daily) and their economic condition was therefore very difficult. At the age of 7, Rekha entered Padakhep and soon later she got admitted in the non formal education program of Padakhep. In 2004, as her father increased income, Rekha started to receive weekly some money from her father. However, Rekha does not forget the difficult situation in which they are living and saves this money in order to support her family whenever they face any problem. Moreover, Rekha knows how important it is to save money for her own well-being and saves therefore money in order to start secondary school. Finally, Rekha added how her participation to some cultural events organized by Padakhep and their partners, allowed her to save more and more money (see March deposit, where Rekha got a prize and saved it). The following figure illustrated ins and outs of Rekha saving account.

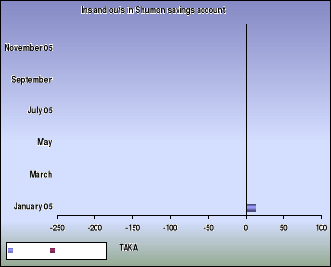

§ Case 2: Shumon Shumon is a young boy of 14 years old who lives in the slum of Bizli Mohalla, in Dhaka city, with his parents and his 4 siblings. His father has a small grocery shop in the slum area and is the only person who supplies income to his family. In order to support his family, Shumon works in the family's shop. In the beginning, Shumon was going to school but he finally had to stop when he was 12 years old in order to help his father. Shumon saves some money in Padakhep for two reasons. First, in order to help his family when they face any kind of problem; and second in order to open his own business in the future. This money is being given by his father. The monthly ins and outs of Shumon saving account are illustrated below. (starting with a balance of 212TK in Jan 05)

B. DIC Mirpur (IFP) The savings balance of DIC Mirpur is far to be equivalent to the one of DIC Mohammadpur. Indeed, we see a particularly high decline since March 2005, many children withdrawing their money.

The following table enlightens this decline:

This lead to a quite dangerous situation, in which the DIC is now in «deficit» with a negative balance. The savings books collected from 5 street children give a diverse picture on the total saving balance in December 2005.

However, the saving balance does not inform about the evolution across time of their savings. Indeed, we need an in-depth analysis of the saving accounts of children. Let us do that with some children. § CATEGORY 1: Bahrul Islam - a boy building up a large lump sum of money for his family

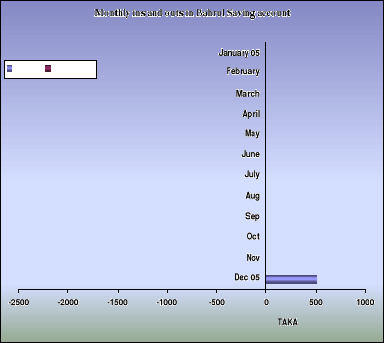

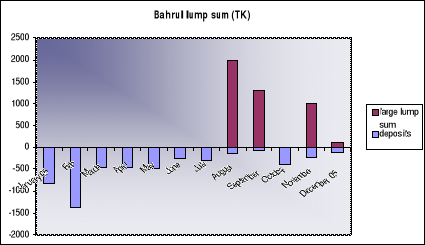

Bahrul Islam, now 13 years old, left his house 2 years ago because he had to bear some expenses for his family (educational expenditures of his 3 brothers & 1 sister) as his father was insane and his mother did earn little amount of money as a domestic worker. He arrived in Dhaka with his uncle. He first lived in his uncle's house but his aunt mistreated him. He therefore left his uncle's house and went to live with some other children he knew in the street. Sleeping in the street near the National Stadium, he was always harassed by people stealing money from him, and by mosquitoes. At the beginning, he used to collect some wastage and then he was interested to do cycle rickshaw servicing. He learned only by observing and then got a loan which allowed Bahrul to start his activity. The money he was earning was put in his saving account until he built a large lump sum of money that he sent to his home village through a trustable person working as a bus driver. The following figure shows how Bahrul save money until he had enough to withdraw 2000 TK and 1500 TK.

The next figure shows the deposit amount as negative values, because the child takes money from his available income and deposits on his account, until he will build a large sum of money.

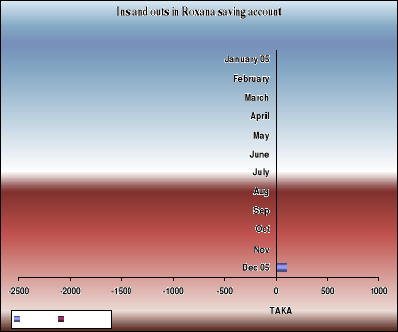

§ CATEGORY 2: Roxana - a 12 year old girl building up a large lump sum for herself 97(*) Born and brought up in a slum with neglect and in absolute poverty, Roxana faced many difficult circumstances in her life. When she was 6 years old, her father, a taxi driver, died in a car accident. Soon after, her mother received 5000 TK (74 US$) from the car company in order to help maintain her family, composed of 1 other sister and 3 brothers; and her mother invested it in a small cake business. Then, she got married with a man who had already 3 wives and was allegedly only interested by her mother's business. Beginning to take the revenue of her wife' shop, her business went bankrupt. Because this man was always ill-treating her and her siblings, Roxana decided, one day, to leave home with her siblings and to go living with her grandmother in a place with no water supply and only ugly toilets. But after one month, Roxana had to fin a job in order to help financially her grandmother and her siblings. She therefore began to work and to collect some vegetables in some market places, as well as wastages. But, whenever collecting wastage, the worst happened: a man abused from her sexually. She then changed place and got involved in Padakhep's program.. Until that time, she never lost contact with her mother and now she is living with her. At Padakhep, Roxana is saving some money in order to buy things for her in good occasions. She therefore withdrew, in October and December 2005 (Aid El Fitr and Aid El Adha festivals), 2000 TK and 1000 TK, with which she bought some nice dresses and other things. The monthly ins and outs of Roxana is being illustrated in the following table:

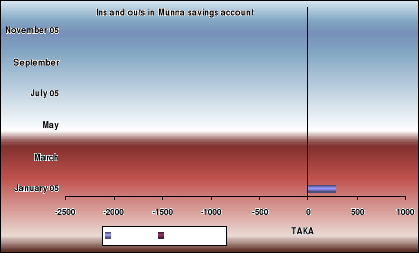

CATEGORY 3 : Munna - a 16 years boy building a large lump sum for his grandmother and himself Munna, a 16 years old boy, was a child living peacefully in Sherpur, his home village. When his mother died, Munna was 6 years old. His father got a new wife, but his stepmother ill-treated him and his 2 brothers. To shun these physical and psychological harassments, Munna came to Dhaka city when he was 10 years old with his 2 brothers and stayed with his grandmother. Then, his life suddenly changed. Because he spent most of his time in the streets of Dhaka, he became drug addicted and got involved in «Mastaans» group. Hopefully, after some time, he met Padakhep's staff and entered in 2002 in DIC Mirpur. Therefore, in order to afford his basic needs and to help his grandmother and young brothers, he found some hazardous jobs (scavenger collector, etc). But soon later, Munna opened his own business and saved some money in Padakhep in order to better help his grandmother and his siblings whether an emergency would arise, as well as for his own future. But Munna does not send money to his home village, as his stepmother is still there.

C. DIC Kawran Bazar (IFP) Our previous point did highlight that street children of this DIC deposit but also withdraw very repeatedly. However, the total savings balance at the DIC is growing (with a slight decrease in October - Aid festival), which means that more and more money is being stored.

Unfortunately, we have not been able to collect detailed savings data from the register. But our discussions did indicate that they have been able to accumulate large lump sums.

Let us now discover Swapon saving activities. CATEGORY 1 Swapon, a 16 years boy saving for meeting emergency At the age of 12, Swapon, whose father died some years before, left his mother because she ill-treated him. He then discovered the street life, before Padakhep welcomed him in his DIC and offered him with various services. In order to survive, Swapon collects some vegetable in Karwan Bazar market and sells it. He buys it 8 TK a kilo, and sells it at 9 TK. This small profit enables him to meet his present expenditures. But Swapon knows how the future is uncertain and saves therefore some money in order to meet his future expenditures. One day, Swapon made an accident in the street, and needed to make a leg operation urgently. Fortunately, Swapon had already saved at that time 3000 TK, which allowed him to pay for the operation cost. D. So, do street children accumulate large lump sum? It seems clear from these figures that street children do accumulate large lump sums, and mainly withdraw it at a precise time for meeting a particular expenditure. However, this tends to demonstrate that Padakhep's saving scheme, based in the drop-in-centre, is reliable, convenient and flexible. Moreover, it shows that interest rates are of little importance, DIC Kawran Bazar being the first in deposits collection, without providing any interest.

Answering this question is essential. Indeed, after having highlighted that the different DIC provide some credit to street children and that many of those children do repay it without facing any difficulty, we need now to evaluate the impact generated by those credits on them. In order to do so, we need to approach the 4 categories of street children separately, by drawing on some case studies collected from our individual-in-depth interviews. A. CATEGORY 1 «... who work and live on the street day and night without their family» As pointed in our program profile, two DIC welcome category 1 street children: DIC Kawran Bazar and DIC Mirpur. Those DIC provide different types of credits. Comparing the two programs in terms of «impact» will therefore enable us to capture valuable learning. § DIC Kawran Bazar This DIC is providing street children with free interest loans of relatively small amounts. The following table provides the loan disbursements of the DIC from January to December 2005, and the investments made by the street children.

The street children credit investments can therefore be classified in 4 categories (see below) n SC SCFigure 1 10.5% 18.5% 37% 34%

n. SC = Number of Street Children Those credit investments are seasonal businesses that are made in some specific occasions (such as Aid festival). Let us Sujon and Kanchan explain it to us. Case 1: Sujon and his two credits § Credit amounts: 1st loan - 30 TK; 2nd loan - 70 TK § Purpose: Seasonal business § Repayment: Completed § Description: Sujon is a boy of 13 years old. He was living in a village nearby Dhaka with his father and mother. As his father used to beat him, Sujon decided to leave his village and to go to Dhaka. When he arrived in the city, Sujon has been welcomed by Padakhep and started to work in the vegetable and fish market of Kawran Bazar (as a «Minti»). He earned a daily income of 40 to 50 TK (0.60 to 0.70 US$). He spends a part of it (+- 25 TK daily) and saves the remaining amount in case he faces any emergency. The first credit he received (30 TK) was to buy chocolate and sell it near the road signal, in Kawran. He was making a daily profit of 15 to 20 TK, which allowed him to repay his loan after 4 days.. The second credit he received (70 TK) was to buy some water and sell it during Ramadan for iftar. Thanks to it, he made a total profit of 50TK (60% of the loan amount), and repaid his credit after 3 days. Parallel to this, Sujon was still working regularly at the market as a Minti, but planned to start a business...without knowing which one exactly though. Case 2: Shahin and his three credits99(*) § Credit amounts: 1st loan - 400 TK; 2nd loan - 300 TK; 3rd loan - 100 TK § Purpose: Seasonal business § Repayment: Completed § Description: Kanchan is a 15 years old boy who lived the worse. His father died and his mother was, alone, keeping them on their feet. Whenever playing football in his village with other children, some «Mastaans» came and offered them biscuits, which were unfortunately «poisoned». They felt sense less and were kidnapped by those criminals. They brought them near Dhaka city. There, they stayed 7 days, locked in a small room, with fear and without any food. Hopefully, they finally found a way to escape and arrived near Tejgaon railway station. There, Kanchan was found by Padakhep's staff and joined the program. But Kanchan was so much terrorized that he needed many psychological counselling sessions before restarting to live «normally». After a while, Kanchan took a loan from Padakhep (400 TK) in order to buy chocolate bars and to sell them on the streets. He was earning 50 to 60 TK daily, and was putting all this money in his savings account in order to repay his loan. But while selling those chocolates at the signal, police men were threatening him and he had to change place. After having repaid the loan, he took a second credit of 300TK in order to sell sugar cane and was earning daily 100 TK. He therefore repaid the entire credit amount within 5 days. His third credit was 100 TK, during Ramadan, in order to sell water for Iftar. After 1 month (end of Ramadan), he repaid the entire loan amount without difficulty. A major part of all the earnings generated by these investments have been deposited in his saving account, which had a balance of 300 TK in January 2006. Now, Kanchan is not working and uses his saving money. When talking about the future, Kanchan says he wants to open a grocery shop. § DIC Mirpur DIC Mirpur is also addressing category 1 street children, but at the difference of the previous DIC, does provide credit of larger amounts to them. Those are generally paid in 23 weekly instalments (6 months) and may or may not be linked with the vocational training received. Case 1: Shafikul Islam § Credit amount: 2000 TK § Purpose: Electrical material § Repayment: Completed § Description: Shafikul is a boy of 16 years old who left his home village after his father went away and got married with another woman. He therefore needed to support his mother and his siblings. As soon as he arrived in Dhaka, he met in the street a staff member from DIC Mirpur and entered the program. He had to find a job, and started to work as a «Ferry Walla»pourquoi tu rajoutes un «h» à la fin, lol (i.e. carrying some goods and selling it to other shops). He was buying goods in credits and repaid the informal credit (from the MOHAJAN) when he sold all the goods. He saved, from his earning, 20 to 30 TK daily. In June 2004, Shafikul got a job at Padakhep as peer educator and earned monthly 1000TK. In November 2004, Shafikul got some vocational training at Dhaksania Mission (one of Padakhep's partner) in electrical technics. Soon later, he received a loan in January 2005 of 2000 TK in order to buy electrical material. He joined therefore an electrical shop where he worked there from 5 PM to 7 PM and gets 10 TK a day. Sometimes, he also uses his instruments to do some «personal» reparations. He finished the repayment in 23 weeks. Now, he is a little bit worried about his future and wants to establish his OWN grocery shop (electrical) in the future. Case 2: Chowdhurry § Credit amount: 2000 TK (30 US $) § Purpose: Vegetable shop § Repayment: Completed § Description: Chowdhurry, a child of 12 years old, is originating from Noakhal. In order to support his family which was living in hard poverty, Chowdhurry decided to leave his home village when he was 9 years old. He left with his cousin and went to Dhaka city. First, his cousin found for him a job as a domestic worker, but he was ill-treated and usually tortured by the house lord. After 2 months of work, Chowdhurry left the house and «arrived» in the street. Hopefully, he met one child who told him about Padakhep and entered the program. In January 2005, he received a credit of 2000 TK in order to start a vegetable shop. But, as soon as his older brother heard about that, he left the village, came to Dhaka and took the control of the shop. First, they were both working in their new vegetable shop, but soon later some problems appeared between them and Chowdhurry had to leave the business. He then found another work in a cement factory, where he has been working since October 2005 9 to 10 hours a day. «Hopefully», his brother did pay the loan installments, and felt problems only 2 times, where Chowdhurry did pay for him. When talking about the future, Chowdhurry says that he wants to leave his present job (which he does not like) and start his own vegetable shop § Summary points Those cases, as well as our different discussions with street children, highlight different interesting facts about category 1 street children: 1. DIC Kawran Bazar allows children to start some seasonal businesses. They do it, but many of them do want to start their own permanent businesses which require larger loan amounts. 2. Those small seasonal business are only a survival strategy, and does not allow the child to plan for the long term. 3. DIC Mirpur does demonstrate that the ones who receive large loan amounts in order to start their own permanent businesses face some difficulties, such as intrusion of a family member or low profit margins. 4. Some, like Shahin, may face some problems with their businesses because of external factors B. CATEGORY 2 «... who work and live on the street day and night with their family» Those children are present in DIC Kawran Bazar and Mirpur, though in higher number in Mirpur. Let us therefore zoom on two of children, one in each DIC. Case 1: Jibon (DIC Kawran Bazar) § Credit amount: 1st loan - 200TK; 2nd loan - 500 TK § Purpose: Seasonal business § Repayment: Completed § Description: Jibon is a 14years old boy living with his parents on the streets of Dhaka. He is the older boy of the family. In order to support better his family, Jibon works in the DIC as a peer educator and receives monthly 1000 TK (15 US $). However, Jibon knows how profitable it is to start some seasonal businesses. He therefore received a credit of 200 TK (3 US$) during Ramadan (October 2005) in order to sell water for Iftar. After repaying back the money, Jibon took another loan in January 2006 of 500 TK (7.50 US$) in order to sell some snacks near the Parliament house before Aid El Adha festival100(*). Thanks to this second loan, he earned a daily profit of 200 TK. At the end of the 4 days, Jibon was able to collect 800 TK as profit and to save a large part of it for his personal future expenditures. When talking about the future, Jibon says he wants to start his own permanent business. Case 2: Roxana and her cake business (DIC Mirpur) § Credit amount: 2000 TK (30 US$) § Purpose: Cake business § Repayment: completed § Description: We all remember Roxana,

this young girl of 12 years old who faces so many difficulties.

§ Summary points: 1. Jibon tries to maximize his profits by engaging in different seasonal businesses. Even if this is a short-term survival strategy, it does not provide him with a long term perspective 2. Roxana does also show us that family intrusion can be dangerous. Her mother involvement in the business was the cause of «failure». C. CATEGORY 3 «...work on the street during the daytime and return at night to their relatives» Munna and his successful investment § Credit amount: 4000 TK (60 US $) § Purpose: Tea stall § Repayment: Completed § Description: We remember Munna, who is supporting his grandmother and his siblings thanks to his savings. In June 2004, Munna took a loan of 4000 TK to open a tea stall in Mirpur. He repaid it after 6 months without facing any difficulty. Munna values a lot his business which generates high profit margins and enables him to support his grandmother, his siblings and himself! When talking about the future, Munna is very confident and says he wants to expand more and more his business. D. CATEGORY 4 All category 4 street children are part of Padakhep formal microfinance program, located in DIC Mohammadpur and in the branch. Because of the importance such program has in the mind of Padakhep, we will highlight here 5 case studies, and seek the learning points we could get from them. Case 1: Rekha and her cake business § Credit amount: 2000 TK (30 US$) § Purpose: Cake business § Repayment: Not yet completed § Description: Rekha is not unknown to us. Remember our previous section where we described Rekha saving strategy. In October 2005, Rekha received a loan of 2000 TK (US$29) in order to start her cake business. Thanks to this loan, Rekha has been able to buy some basic inputs for her street business and to sell cakes (i.e. handmade panckakes). After now 3 months, she has already repaid half of the amount (1000 TK) and her business is running well. The Now, Rekha got admitted to secondary school and will work part-time in order to be able to go to school. Case 2: Shumon and his father's grocery shop § Credit amount: 5000 TK (74 US $) § Purpose: Parents business § Repayment: completed § Description: Our savings section talked about Shumon, who was saving money in order to help his family and to open his own business. Apart from the support he is providing to his parents business, Shumon took a loan of 5000 TK in January 2005. This credit has been totally invested in his father grocery shop, and Shumon repaid it in June 2005 thanks to the money he received from his parents. Now, Shumon is usually working in his father's shop and wants to open his own business in the future. Case 3: Gewel and his grocery shop § Credit amount: 5000 TK (74 US $) § Purpose: start a grocery shop § Repayment: completed § Description: Born in Dhaka (Barichal district), Gewel, a 17 years old boy, always lived in slums. Beginning to discover little by little the street world, he got involved in a «mastaans» gang (see chapter 2 for a definition). But he slowly got out from this vicious circle when discovering Padakhep. He began to save money and, in June 2004, Gewel took a loan of 5000 TK (US$ 74) in order to start a grocery shop. He paid back his loan after 45 weeks without facing any major difficulty. Concerning his future, Gewel is very optimist and wants to take another loan to expand his business, just after completing secondary school. Case 4: Shahida and her father's potato business § Credit amount: 2000 TK (30 US$) § Purpose: Parents business § Repayment: completed § Description: Chahida, a girl of 17 years old, is living with her parents in a slum of Dhaka city. Her father was disabled and therefore could not maintain her family. As she is the older child in the family, she worked in a garment factory in order to support her parents and her younger siblings. She heard after of Padakhep and entered in June 2003. There, at Padakhep, she received various types of services and because of her high capacity in dealing with other street children, she was proposed a job in Padakhep as a peer educator and was earning 1000TK a month. She began to save a part of this amount for two purposes: to get her secondary school certificate, and to have access to credit. She did this and got therefore 2000 TK as credit. As she knew that giving money to her parents is not a sustainable solution for her, she gave this credit amount to her father in order to start a potato chips business at home, as he is disabled. She managed to work in the same time in her father's shop, and her father gave her the weekly instalments which allowed her to repay the loan after 6 months. When talking about the future, Shahida wants to get her secondary school certificate and to start working with children. Case 5: Raju and his training § Credit amount: 2000 TK (30 US$) § Purpose: Mobile materials for his training § Repayment: one instalment remaining § Description: Raju is a young boy of 13 years old who lives with his parents and his 3 siblings in a slum of Dhaka city. His father is a mason helper and earns daily 50 to 60 TK, whereas his mother is a housewife. Raju has one passion: mobile phones. He knows how to repair every mobile phone. In January 2005, Raju took a loan of 2000TK in order to invest it for buying mobile reparation material for his cousin's mobile shop. However, Raju is still a trainee and does not get any income from his activity. However, he repaid the loan thanks to some small reparations he is doing besides his traineeship and to some seasonal businesses. When talking about the future, Rau has one desire: to open his own mobile shop. § Summary points 1. Shumon and Shahida did invest the credit in their families businesses. Shumon does want to start his own business and Shahida does not want at all to have a business. 2. Gewel made a successful investment which allows him to support his family and to meet his own expenditures. 3. Raju, even if he benefited from a credit in order to buy mobile material, did only find an unpaid traineeship and is paying back his loan thanks to other activities. 4. Learning points: program effectiveness The various programs do show a mitigated picture on the effectiveness of the intervention. #177; Regarding savings

The different savings schemes seem to be reliable, convenient and flexible, the street children using those savings services intensively, and being able to accumulate large lump sums. Moreover, it appeared that providing interest rate is of little importance to the children, demonstrating therefore their high needs to save money and maybe the option for a microfinance program for not providing interest rate, reducing therefore their costs and impacting positively their sustainability. Placing savings services in drop-in-centres is surely the key of their success, which confirms the proposition of our comprehensive microfinance plus framework. #177; Regarding credit On one side, when children are being given small loans (for starting seasonal businesses), those loans do not guarantee a long-term perspective to the children. On the other side, when children are being given larger loans, their businesses seem often far to be a way towards empowerment: the family intrusion does usually inhibit their businesses, or the child faces some difficulties in managing it in a profitable way. When describing our microfinance model for street children in our section 2.3., we pointed out the necessity to combine the provision of financial services with training (production or service; entrepreneurship and management). Beyond some positive impacts of Padakhep's intervention, we witness different risky factors in Padakhep's program: ü Some street children receive production training but no entrepreneurship and management training ü Start a service oriented business (such as a grocery shop) without getting a service oriented training, entrepreneurship and management training ü Some children, like Raju, pay for their production oriented training with the credit amount received; even if he repaid his loan, his gain is limited and, moreover, it creates uncertainty for his future. ü The families businesses seem to be successful, but the question of the impact on the child is mitigated ü Linking the guardians to the program might be negatively impacting the children So, here, both the question of financial services (design and delivery) and of training appears to be the great missing point of Padakhep's credit point, and needs to be strengthened. * 92 FP means formal program. * 93 As pointed in our program profile, savings services have been decentralized (from branch to the DIC) since July 2004. The DIC is therefore keeping the total data since this date. * 94 A « member » is different from a « saver ». If a person expresses his/her interest to enter the saving program, Padakhep «opens a saving account»; but this person may start saving some months after. So, all members do not deposit money; but it show that they value such services. * 95 IFP means Informal Program * 96 One of the reasons of this reduction may be due to the two Eid festivals: one in October 2005 and the second in January 2006. The staff members highlighted how children withdrawed money in order to buy gifts for themselves and their siblings. * 97 Roxana is a pseudonym. Indeed, due to the difficult circumstances the girl faced, we prefer not to mention her true name in order to respect her intimacy. * 98 Water was a particularly lucrative activity for children during Ramadan: indeed, those children were selling water for «iftar» (at sunset time) * 99 As for «Roxana», we decided not to use the true name of the child, considering the hard events he experienced. * 100 Aid El Adha is the second Muslim festival where the believers sacrifice generally a sheep, following the tradition of Abraham . |

|