La microfinance, un défi d'adaptation au contexte localpar Clara Bécard HEC Paris - Master in Management 2021 |

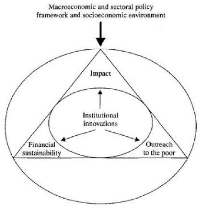

4 June 2021 Public Report M2 / International Business Major Master research paper Microfinance, an adaptation challenge to the local context Adjusting practices for an inclusive microfinance sector in Bangladesh and France La microfinance, un défi d'adaptation au contexte local L'ajustement des pratiques pour une microfinance inclusive au Bangladesh et en France Clara Bécard Under the supervision of M. Laurence Moret 2 AbstractMicrofinance is one of the most successful examples of reverse innovation: born out of the determination of a university professor in the Bangladeshi countryside and his trial with forty-two women from a small village, it is recognized today by the largest economies as a powerful tool in fighting poverty in all kinds of countries. With a growth rate of around 20% in the 2000s and 7% in the 2010s, the total worldwide number of borrowers amounted to 139.9 million in 20181. However, since microfinance is used in so many countries, it is applied in very different contexts and in various formats. It is not a homogenous phenomenon, but rather a diverse one, resulting in different levels of success depending on the location. Bangladesh, the birthplace of microfinance, and France, pioneering it in Europe, are worldwide sources of inspiration for the sector. Even though used differently in both countries, microfinance is a tool that, with analysis, innovation and determination, can be adapted and implemented to generate efficient practices with tangible results. This thesis examines in detail how one idea of tackling poverty has fared in very different environments, in an attempt to provide recommendations for a sector that still has a long road ahead. 3 1 Microfinance Barometer 2019. 4 Executive Summary IntroductionWinning the 2006 Nobel Peace Prize2, counting tens of thousands of over-indebted borrowers in Andhra Pradesh in 20103, increasing the level of financially-included adults worldwide from 51 to 69% between 2011 and 20174, questioned by the 2019 Nobel Prizes in Economic Sciences5... While microfinance has become an integral part of the fight against poverty and unemployment in the past 30 years, it is alternately successful and controversial. In some countries, it advances efficiently and is approved almost unanimously, following the example of Bangladesh. However, in others, it is continuously on the verge of turmoil, as in Mexico or in India, or remains marginal, as in Germany. How can such disparities be explained? Perhaps the countries that implement microfinance most successfully can teach us something. Microfinance is defined by J. Murdoch, one of the main contributors to the evaluation of its impact since its inception, as an activity with the purpose of «serving clients that have been excluded from the formal banking sector». This initiative stems from the idea that «much poverty can be alleviated - and that economic and social structures can be transformed fundamentally - by providing financial services to low-income households» 6. The target of microfinance is therefore vulnerable and marginalized populations, with an independent, informal, or sometimes inexistent economic activity. The financial services offered are mainly in the form of microcredits, micro-savings, and micro-insurance. They are provided by Microfinance Institutions (MFIs) of various types, such as commercial banks, non-governmental organizations (NGOs) or cooperatives. 2 Muhammad Yunus is a Bangladeshi researcher who founded modern microfinance. Nicknamed `the banker of the poor', he received the Nobel Peace Prize in 2006. 3 In October 2010, in the Andhra Pradesh province of India, thousands of over-indebted microcredit customers revolted against the pressure applied by the microcredit agents of Microfinance Institutions. The repayment rate collapsed and many institutions went bankrupt. 4 World Bank Group. The Global Findex Database 2017 (Global Findex). (2017). 5 The French researcher Esther Duflo and the Americans Abhijit Banerjee and Michael Kremer were rewarded in 2019 with the Nobel Prizes in Economic Sciences for their work on the «reduction of global poverty». Among other assertions, they state that the current practices of microfinance are not as efficient as critics claim. 6 Murdoch, J. The Microfinance Promise. Journal of Economic Literature. Vol. XXXVII, p1569?1614. (1999). 5 While its goals can vary from one place to another, they always consist essentially of the development of financial inclusion to reduce the vulnerability of precarious populations and eventually help them out of poverty. More specifically, there is both a social dimension and an economic dimension to microfinance, distinguishing it from the activity of most money lenders. The social dimension is intended to enable vulnerable populations to cover their basic needs and offer them relevant practical support. The economic dimension seeks to sustain the local economy by creating jobs and wealth. In addition, the activity is intended to be sustainable by providing financial and material resources to the MFIs through their revenues and their regulatory environment. Even though microfinance practices have existed in the past, Muhammad Yunus is considered to be the father of modern microfinance. His creativity and persistence were key to the success of the sector in the country and to its international expansion. In 1976, M. Yunus took it upon himself to use his own finances to offer small loans to the villages in his community. In view of the repeatedly favorable outcomes, in 1983 he decided to create the Grameen Bank, the 'village bank'. The initiative soon won praise and the popularity of microfinance grew swiftly: 2005 was named the year of microfinance by the UN and M. Yunus received the Nobel Peace Prize in 2006. The sector is now internationally recognized as a means of reaching the global sustainability objectives as defined by the UN and is explicitly mentioned in seven of the Social Development Goals (see Appendix 2). In spite of this worldwide recognition, microfinance has experienced multiple setbacks in its history. It can be divided into several phases. After a period of skepticism and obstacles that ran until the beginning of the 1980s, the sector entered a phase of broad acclamation and rapid expansion peaking in the 2000s. This rapid development worked against it and resulted in numerous scandals and disillusionments from the beginning of the 2010s, with the most significant being the Andhra Pradesh crisis in India. Microfinance then entered a phase of recovery with slower, more regulated and more controlled growth, at both local and global level. Therefore, the hope is that microfinance has now become of age. This maturity is an opportunity for us to examine the different levels of success of its practices around the world. The studies, which have proliferated rapidly, indicate unquestionably 6 that we have passed the time of blind enthusiasm of the early days. However, there are two countries in particular that, even with imperfections, have been able to avoid criticism and thrive. Bangladesh is an obvious first example. Birthplace of microfinance, worldwide source of inspiration, the country is second in terms of number of borrowers after India, amounting to 32 million in 20197. Financial inclusion is more advanced than in the vast majority of low-income countries, reaching (directly or through households) 50% of the population, despite 70% living in rural areas8. Bangladesh was relatively unaffected by the 2010 crisis due to the foresight of its MFIs in light of the rapid growth of the sector. Microfinance in France stems directly from the Bangladeshi success. Inspired by the achievements of M. Yunus after working closely with him, Maria Nowak introduced his methods to Europe. When she created the Association for the Right to Economic Initiative (in French Association pour le Droit à l'Initiative Economique, Adie) in 1989, the continent was still very skeptical. However, with time, France became a model itself, spearheading the creation of the European Microfinance Network in 2003, and it still contributes to the drafting of White Papers. With 244 000 microcredits distributed in 20189, France is the leading European country in the sector. It has also proven itself to be efficient: every euro invested generates €2.38 in revenues, stemming from the reduction in social benefits payments and from tax and social revenues10. Research questions The purpose of this thesis is to understand how these two highly contrasting countries have managed to successfully implement the same mechanism. The reflection is based on the assumption that the key to this success is adaptation to the local context. The fact that France was inspired directly by Bangladesh provides us with a favorable foundation to study how a country can efficiently shape the sector corresponding to its environment. 7 Wing, L. A. FinTech - Creating New Opportunities for MFIs in Bangladesh. DATABD.CO. (2019, 24 juilletJuly). 8 UN DESA, Government of the People's Republic of Bangladesh. Financial Inclusion in Bangladesh, A Concept Note. (2018). 9 Microfinance Barometer 2019. 10 KPMG & Adie. L'impact économique de l'action de l'Adie. (2016). 7 In their book The Triangle of Microfinance: Financial Sustainability, Outreach, and Impact, M. Zeller and R. L. Meyer represent microfinance in a schematic figure comprising two circles. The inner circle represents the MFIs, while the outer circle represents the environment of microfinance, which affects the sector's ability to pursue its objectives. The critical triangle in achieving economic sustainability of microfinance

Source: Zeller, M., & Meyer, R. L. The Triangle of Microfinance: Financial Sustainability, Outreach, and Impact. International Food Policy Research Institute. p6. (2003). The two researchers state the components of this environment «are mainly the policy framework, both macroeconomic and sectoral, and the socioeconomic, agroecological, and political conditions influencing the performance of financial institutions». In light of this analysis, this thesis considers that the local context comprises the economic and financial, political and regulatory and socio-cultural factors that are applicable to each of these two countries. My decision to write a thesis about this subject stems naturally from the interest I have had in the sector for several years and from my conviction that it can be an efficient tool in fighting poverty. Despite its flaws and insufficiencies, microfinance has started to structure itself internationally only recently. Its potential for progress is tremendous and deserves a close examination. 8 Methodology The methodology of this thesis is based on:

The areas of research of this thesis are France and Bangladesh, from the emergence of microfinance in the modern sense and directed to the local population in these countries, until 2019. The economic crisis resulting from Covid-19, like many other major crises, hit impoverished populations the most, caused a lasting increase in the already considerable inequalities, and largely wrote-off the achievements of the last decades. Therefore, microfinance has undergone significant changes since the beginning of 2020. With the aim of focusing on the problematic of this thesis and as it is impossible to currently predict the future of the sector, this analysis will be based on the data available before the beginning of this crisis. This paper is organized as follows. Firstly, a literature review will enable an overview of existing knowledge. Then, Section I surveys the reasons for the implementation of microfinance in Bangladesh and in France, and how it developed. Section II examines in detail the parameters that the sector needs to consider in both of these countries. Finally, Section III establishes the reasons 9 for microfinance's success in adapting to these factors, while underlining the improvements that can still be made. Summary of the literature review With Bangladesh and France being so different, the available literature on the use of microfinance in each country is very different. In Bangladesh, as in other low-income countries, it is particularly hard to isolate the impact of microfinance activities and collect data on the beneficiaries. While various studies started being published through the 1980s, the first to be established as a reference was that of Pitt and Khandker in 199811. It was followed seven years later by a paper by Khandker that studied the same groups of individuals to identify long-term effects12. Both demonstrate a positive impact on revenues. However, as microfinance became more well-known and Randomized Control Trials (RCTs) 13 became the norm, several researchers challenged their findings. Morduch and Roodman are the best-known critics of Pitt and Khandker and of microfinance benefits in general14. The studies multiplied with the growth and the setbacks of microfinance so much so that it is hard to draw general conclusions. However, Bhuiya, Khanam and Rahman15 provide us with an overview of the literature from the 1980s to 201316. Overall, the vast majority of the studies are in favor of a positive impact of microfinance and very few of the critics are thorough and unbiased. However, from 2010, the difficulties in the sector are undeniable. To understand their causes and identify levers for 11 Khandker, S. R., & Pitt, M. M. The Impact of Group-Based Credit Programs on Poor Households in Bangladesh: Does the Gender of Participants Matter? (1998). 12 Khandker, S. R. Microfinance and Poverty: Evidence Using Panel Data from Bangladesh. The World Bank Economic Review. (2005) 13 First developed in the medical field, this scientific method consists of randomly allocating participants to the treatment group (here, the group that participates in the studied microfinance programs) or the control group. This method has been largely adopted because of its efficiency in reducing selection bias and allocation bias. 14 Morduch, J. & Roodman, D. The Impact of Microcredit on the Poor in Bangladesh: Revisiting the Evidence. Center for Global Development. (2009). 15 Bhuiya, M. M. M., Khanam, R., & Rahman, M. M. Microfinance Operations in Bangladesh. An Overview. Journal of Applied Business and Economics Vol. 18(3). (2016). 16 See table p. 75. Bhuiya uses the same table in his paper. 10 improvement, S. Rutherford and S. K. Sinha interviewed 43 beneficiaries in the field17 for the CGAP18. They throw light on the need to control and standardize MFIs' branch practices. As for France, the literature is of a very different nature. The available data on beneficiaries and their activities is remarkably precise. Therefore, there are extensive reports presenting information about microfinance and recommendations for the future. The Observatoire de l'Inclusion Bancaire (Observatory of Financial Inclusion) is a significant source. However, it is important to keep sight of the social vision of microfinance in France, embodied by its founder, Maria Nowak. The creator of Adie wrote L'Espoir Economique (The Economic Hope), a very valuable book for understanding this vision, backed by the narrative of individuals who benefited from microcredits and were able to regain dignity. The reality of microfinance, its context and its purpose are very different in low- and in high-income countries. This disparity is reflected in the literature. It is very rich but lacks transversal analyses to provide internationally applicable recommendations. Furthermore, although numerous studies on the development and impact of microfinance in different countries around the world exist, they seldom describe in detail the importance of the local particularities. In this thesis, we describe thoroughly the local context of Bangladesh and France to identify recommendations applicable everywhere and others that are location-specific. Summary of the findings and implications The study of microfinance in Bangladesh and in France enables us to discern practices that are essential for microfinance to operate efficiently and which are relevant regardless of the location: Proceed in several steps. Start by ensuring that the context is well-understood and by assessing local potential through market and feasibility studies. Then, gradually adapt supply to demand: initially introduce a standard product that has proved to be efficient elsewhere, before increasingly 17 Sinha, S. K. & Rutherford, S. Household Interviews in Bangladesh, 2013. CGAP Focus Note 87 « A Microcredit Crisis Averted : The Case of Bangladesh ». CGAP. (2013). 18 The CGAP is a think tank gathering different kinds of organizations that aim at developing financial services for marginalized populations. It regularly publishes recommendations for MFIs and investors, backed by research and experiments. 11 offering various products and declinations. Progressively gain independence from outside sources of inspiration. Preserve the social vocation. Prevent the activity from drifting towards profit seeking. Be present in the field and in touch with customers to understand their needs and fulfil microfinance's social objectives. Transform the environment. Strive to have an impact on regulations and the financial sector to create an advantageous context and a dynamic of support for microfinance activities. This task benefits greatly from being carried out by a strong and forward-thinking leader capable of achieving these developments. Call these practices into question and improve them continually. Be constantly aware of the changes in the local context and regulations to protect customers and employees. Perform systematic satisfaction and impact surveys. Invest in new technical capacities. However, this exercise has also demonstrated the advantageous characteristics both of these countries enjoy individually, which cannot necessarily be reproduced elsewhere. In Bangladesh, the high population density, relatively uniform across the country, the uniformity of cultural practices and the strong sense of community across villages constitute a convenient context for the rapid expansion of microfinance. In France, the political stability, the pre-existing regulatory framework, the availability of public funding, the presence of complementary organizations, coupled with the broad access to health and education, enabled the creation of MFIs that concentrate exclusively on their social impact goal. Without an initial advantageous context, governments and private actors need all the more to apply the aforementioned knowledgeable recommendations. Préface La microfinance est un des exemples d'innovation inversée les plus réussis : née de la détermination d'un professeur d'université dans la campagne bangladaise et de son expérimentation sur quarante-deux femmes d'un petit village, elle est aujourd'hui reconnue par les plus grandes puissances économiques comme un outil efficace de lutte contre la pauvreté dans tous types de pays. Avec une croissance autour de 20% dans les années 2000 et 7% dans les années 2010, elle compte 139,9 millions d`emprunteurs à travers le monde en 201819. Cependant, si la microfinance est utilisée dans tant de pays, elle évolue de fait dans des contextes très différents et se concrétise dans des formes variées. Ce n'est pas un phénomène unique, mais pluriel, qui ne connaît pas le même succès partout. Le Bangladesh, berceau de la microfinance, et la France, pionnière en Europe, sont internationalement reconnus comme des sources d'inspiration dans le domaine. Bien qu'exécutée de manière très différente dans ces deux pays, la capacité de la microfinance à analyser, innover, s'adapter et se faire confiance lui a permis de mettre en place des pratiques efficaces aux effets tangibles. Dans ce mémoire, nous étudions en détail le chemin qu'une certaine idée de la lutte contre la pauvreté a parcouru dans des environnements on ne peut plus éloignés, pour tenter d'en tirer des recommandations pour un secteur qui doit encore faire ses preuves. 12 19 Baromètre de la Microfinance 2019. 13 Remerciements Je tiens à témoigner toute ma reconnaissance à ma tutrice, Madame Moret, Directrice de la communication externe, des partenariats et de la documentation chez Crédit Coopératif et intervenante à HEC Paris sur le domaine de la microfinance dans le cadre du certificat Inclusive and Social Business, dont l'expérience, les connaissances et l'enthousiasme ont été une source d'inspiration et de soutien essentielle à la rédaction de ce mémoire. J'adresse mes sincères remerciements aux professionnels de la microfinance qui ont accepté de répondre à mes questions et ont grandement contribué à mon travail de recherche. Tout particulièrement, je voudrais exprimer ma reconnaissance à Madame Nowak, fondatrice de la microfinance en France et en Europe, créatrice de l'Adie, auteure talentueuse, personnalité captivante qui a inspiré des milliers de personnes à travers le monde à avoir un impact positif sur leur environnement. Je remercie également Madame Rosado, Directrice générale adjointe de l'Adie, et Monsieur Hailey, Head of Impact chez ResponsAbility, dont l'expérience professionnelle ont été d'une aide précieuse. Enfin, je tiens à remercier mes parents, en particulier ma mère, dont le soutien, l'optimisme et la confiance qu'elle me témoigne m'ont portée tout au long de mes études, et encore jusque dans la rédaction de ce dernier travail, qui a pour moi une importance toute particulière. 14 Table des matières Abstract 3 Executive Summary 4 Préface 12 Remerciements 13 Introduction 16 Revue Littéraire 21 I. De la création de la microfinance au Bangladesh à son exportation en France, un même mécanisme pour répondre à différents types de pauvreté 24 A. Les facteurs qui justifient la mise en place de la microfinance dans chacun des deux pays 24

B. La naissance de la microfinance au Bangladesh portée par Muhammad Yunus 29

C. L'exportation de la microfinance en France insufflée par Maria Nowak 37

II. Deux pays aux réalités locales très différentes : vue d'ensemble des paramètres qui affectent la microfinance 43 A. Les facteurs économiques et financiers 43

B. Les facteurs politiques et réglementaires 52

15 C. Les facteurs socioculturels 56

III. Se réinventer pour assurer l'efficacité de la microfinance : bonnes pratiques et mesures d'impact 63 A. Le Bangladesh, un modèle mouvant 63

B. La France, un élève qui a trouvé ses marques 85

C. La microfinance dans ces deux pays peut encore connaître des améliorations 106

Conclusion 113 Entretien avec Maria Nowak - 13/01/2021 117 Entretien avec Alice Rosado - 04/02/2021 125 Entretien avec Paul Hailey - 05/01/2021 133 Références 141 Annexes 147 16 |

|