CONCLUSION

En définitive, nos analyses ont porté dans un

premier temps, sur la description de l'évolution des séries,

ensuite sur l'étude de leur saisonnalité et leur

stationnarité. Enfin, nous avons procédé à une

modélisation ARIMA des séries de l'IHPC et à l'analyse des

chocs.

De ce travail, il ressort que :

- toutes les séries sont non saisonnières ;

- des douze séries, seules les fonctions deux, cinq,

onze et douze sont stationnaires en différence première ; toutes

les autres sont stationnaires en niveau.

- la série FCT1 est un processus ARMA(6,7) ; les

séries D(FCT2), FCT7, D(FCT11) sont des processus ARMA(2,12) ; les

séries FCT3 et FCT4 sont des processus ARMA(4, 12) ; les séries

D(FCT5), FCT8 sont respectivement des MA(12) et MA(13) ; la série FCT6

est un processus ARMA(2, 13) ; la série FCT9 est un processus ARMA(6,

10) enfin, les séries FCT10 et D(FCT12) sont des processus

ARMA(1,12).

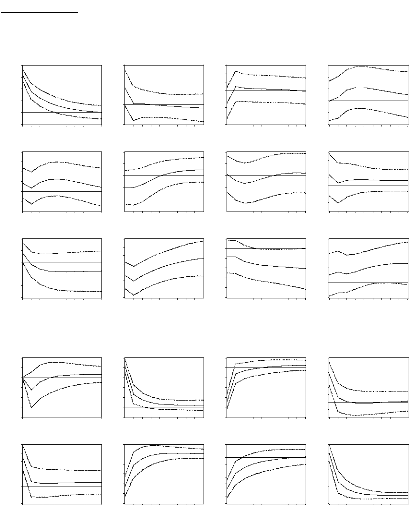

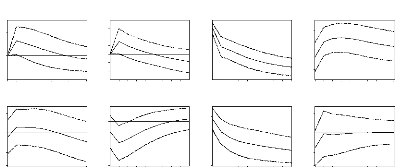

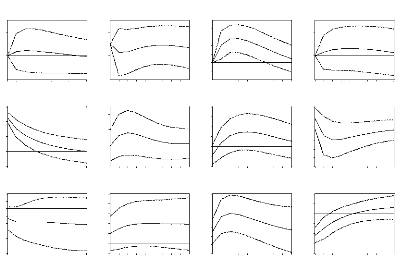

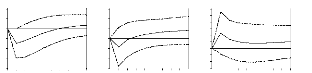

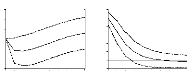

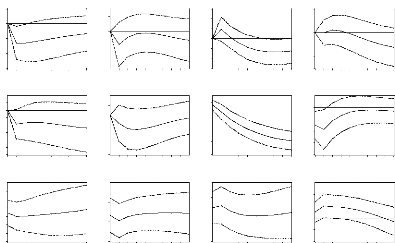

- un choc sur l'une des douze fonctions affecte les autres

fonctions puis l'indice global des prix.

Plusieurs extensions de ce travail sont envisageables. En

effet, cette modélisation des indices de prix sectoriels pourrait, par

exemple, être complétée par des prévisions afin de

permettre aux décideurs de mieux mener les politiques

anti-inflationnistes.

BIBLIOGRAPHIE

· BEFFY P., MONFORT B. et al, 2003 << L'apport d'un

modèle macroéconométrique pour l' analyse conjoncturelle

>>, Insee.

· BOURBONNAIS R. ; TERRAZA M. ,1998 - << Analyse des

séries temporelles en économie >>, Presses universitaires

de France, Paris.

· BOURBONNAIS (R.), 2000, «Econométrie»,

3ième édition. Paris, Dunod.

· DOE L. et DIARISSO S., 1996, << Une analyse

empirique de l'inflation en Côte d'Ivoire >> in Notes

d'Information et Statistiques N° 465- Août/Décembre 1996.

Dakar, BCEAO.

· DOSSOU A., 2000, << Guide pratique de

l'économétrie des séries temporelles >>, Dakar,

BCEAO.

· HURLIN C., 2001 << Econométrie

appliquée, séries temporelles>>, Université Paris IX

Dauphine.

· JOHNSTON J ; DINARDO J. , 1999 << Méthodes

économétriques >>, 4ième édition.

Paris, Jouve

· JONDEAU E., Le BIHAN H. et SEDILLOT F., 1999 <<

Modélisation et prévision des indices de prix sectoriels >>

Banque de France.

· KOULIBALI B.I., 2001 << Prévision à

court terme de l'inflation en Côte d'Ivoire >> Rapport de stage,

Ensea, Abidjan.

· LAWSON Z. L. D. ; MOSSO R., 2001 << Elaboration

d'un tableau de bord conjoncturel de l'indice des prix à la consommation

au Togo >>, Mémoire d'Analyse conjoncturelle, Ensea, Abidjan.

· PERRAUDIN C., 2002 << Séries

chronologiques >>, Université Paris I.

A NNEXES

ANNEXE 1 : RESULTATS DES TESTS DE RACINE UNITAIRE

|

SERIES

|

ETAPE: A

|

ETAPE: B0

|

ETAPE: B1

|

ETAPE: C

|

ETAPE: D0

|

ETAPE: D1

|

ETAPE: E

|

CONCLUSION

|

|

FCT1

|

(-2.42) [-3.46];

donc (p = 0

|

(2.96) [6.57];

donc

(3, cp) = ( 0, 0)

|

|

(-2.20) [-2.90];

donc (p = 0

|

(2.49) [4.76];

donc

(i, cp) = ( 0, 0)

|

|

(-2.06) [-1.94]; donc (p ~ 0

|

FCT1 est un

processus:

I(0)

|

|

FCT2

|

(-3.08) [-3.46];

|

(4.76) [6.57];

|

|

(-2.21) [-2.90];

|

(2.43) [4.76];

|

|

(-1.50) [-1.94];

|

FCT2 possède

|

|

donc (p = 0

|

donc

|

|

donc (p = 0

|

donc

|

|

donc (p = 0

|

une racine

|

|

|

(3, cp) = ( 0, 0)

|

|

|

(i, cp) = ( 0, 0)

|

|

|

unitaire

|

|

D(FCT2)

|

(-5.03) [-3.47];

|

|

(0.14) [1.96];

|

(-5.08) [-2.90];

|

|

(0.10) [1.96];

|

(-5.12) [-1.94];

|

D(FCT2) est un

|

|

donc (p ~ 0

|

|

donc 3 = 0

|

donc (p ~0

|

|

donc i =0

|

donc (p ~ 0

|

processus:

|

|

|

|

|

|

|

|

|

I(0)

|

|

FCT3

|

(-3.37) [-3.46];

|

(5.84) [6.57];

|

|

(-3.17) [-2.90];

|

|

(1.90) [1.96];

|

(-2.50) [-1.94];

|

FCT3 est un

|

|

donc (p = 0

|

donc

|

|

donc (p ~0

|

|

donc i =0

|

donc (p ~ 0

|

processus:

|

|

|

(3, cp) = ( 0, 0)

|

|

|

|

|

|

I(0)

|

|

FCT4

|

(-2.77) [-3.46];

|

(3.82) [6.57];

|

|

(-2.75) [-2.90];

|

(3.89) [4.76];

|

|

(-2.22) [-1.94];

|

FCT4 est un

|

|

donc (p = 0

|

donc

|

|

donc (p = 0

|

donc

|

|

donc (p ~ 0

|

processus:

|

|

|

(3, cp) = ( 0, 0)

|

|

|

(i, cp) = ( 0, 0)

|

|

|

I(0)

|

|

FCT5

|

(-2.20) [-3.46];

|

(2.74) [6.57];

|

|

(-1.56) [-2.90];

|

(1.39) [4.76];

|

|

(-1.48) [-1.94];

|

FCT5 possède

|

|

donc (p = 0

|

donc

|

|

donc (p = 0

|

donc

|

|

donc (p = 0

|

une racine

|

|

|

(3, cp) = ( 0, 0)

|

|

|

(i, cp) = ( 0, 0)

|

|

|

unitaire

|

|

D(FCT5)

|

(-3.83) [-3.47];

|

|

(0.51) [1.96];

|

(-3.82) [-2.90];

|

|

(0.57) [1.96];

|

(-3.80) [-1.94];

|

D(FCT5) est un

|

|

donc (p ~ 0

|

|

donc 3 = 0

|

donc (p ~0

|

|

donc i =0

|

donc (p ~ 0

|

processus:

|

|

|

|

|

|

|

|

|

I(0)

|

|

FCT6

|

(-3.00) [-3.46];

|

(4.52) [6.57];

|

|

(-2.88) [-2.90];

|

(4.16) [4.76];

|

|

(-2.00) [-1.94];

|

FCT6 est un

|

|

donc (p = 0

|

donc

|

|

donc (p = 0

|

donc

|

|

donc (p ~ 0

|

processus:

|

|

|

(3, cp) = ( 0, 0)

|

|

|

(i, cp) = ( 0, 0)

|

|

|

I(0)

|

|

FCT7

|

(-2.32) [-3.46];

|

(2.80) [6.57];

|

|

(-2.36) [-2.90];

|

(2.81) [4.76];

|

|

(-1.95) [-1.94];

|

FCT7 est un

|

|

donc (p = 0

|

donc

|

|

donc (p = 0

|

donc

|

|

donc (p ~ 0

|

processus:

|

|

|

(3, cp) = ( 0, 0)

|

|

|

(i, cp) = ( 0, 0)

|

|

|

I(0)

|

|

FCT8

|

(-3.19) [-3.46];

|

(5.16) [6.57];

|

|

(-3.21) [-2.90];

|

|

(0.01) [1.96];

|

(-3.23) [-1.94];

|

FCT8 est un

|

|

donc (p = 0

|

donc

|

|

donc (p ~0

|

|

donc i =0

|

donc (p ~ 0

|

processus:

|

|

|

(3, cp) = ( 0, 0)

|

|

|

|

|

|

I(0)

|

NOTE : les valeurs entre parenthèses

désignent les valeurs empiriques obtenues tandis que celles entre

crochets sont celles tabulées.

RESULTATS DES TESTS DE RACINE UNITAIRE (suite)

|

SERIES

|

ETAPE: A

|

ETAPE: B0

|

ETAPE: B1

|

ETAPE: C

|

ETAPE: D0

|

ETAPE: D1

|

ETAPE: E

|

CONCLUSION

|

|

FCT9

|

(-3.36) [-3.46];

donc (p = 0

|

(5.68) [6.57];

donc

(3, cp) = ( 0, 0)

|

|

(-3.15) [-2.90];

donc (p ~0

|

|

(1.69) [1.96];

donc t =0

|

(-2.63) [-1.94]; donc (p ~ 0

|

FCT9 est un

processus:

I(0)

|

|

FCT10

|

(-2.25) [-3.46];

|

(2.64) [6.57];

|

|

(-2.29) [-2.90];

|

(2.63) [4.76];

|

|

(-1.96) [-1.94];

|

FCT10 est un

|

|

donc (p = 0

|

donc

|

|

donc (p = 0

|

donc

|

|

donc (p ~ 0

|

processus:

|

|

|

(3, cp) = ( 0, 0)

|

|

|

(t, cp) = ( 0, 0)

|

|

|

I(0)

|

|

FCT11

|

(-1.05) [-3.46];

|

(1.14) [6.57];

|

|

(-1.27) [-2.90];

|

(0.96) [4.76];

|

|

(-0.73) [-1.94];

|

FCT11 possède

|

|

donc (p = 0

|

donc

|

|

donc (p = 0

|

donc

|

|

donc (p = 0

|

une racine

|

|

|

(3, cp) = ( 0, 0)

|

|

|

(t, cp) = ( 0, 0)

|

|

|

unitaire

|

|

D(FCT11)

|

(-3.98) [-3.47];

|

|

(0.83) [1.96];

|

(-3.93) [-2.90];

|

|

(0.40) [1.96];

|

(-3.94) [-1.94];

|

D(FCT11) est

|

|

donc (p ~ 0

|

|

donc 3 = 0

|

donc (p ~0

|

|

donc t =0

|

donc (p ~ 0

|

un processus:

|

|

|

|

|

|

|

|

|

I(0)

|

|

FCT12

|

(-1.81) [-3.46];

|

(1.93) [6.57];

|

|

(-1.66) [-2.90];

|

(1.42) [4.76];

|

|

(-1.65) [-1.94];

|

FCT12 possède

|

|

donc (p = 0

|

donc

|

|

donc (p = 0

|

donc

|

|

donc (p = 0

|

une racine

|

|

|

(3, cp) = ( 0, 0)

|

|

|

(t, cp) = ( 0, 0)

|

|

|

unitaire

|

|

D(FCT12)

|

(-4.49) [-3.47];

|

|

(0.71) [1.96];

|

(-4.46) [-2.90];

|

|

(0.33) [1.96];

|

(-4.48) [-1.94];

|

D(FCT12) est

|

|

donc (p ~ 0

|

|

donc 3 = 0

|

donc (p ~0

|

|

donc t =0

|

donc (p ~ 0

|

un processus:

|

|

|

|

|

|

|

|

|

I(0)

|

NOTE : les valeurs entre parenthèses

désignent les valeurs empiriques obtenues tandis que celles entre

crochets sont celles tabulées.

ANNEXE2

FONCTION 1

Résultats de l' estimation

Dependent Variable: FCT1

Method: Least Squares

Date: 01/02/01 Time: 18:44

Sample(adjusted): 1997:07 2004:04

Included observations: 82 after adjusting endpoints Convergence

achieved after 15 iterations

Backcast: 1996:12 1997:06

|

Variable

|

Coefficient

|

Std. Error t-Statistic

|

Prob.

|

|

AR(2)

|

0.526398

|

0.106895 4.924451

|

0.0000

|

|

AR(6)

|

-0.347065

|

0.09673 1 -3.587920

|

0.0006

|

|

MA(7)

|

0.783637

|

0.059902 13.08207

|

0.0000

|

MA(1)

|

0.786420

|

0.063801 12.32620

|

0.0000

|

MA(2)

|

|

-0.159231

|

0.069363 -2.295618

|

0.0245

|

|

|

MA(6)

|

0.763688

|

0.058269 13.10634

|

0.0000

|

|

R-squared

|

0.604926

|

Mean dependent var

|

2.077448

|

|

Adjusted R-squared

|

0.578935

|

S.D. dependent var

|

4.71 4668

|

|

S.E. of regression

|

3.059326

|

Akaike info criterion

|

5.144622

|

|

Sum squared resid

|

711.3202

|

Schwarz criterion

|

5.320723

|

|

Log likelihood

|

-204.9295

|

Durbin-Watson stat

|

1.976965

|

Corrélogramme des résidus

Date: 01/02/01 Time: 18:47 Sample: 1997:07 2004:04 Included

observations: 82

Q-statistic

probabilities

adjusted for 6

ARMA term(s)

|

Autocorrelation

|

Partial Correlation

|

|

AC

|

PAC

|

Q-Stat

|

Prob

|

|

. | . |

|

. | . |

|

1

|

-0.032

|

-0.032

|

0.0862

|

|

|

. | . |

|

. | . |

|

2

|

-0.004

|

-0.005

|

0.0877

|

|

|

.*| . |

|

.*| . |

|

3

|

-0.072

|

-0.073

|

0.5436

|

|

|

. | . |

|

. | . |

|

4

|

0.064

|

0.060

|

0.9066

|

|

|

. |*. |

|

. |*. |

|

5

|

0.102

|

0.106

|

1.8358

|

|

|

.*| . |

|

.*| . |

|

6

|

-0.111

|

-0.111

|

2.9442

|

|

|

. | .

|

|

|

. | .

|

|

|

7

|

0.043

|

0.047

|

3.1102

|

0.078

|

|

. |*.

|

|

|

. |*.

|

|

|

8

|

0.089

|

0.107

|

3.8540

|

0.146

|

|

. | .

|

|

|

. | .

|

|

|

9

|

-0.006

|

-0.033

|

3.8569

|

0.277

|

|

. |*.

|

|

|

. |*.

|

|

|

10

|

0.106

|

0.120

|

4.9418

|

0.293

|

|

. | .

|

|

|

. | .

|

|

|

11

|

-0.052

|

-0.015

|

5.2081

|

0.391

|

|

**| .

|

|

|

**| .

|

|

|

12

|

-0.201

|

-0.258

|

9.1885

|

0.163

|

|

. | .

|

|

|

. | .

|

|

|

13

|

-0.027

|

-0.021

|

9.2595

|

0.235

|

|

. |*.

|

|

|

. |*.

|

|

|

14

|

0.106

|

0.131

|

10.393

|

0.239

|

|

. | .

|

|

|

. | .

|

|

|

15

|

0.044

|

-0.032

|

10.592

|

0.305

|

FONCTION 2

Résultats de l' estimation de D(FCT2)

Dependent Variable: D(FCT2)

Method: Least Squares

Date: 01/04/01 Time: 09:17

Sample(adjusted): 1997:04 2004:04

Included observations: 85 after adjusting endpoints Convergence

achieved after 7 iterations

Backcast: 1996:04 1997:03

|

Variable

|

Coefficient

|

Std. Error t-Statistic

|

Prob.

|

AR(1)

|

-0.224272

|

0.105344 -2.128940

|

0.0363

|

AR(2)

|

|

-0.299668

|

0.105441 -2.842036

|

0.0057

|

|

|

MA(12)

|

-0.961850

|

0.032031 -30.02836

|

0.0000

|

|

R-squared

|

0.551 955

|

Mean dependent var

|

0.004121

|

|

Adjusted R-squared

|

0.541 027

|

S.D. dependent var

|

5.167560

|

|

S.E. of regression

|

3.500893

|

Akaike info criterion

|

5.378570

|

|

Sum squared resid

|

1005.013

|

Schwarz criterion

|

5.46478 1

|

|

Log likelihood

|

-225.5892

|

Durbin-Watson stat

|

2.069955

|

Corrélogramme des résidus

Date: 01/04/01 Time: 09:20 Sample: 1997:04 2004:04 Included

observations: 85

Q-statistic

probabilities

adjusted for 3

ARMA term(s)

|

Autocorrelation

|

Partial Correlation

|

|

AC

|

PAC

|

Q-Stat

|

Prob

|

|

. | . |

|

. | . |

|

1

|

-0.035

|

-0.035

|

0.1078

|

|

|

.*| . |

|

.*| . |

|

2

|

-0.059

|

-0.061

|

0.4229

|

|

|

.*| . |

|

.*| . |

|

3

|

-0.152

|

-0.158

|

2.5184

|

|

|

.*| . |

|

.*| . |

|

4

|

-0.136

|

-0.157

|

4.1967

|

0.041

|

|

.

|

| .

|

|

|

.*| .

|

|

|

5

|

-0.036

|

-0.077

|

4.3165

|

0.116

|

|

.

|

| .

|

|

|

.*| .

|

|

|

6

|

-0.053

|

-0.114

|

4.5828

|

0.205

|

|

.

|

|*.

|

|

|

. | .

|

|

|

7

|

0.069

|

-0.002

|

5.0283

|

0.284

|

|

.

|

| .

|

|

|

. | .

|

|

|

8

|

0.037

|

-0.013

|

5.1623

|

0.396

|

|

.

|

|*.

|

|

|

. | .

|

|

|

9

|

0.090

|

0.058

|

5.9471

|

0.429

|

|

.

|

| .

|

|

|

. | .

|

|

|

10

|

-0.028

|

-0.029

|

6.0246

|

0.537

|

|

.

|

| .

|

|

|

. |*.

|

|

|

11

|

0.054

|

0.078

|

6.3131

|

0.612

|

|

.

|

| .

|

|

|

. | .

|

|

|

12

|

-0.038

|

-0.002

|

6.4605

|

0.693

|

|

.

|

| .

|

|

|

. | .

|

|

|

13

|

-0.023

|

0.011

|

6.5163

|

0.770

|

|

.

|

| .

|

|

|

. | .

|

|

|

14

|

0.000

|

0.022

|

6.5163

|

0.837

|

|

.*| . |

|

.*| . |

|

15

|

-0.081

|

-0.064

|

7.2036

|

0.844

|

FONCTION 3

Résultats de l'estimation

Dependent Variable: FCT3

Method: Least Squares

Date: 01/02/01 Time: 18:57

Sample(adjusted): 1997:05 2004:04

Included observations: 84 after adjusting endpoints Convergence

achieved after 16 iterations

Backcast: OFF (Roots of MA process too large)

|

Variable

|

Coefficient

|

Std. Error t-Statistic

|

Prob.

|

|

AR(1)

|

0.882389

|

0.075637 11.66608

|

0.0000

|

|

AR(4)

|

0.192353

|

0.087266 2.204211

|

0.0304

|

|

MA(3)

|

-0.178984

|

0.026109 -6.855142

|

0.0000

|

|

MA(5)

|

-0.248313

|

0.028744 -8.638825

|

0.0000

|

|

MA(12)

|

-1.411857

|

0.039760 -35.50967

|

0.0000

|

|

R-squared

|

0.768835

|

Mean dependent var

|

1.475876

|

|

Adjusted R-squared

|

0.7571 30

|

S.D. dependent var

|

2.540909

|

|

S.E. of regression

|

1.252206

|

Akaike info criterion

|

3.345369

|

|

Sum squared resid

|

123.8736

|

Schwarz criterion

|

3.49006 1

|

|

Log likelihood

|

-135.5055

|

Durbin-Watson stat

|

2.141 441

|

Corrélogramme des résidus

Date: 01/02/01 Time: 18:58 Sample: 1997:05 2004:04 Included

observations: 84

Q-statistic

probabilities

adjusted for 5

ARMA term(s)

|

Autocorrelation

|

Partial Correlation

|

|

AC

|

PAC

|

Q-Stat

|

Prob

|

|

.*| .

|

|

|

.*| .

|

|

|

1

|

-0.100

|

-0.100

|

0.8681

|

|

|

. | .

|

|

|

. | .

|

|

|

2

|

-0.012

|

-0.022

|

0.8812

|

|

|

. |*.

|

|

|

. |*.

|

|

|

3

|

0.113

|

0.111

|

2.0278

|

|

|

. | .

|

|

|

. | .

|

|

|

4

|

-0.033

|

-0.011

|

2.1254

|

|

|

. | .

|

|

|

. | .

|

|

|

5

|

0.020

|

0.018

|

2.1606

|

|

|

.*| .

|

|

|

.*| .

|

|

|

6

|

-0.124

|

-0.137

|

3.5924

|

0.058

|

|

.*| .

|

|

|

**| .

|

|

|

7

|

-0.175

|

-0.203

|

6.4589

|

0.040

|

|

. | .

|

|

|

.*| .

|

|

|

8

|

-0.053

|

-0.109

|

6.7246

|

0.081

|

|

.*| .

|

|

|

**| .

|

|

|

9

|

-0.178

|

-0.189

|

9.7839

|

0.044

|

|

.*| .

|

|

|

.*| .

|

|

|

10

|

-0.115

|

-0.149

|

11.083

|

0.050

|

|

. | .

|

|

|

. | .

|

|

|

11

|

0.040

|

0.002

|

11.242

|

0.081

|

|

.*| .

|

|

|

.*| .

|

|

|

12

|

-0.170

|

-0.178

|

14.126

|

0.049

|

|

. | .

|

|

|

.*| .

|

|

|

13

|

-0.032

|

-0.143

|

14.230

|

0.076

|

|

. |*.

|

|

|

. | .

|

|

|

14

|

0.126

|

0.007

|

15.881

|

0.069

|

|

. | .

|

|

|

. | .

|

|

|

15

|

0.013

|

-0.046

|

15.899

|

0.103

|

FONCTION 4

Résultats de l'estimation

Dependent Variable: FCT4

Method: Least Squares

Date: 01/03/01 Time: 20:17

Sample(adjusted): 1997:05 2004:04

Included observations: 84 after adjusting endpoints Convergence

achieved after 17 iterations

Backcast: 1996:05 1997:04

|

Variable

|

Coefficient

|

Std. Error t-Statistic

|

Prob.

|

|

AR(1)

|

0.781817

|

0.077106 10.13956

|

0.0000

|

|

AR(4)

|

0.184428

|

0.076565 2.408765

|

0.0183

|

|

MA(2)

|

0.101348

|

1.49E-05 6785.698

|

0.0000

|

|

MA(12)

|

-0.901049

|

0.057188 -15.75586

|

0.0000

|

|

R-squared

|

0.81 71 24

|

Mean dependent var

|

4.301162

|

|

Adjusted R-squared

|

0.81 0266

|

S.D. dependent var

|

5.41 5988

|

|

S.E. of regression

|

2.359120

|

Akaike info criterion

|

4.600902

|

|

Sum squared resid

|

445.2357

|

Schwarz criterion

|

4.716655

|

|

Log likelihood

|

-189.2379

|

Durbin-Watson stat

|

1.969440

|

Corrélogramme des résidus

Date: 01/03/01 Time: 20:21 Sample: 1997:05 2004:04 Included

observations: 84

Q-statistic

probabilities

adjusted for 4

ARMA term(s)

|

Autocorrelation

|

Partial Correlation

|

AC

|

PAC

|

Q-Stat

|

Prob

|

|

. | .

|

|

|

. | . |

|

1

|

0.008

|

0.008

|

0.0058

|

|

|

. | .

|

|

|

. | . |

|

2

|

0.004

|

0.004

|

0.0070

|

|

|

. |*.

|

|

|

. |*.

|

| 3

|

0.090

|

0.089

|

0.7218

|

|

|

. |*.

|

|

|

. |*.

|

| 4

|

0.109

|

0.108

|

1.7868

|

|

|

.*| .

|

|

|

.*| .

|

| 5

|

-0.125

|

-0.129

|

3.2148

|

0.073

|

|

.*| .

|

|

|

.*| .

|

| 6

|

-0.152

|

-0.165

|

5.3577

|

0.069

|

|

. | .

|

|

|

. | . |

|

7

|

0.045

|

0.030

|

5.5486

|

0.136

|

|

.*| .

|

|

|

.*| .

|

| 8

|

-0.082

|

-0.068

|

6.1890

|

0.185

|

|

.*| .

|

|

|

.*| .

|

| 9

|

-0.114

|

-0.063

|

7.4426

|

0.190

|

|

. | .

|

|

|

. | . |

|

10

|

-0.023

|

-0.009

|

7.4962

|

0.277

|

|

. |*.

|

|

|

. |*.

|

| 11

|

0.151

|

0.131

|

9.7519

|

0.203

|

|

**| .

|

|

|

**| .

|

| 12

|

-0.196

|

-0.194

|

13.606

|

0.093

|

|

. | .

|

|

|

. |*.

|

| 13

|

0.051

|

0.069

|

13.869

|

0.127

|

|

**| .

|

|

|

**| .

|

| 14

|

-0.214

|

-0.310

|

18.611

|

0.045

|

|

. |*.

|

|

|

. |*.

|

| 15

|

0.117

|

0.146

|

20.047

|

0.045

|

|

. | .

|

|

|

. |*.

|

| 16

|

0.023

|

0.068

|

20.103

|

0.065

|

FONCTION 5

Résultats de l'estimation de D(FCT5)

Dependent Variable: D(FCT5)

Method: Least Squares

Date: 01/03/01 Time: 20:44

Sample(adjusted): 1997:02 2004:04

Included observations: 87 after adjusting endpoints Convergence

achieved after 8 iterations

Backcast: 1996:02 1997:01

|

Variable

|

Coefficient

|

Std. Error t-Statistic

|

Prob.

|

|

MA(12)

|

-0.900653

|

0.025626 -35.14619

|

0.0000

|

|

R-squared

|

0.51 6010

|

Mean dependent var

|

-0.050238

|

|

Adjusted R-squared

|

0.516010

|

S.D. dependent var

|

1.591118

|

|

S.E. of regression

|

1.106930

|

Akaike info criterion

|

3.052486

|

|

Sum squared resid

|

105.3753

|

Schwarz criterion

|

3.080830

|

|

Log likelihood

|

-131 .7831

|

Durbin-Watson stat

|

2.118074

|

Corrélogramme des résidus

Date: 01/03/01 Time: 20:46 Sample: 1997:02 2004:04 Included

observations: 87

Q-statistic

probabilities

adjusted for 1

ARMA term(s)

|

Autocorrelation Partial Correlation

|

|

AC

|

PAC

|

Q-Stat

|

Prob

|

|

.*| . | .*| . |

|

1

|

-0.066

|

-0.066

|

0.3944

|

|

|

.*| . | .*| . |

|

2

|

-0.155

|

-0.160

|

2.5752

|

0.109

|

|

. | . | . | . |

|

3

|

-0.004

|

-0.027

|

2.5763

|

0.276

|

|

.*| . | .*| . |

|

4

|

-0.131

|

-0.163

|

4.1844

|

0.242

|

|

. |*.

|

| . |*.

|

|

|

5

|

0.163

|

0.143

|

6.7081

|

0.152

|

|

. | .

|

| . | .

|

|

|

6

|

0.048

|

0.021

|

6.9245

|

0.226

|

|

. | .

|

| . | .

|

|

|

7

|

-0.032

|

0.024

|

7.0221

|

0.319

|

|

. | .

|

| . | .

|

|

|

8

|

0.026

|

0.022

|

7.0883

|

0.420

|

|

. | .

|

| . | .

|

|

|

9

|

-0.043

|

0.003

|

7.2686

|

0.508

|

|

. |*.

|

| . |*.

|

|

|

10

|

0.098

|

0.097

|

8.2357

|

0.511

|

|

. | .

|

| . | .

|

|

|

11

|

-0.014

|

-0.024

|

8.2570

|

0.604

|

|

**| .

|

| .*| .

|

|

|

12

|

-0.208

|

-0.187

|

12.736

|

0.311

|

|

. |*.

|

| . | .

|

|

|

13

|

0.094

|

0.056

|

13.664

|

0.323

|

|

.*| . | .*| . |

|

14

|

-0.067

|

-0.108

|

14.139

|

0.364

|

|

.*| . | .*| . |

|

15

|

-0.075

|

-0.107

|

14.749

|

0.396

|

FONCTION 6

Résultats de l'estimation

Dependent Variable: FCT6

Method: Least Squares

Date: 01/02/01 Time: 19:00

Sample(adjusted): 1997:03 2004:04

Included observations: 86 after adjusting endpoints Convergence

achieved after 19 iterations

Backcast: 1996:02 1997:02

|

Variable

|

Coefficient

|

Std. Error t-Statistic

|

Prob.

|

|

AR(2)

|

0.856004

|

0.065091 13.15097

|

0.0000

|

|

MA(1)

|

0.879789

|

0.060701 14.49371

|

0.0000

|

MA(12)

|

-0.860826

|

0.041276 -20.85554

|

0.0000

|

MA(13)

|

|

-0.777722

|

0.064986 -11.96746

|

0.0000

|

|

|

R-squared

|

0.649013

|

Mean dependent var

|

2.639979

|

|

Adjusted R-squared

|

0.636172

|

S.D. dependent var

|

3.583638

|

|

S.E. of regression

|

2.161586

|

Akaike info criterion

|

4.424957

|

|

Sum squared resid

|

383.1412

|

Schwarz criterion

|

4.539112

|

|

Log likelihood

|

-186.2731

|

Durbin-Watson stat

|

2.021177

|

Corrélogramme des résidus

Date: 01/02/01 Time: 19:01 Sample: 1997:03 2004:04 Included

observations: 86

Q-statistic

probabilities

adjusted for 4

ARMA term(s)

|

Autocorrelation

|

Partial Correlation

|

AC

|

PAC

|

Q-Stat

|

Prob

|

|

. | .

|

|

|

. | .

|

| 1

|

-0.053

|

-0.053

|

0.2525

|

|

|

.*| .

|

|

|

.*| .

|

| 2

|

-0.160

|

-0.163

|

2.5470

|

|

|

.*| .

|

|

|

.*| .

|

| 3

|

-0.138

|

-0.161

|

4.2795

|

|

|

. | .

|

|

|

.*| .

|

| 4

|

-0.024

|

-0.076

|

4.3318

|

|

|

. | .

|

|

|

. | .

|

| 5

|

0.020

|

-0.042

|

4.3682

|

0.037

|

|

. | .

|

|

|

. | .

|

| 6

|

0.051

|

0.010

|

4.6164

|

0.099

|

|

. | .

|

|

|

. | .

|

| 7

|

0.034

|

0.024

|

4.7280

|

0.193

|

|

. |*.

|

|

|

. |*.

|

| 8

|

0.129

|

0.151

|

6.3312

|

0.176

|

|

. | .

|

|

|

. | .

|

| 9

|

-0.052

|

-0.002

|

6.5961

|

0.252

|

|

. | .

|

|

|

. |*.

|

| 10

|

0.025

|

0.091

|

6.6565

|

0.354

|

|

.*| .

|

|

|

.*| .

|

| 11

|

-0.127

|

-0.089

|

8.2881

|

0.308

|

|

.*| .

|

|

|

.*| .

|

| 12

|

-0.159

|

-0.177

|

10.870

|

0.209

|

|

. |*.

|

|

|

. |*.

|

| 13

|

0.140

|

0.082

|

12.916

|

0.166

|

|

. | .

|

|

|

. | .

|

| 14

|

0.045

|

-0.044

|

13.125

|

0.217

|

|

. |*.

|

|

|

. |*.

|

| 15

|

0.152

|

0.150

|

15.589

|

0.157

|

FONCTION 7

Résultats de l' estimation

Dependent Variable: FCT7

Method: Least Squares

Date: 01/02/01 Time: 19:03

Sample(adjusted): 1997:03 2004:04

Included observations: 86 after adjusting endpoints Convergence

achieved after 9 iterations

Backcast: OFF (Roots of MA process too large)

|

Variable

|

Coefficient

|

Std. Error t-Statistic

|

Prob.

|

AR(1)

|

0.713313

|

0.107059 6.662815

|

0.0000

|

AR(2)

|

|

0.308715

|

0.109321 2.823934

|

0.0060

|

|

|

MA(2)

|

-0.233830

|

0.049015 -4.770594

|

0.0000

|

|

MA(12)

|

-1 .027328

|

0.057321 -17.92253

|

0.0000

|

|

R-squared

|

0.784563

|

Mean dependent var

|

7.842592

|

|

Adjusted R-squared

|

0.776681

|

S.D. dependent var

|

12.371 06

|

|

S.E. of regression

|

5.846143

|

Akaike info criterion

|

6.41 4837

|

|

Sum squared resid

|

2802.546

|

Schwarz criterion

|

6.528992

|

|

Log likelihood

|

-271.8380

|

Durbin-Watson stat

|

2.035167

|

Corrélogramme des résidus

Date: 01/02/01 Time: 19:05 Sample: 1997:03 2004:04 Included

observations: 86

Q-statistic

probabilities

adjusted for 4

ARMA term(s)

|

Autocorrelation

|

Partial Correlation

|

|

AC

|

PAC

|

Q-Stat

|

Prob

|

|

. | . |

|

. | .

|

|

|

1

|

-0.025

|

-0.025

|

0.0557

|

|

|

.*| . |

|

.*| .

|

|

|

2

|

-0.078

|

-0.079

|

0.6067

|

|

|

. | .

|

|

|

. | .

|

|

|

3

|

-0.004

|

-0.009

|

0.6085

|

|

|

. | .

|

|

|

. | .

|

|

|

4

|

-0.037

|

-0.044

|

0.7349

|

|

|

. | .

|

|

|

. | .

|

|

|

5

|

-0.036

|

-0.039

|

0.8544

|

0.355

|

|

. | .

|

|

|

.*| .

|

|

|

6

|

-0.056

|

-0.066

|

1.1530

|

0.562

|

|

. |*.

|

|

|

. |*.

|

|

|

7

|

0.084

|

0.075

|

1.8358

|

0.607

|

|

. | .

|

|

|

. | .

|

|

|

8

|

-0.007

|

-0.015

|

1.8399

|

0.765

|

|

. |*.

|

|

|

. |*.

|

|

|

9

|

0.154

|

0.166

|

4.1671

|

0.526

|

|

.*| . |

|

.*| .

|

|

|

10

|

-0.067

|

-0.070

|

4.6202

|

0.593

|

|

**| . |

|

.*| .

|

|

|

11

|

-0.206

|

-0.187

|

8.9091

|

0.259

|

|

. | . |

|

.*| .

|

|

|

12

|

-0.043

|

-0.067

|

9.0958

|

0.334

|

|

.*| . |

|

.*| .

|

|

|

13

|

-0.094

|

-0.117

|

10.019

|

0.349

|

|

. | . |

|

. | .

|

|

|

14

|

0.060

|

0.047

|

10.395

|

0.407

|

|

. | . |

|

. | .

|

|

|

15

|

-0.001

|

-0.011

|

10.395

|

0.495

|

FONCTION 8

Résultats de l'estimation

Dependent Variable: FCT8

Method: Least Squares

Date: 01/02/01 Time: 19:09

Sample: 1997:01 2004:04

Included observations: 88

Convergence achieved after 36 iterations Backcast: OFF (Roots of

MA process too large)

|

Variable

|

Coefficient

|

Std. Error t-Statistic

|

Prob.

|

|

MA(1)

|

0.851 390

|

0.057296 14.85960

|

0.0000

|

|

MA(3)

|

-0.283324

|

0.050397 -5.621835

|

0.0000

|

MA(12)

|

-0.877008

|

0.099816 -8.786242

|

0.0000

|

MA(13)

|

|

-0.811989

|

0.111085 -7.309635

|

0.0000

|

|

|

R-squared

|

0.639459

|

Mean dependent var

|

0.033082

|

|

Adjusted R-squared

|

0.626583

|

S.D. dependent var

|

2.5951 47

|

|

S.E. of regression

|

1.585839

|

Akaike info criterion

|

3.804494

|

|

Sum squared resid

|

211.2504

|

Schwarz criterion

|

3.917100

|

|

Log likelihood

|

-163.3977

|

Durbin-Watson stat

|

2.126999

|

Corrélogramme des résidus

Date: 01/02/01 Time: 19:10 Sample: 1997:01 2004:04 Included

observations: 88

Q-statistic

probabilities

adjusted for 4

ARMA term(s)

|

Autocorrelation

|

Partial Correlation

|

|

AC

|

PAC

|

Q-Stat

|

Prob

|

|

.*| .

|

|

|

.*| .

|

|

|

1

|

-0.092

|

-0.092

|

0.7771

|

|

|

. | .

|

|

|

. | .

|

|

|

2

|

0.052

|

0.044

|

1.0243

|

|

|

. |*.

|

|

|

. |*.

|

|

|

3

|

0.128

|

0.138

|

2.5588

|

|

|

.*| .

|

|

|

.*| .

|

|

|

4

|

-0.083

|

-0.062

|

3.2029

|

|

|

. | .

|

|

|

. | .

|

|

|

5

|

0.007

|

-0.021

|

3.2074

|

0.073

|

|

. | .

|

|

|

. | .

|

|

|

6

|

0.030

|

0.021

|

3.2957

|

0.192

|

|

.*| .

|

|

|

.*| .

|

|

|

7

|

-0.122

|

-0.101

|

4.7552

|

0.191

|

|

. |*.

|

|

|

. | .

|

|

|

8

|

0.087

|

0.064

|

5.5042

|

0.239

|

|

.*| .

|

|

|

. | .

|

|

|

9

|

-0.061

|

-0.044

|

5.8779

|

0.318

|

|

. | .

|

|

|

. | .

|

|

|

10

|

-0.050

|

-0.039

|

6.1320

|

0.409

|

|

. | .

|

|

|

. | .

|

|

|

11

|

0.057

|

0.026

|

6.4703

|

0.486

|

|

.*| .

|

|

|

. | .

|

|

|

12

|

-0.085

|

-0.056

|

7.2167

|

0.513

|

|

. | .

|

|

|

. | .

|

|

|

13

|

0.046

|

0.043

|

7.4411

|

0.591

|

|

. | .

|

|

|

. | .

|

|

|

14

|

0.016

|

0.001

|

7.4683

|

0.681

|

|

. | .

|

|

|

. |*.

|

|

|

15

|

0.042

|

0.079

|

7.6571

|

0.744

|

FONCTION 9

Résultats de l'estimation

Dependent Variable: FCT9

Method: Least Squares

Date: 01/02/01 Time: 18:51

Sample(adjusted): 1997:07 2004:04

Included observations: 82 after adjusting endpoints Convergence

achieved after 11 iterations

Backcast: 1996:09 1997:06

|

Variable

|

Coefficient

|

Std. Error t-Statistic

|

Prob.

|

|

AR(2)

|

0.883380

|

0.089082 9.916442

|

0.0000

|

|

AR(6)

|

-0.172742

|

0.078240 -2.207844

|

0.0302

|

|

MA(10)

|

-0.128983

|

0.050538 -2.552231

|

0.0127

|

MA(1)

|

1.179665

|

0.104095 11.33254

|

0.0000

|

MA(2)

|

|

0.31 4264

|

0.115060 2.731303

|

0.0078

|

|

|

R-squared

|

0.894593

|

Mean dependent var

|

1.320023

|

|

Adjusted R-squared

|

0.889117

|

S.D. dependent var

|

2.272249

|

|

S.E. of regression

|

0.756637

|

Akaike info criterion

|

2.339172

|

|

Sum squared resid

|

44.08252

|

Schwarz criterion

|

2.485923

|

|

Log likelihood

|

-90.90606

|

Durbin-Watson stat

|

2.063749

|

Corrélogramme des résidus

Date: 01/02/01 Time: 18:52 Sample: 1997:07 2004:04 Included

observations: 82

Q-statistic

probabilities

adjusted for 5

ARMA term(s)

|

Autocorrelation

|

Partial Correlation

|

|

AC

|

PAC

|

Q-Stat

|

Prob

|

|

.*| .

|

|

|

.*| .

|

|

|

1

|

-0.085

|

-0.085

|

0.6173

|

|

|

. | .

|

|

|

. | .

|

|

|

2

|

-0.006

|

-0.014

|

0.6207

|

|

|

.*| .

|

|

|

.*| .

|

|

|

3

|

-0.063

|

-0.065

|

0.9644

|

|

|

.*| .

|

|

|

.*| .

|

|

|

4

|

-0.078

|

-0.090

|

1.4956

|

|

|

. | .

|

|

|

. | .

|

|

|

5

|

-0.004

|

-0.021

|

1.4973

|

|

|

. | .

|

|

|

. | .

|

|

|

6

|

-0.025

|

-0.035

|

1.5556

|

0.212

|

|

. | .

|

|

|

. | .

|

|

|

7

|

0.004

|

-0.014

|

1.5570

|

0.459

|

|

.*| .

|

|

|

.*| .

|

|

|

8

|

-0.107

|

-0.120

|

2.6177

|

0.454

|

|

. |**

|

|

|

. |**

|

|

|

9

|

0.229

|

0.208

|

7.5590

|

0.109

|

|

. | .

|

|

|

. | .

|

|

|

10

|

-0.012

|

0.015

|

7.5733

|

0.181

|

|

.*| .

|

|

|

.*| .

|

|

|

11

|

-0.087

|

-0.103

|

8.3059

|

0.217

|

|

**| .

|

|

|

**| .

|

|

|

12

|

-0.247

|

-0.274

|

14.290

|

0.046

|

|

.*| .

|

|

|

.*| .

|

|

|

13

|

-0.080

|

-0.106

|

14.929

|

0.061

|

|

. |*.

|

|

|

. |*.

|

|

|

14

|

0.115

|

0.098

|

16.271

|

0.061

|

|

. | .

|

|

|

. | .

|

|

|

15

|

0.057

|

0.055

|

16.606

|

0.084

|

FONCTION 10

Résultats de l'estimation

Dependent Variable: FCT1 0

Method: Least Squares

Date: 01/03/01 Time: 19:29

Sample(adjusted): 1997:02 2004:04

Included observations: 87 after adjusting endpoints Convergence

achieved after 8 iterations

Backcast: 1996:02 1997:01

|

Variable

|

Coefficient

|

Std. Error t-Statistic

|

Prob.

|

|

AR(1)

|

0.964445

|

0.027906 34.56105

|

0.0000

|

|

MA(12)

|

-0.927823

|

0.038116 -24.34212

|

0.0000

|

|

R-squared

|

0.827159

|

Mean dependent var

|

3.251829

|

|

Adjusted R-squared

|

0.825126

|

S.D. dependent var

|

7.137689

|

|

S.E. of regression

|

2.984837

|

Akaike info criterion

|

5.047688

|

|

Sum squared resid

|

757.2865

|

Schwarz criterion

|

5.104375

|

|

Log likelihood

|

-217.5744

|

Durbin-Watson stat

|

2.259114

|

Corrélogramme des résidus

Date: 01/03/01 Time: 19:31 Sample: 1997:02 2004:04 Included

observations: 87

Q-statistic

probabilities

adjusted for 2

ARMA term(s)

|

Autocorrelation

|

Partial Correlation

|

|

AC

|

PAC

|

Q-Stat

|

Prob

|

|

.*| .

|

|

|

.*| .

|

|

|

1

|

-0.130

|

-0.130

|

1.5276

|

|

|

. | .

|

|

|

.*| .

|

|

|

2

|

-0.049

|

-0.067

|

1.7437

|

|

|

. | .

|

|

|

. | .

|

|

|

3

|

0.008

|

-0.008

|

1.7494

|

0.186

|

|

. | .

|

|

|

. | .

|

|

|

4

|

-0.027

|

-0.030

|

1.8152

|

0.403

|

|

. | .

|

|

|

. | .

|

|

|

5

|

0.063

|

0.056

|

2.1882

|

0.534

|

|

. | .

|

|

|

. | .

|

|

|

6

|

-0.019

|

-0.006

|

2.2229

|

0.695

|

|

.*| .

|

|

|

.*| .

|

|

|

7

|

-0.176

|

-0.177

|

5.2144

|

0.390

|

|

. |**

|

|

|

. |*.

|

|

|

8

|

0.229

|

0.189

|

10.359

|

0.110

|

|

. | .

|

|

|

. | .

|

|

|

9

|

-0.016

|

0.020

|

10.386

|

0.168

|

|

. | .

|

|

|

. | .

|

|

|

10

|

0.010

|

0.029

|

10.396

|

0.238

|

|

**| .

|

|

|

**| .

|

|

|

11

|

-0.194

|

-0.212

|

14.243

|

0.114

|

|

.*| .

|

|

|

.*| .

|

|

|

12

|

-0.110

|

-0.142

|

15.491

|

0.115

|

|

. |*.

|

|

|

. | .

|

|

|

13

|

0.104

|

0.035

|

16.630

|

0.119

|

|

. | .

|

|

|

. | .

|

|

|

14

|

0.060

|

0.060

|

17.006

|

0.149

|

|

. | .

|

|

|

. |*.

|

|

|

15

|

-0.006

|

0.086

|

17.010

|

0.199

|

FONCTION 11

Résultats de l'estimation de D(FCT11)

Dependent Variable: D(FCT1 1)

Method: Least Squares

Date: 01/03/01 Time: 19:47

Sample(adjusted): 1997:04 2004:04

Included observations: 85 after adjusting endpoints Convergence

achieved after 8 iterations

Backcast: OFF (Roots of MA process too large)

|

Variable

|

Coefficient

|

Std. Error t-Statistic

|

Prob.

|

|

AR(2)

|

-0.365521

|

0.103162 -3.543164

|

0.0007

|

|

MA(10)

|

0.143445

|

0.055531 2.583165

|

0.0116

|

|

MA(12)

|

-1.028131

|

0.055940 -18.37903

|

0.0000

|

|

R-squared

|

0.634452

|

Mean dependent var

|

0.137891

|

|

Adjusted R-squared

|

0.625536

|

S.D. dependent var

|

4.248481

|

|

S.E. of regression

|

2.599791

|

Akaike info criterion

|

4.783396

|

|

Sum squared resid

|

554.2310

|

Schwarz criterion

|

4.869607

|

|

Log likelihood

|

-200.2943

|

Durbin-Watson stat

|

1.974595

|

Corrélogramme des résidus

Date: 01/03/01 Time: 19:48 Sample: 1997:04 2004:04 Included

observations: 85

Q-statistic

probabilities

adjusted for 3

ARMA term(s)

|

Autocorrelation

|

Partial Correlation

|

|

AC

|

PAC

|

Q-Stat

|

Prob

|

|

.

|

| .

|

|

|

.

|

| .

|

|

|

1

|

0.012

|

0.012

|

0.0122

|

|

|

.

|

| .

|

|

|

.

|

| .

|

|

|

2

|

-0.008

|

-0.008

|

0.0182

|

|

|

.

|

| .

|

|

|

.

|

| .

|

|

|

3

|

0.062

|

0.063

|

0.3703

|

|

|

.

|

| .

|

|

|

.

|

| .

|

|

|

4

|

-0.002

|

-0.004

|

0.3708

|

0.543

|

|

.

|

| .

|

|

|

.

|

| .

|

|

|

5

|

0.023

|

0.025

|

0.4209

|

0.810

|

|

.

|

| .

|

|

|

.

|

| .

|

|

|

6

|

0.020

|

0.016

|

0.4586

|

0.928

|

|

.

|

| .

|

|

|

.

|

| .

|

|

|

7

|

-0.049

|

-0.049

|

0.6890

|

0.953

|

|

.

|

| .

|

|

|

.

|

| .

|

|

|

8

|

0.015

|

0.014

|

0.7120

|

0.982

|

|

.*| . |

|

.*| . |

|

9

|

-0.102

|

-0.106

|

1.7269

|

0.943

|

|

. | . |

|

. | . |

|

10

|

0.052

|

0.062

|

1.9967

|

0.960

|

|

.*| . |

|

.*| . |

|

11

|

-0.097

|

-0.107

|

2.9319

|

0.939

|

|

.*| . |

|

.*| . |

|

12

|

-0.155

|

-0.138

|

5.3641

|

0.801

|

|

. | . |

|

. | . |

|

13

|

0.012

|

0.009

|

5.3797

|

0.864

|

|

. | . |

|

. | . |

|

14

|

0.010

|

0.019

|

5.3897

|

0.911

|

|

. | . |

|

. | . |

|

15

|

-0.039

|

-0.019

|

5.5499

|

0.937

|

FONCTION 12

Résultats de l'estimation de D(FCT12)

Dependent Variable: D(FCT12)

Method: Least Squares

Date: 01/03/01 Time: 19:52

Sample(adjusted): 1997:03 2004:04

Included observations: 86 after adjusting endpoints Convergence

achieved after 26 iterations

Backcast: OFF (Roots of MA process too large)

|

Variable

|

Coefficient

|

Std. Error t-Statistic

|

Prob.

|

|

AR(1)

|

-0.411614

|

0.101713 -4.046822

|

0.0001

|

|

MA(4)

|

-0.209317

|

0.068019 -3.077325

|

0.0028

|

|

MA(6)

|

0.354961

|

0.072853 4.872284

|

0.0000

|

|

MA(12)

|

-1 .055603

|

0.096379 -10.95260

|

0.0000

|

|

R-squared

|

0.612177

|

Mean dependent var

|

-0.057700

|

|

Adjusted R-squared

|

0.597988

|

S.D. dependent var

|

3.258705

|

|

S.E. of regression

|

2.066162

|

Akaike info criterion

|

4.334658

|

|

Sum squared resid

|

350.0601

|

Schwarz criterion

|

4.448814

|

|

Log likelihood

|

-182.3903

|

Durbin-Watson stat

|

2.053124

|

Corrélogramme des résidus

Date: 01/03/01 Time: 19:53 Sample: 1997:03 2004:04 Included

observations: 86

Q-statistic

probabilities

adjusted for 4

ARMA term(s)

|

Autocorrelation

|

Partial Correlation

|

|

AC

|

PAC

|

Q-Stat

|

Prob

|

|

. | .

|

|

|

. | .

|

|

|

1

|

-0.027

|

-0.027

|

0.0668

|

|

|

.*| .

|

|

|

.*| .

|

|

|

2

|

-0.075

|

-0.076

|

0.5756

|

|

|

. | .

|

|

|

. | .

|

|

|

3

|

-0.021

|

-0.026

|

0.6166

|

|

|

. | .

|

|

|

. | .

|

|

|

4

|

-0.018

|

-0.025

|

0.6456

|

|

|

. | .

|

|

|

. | .

|

|

|

5

|

0.005

|

0.000

|

0.6478

|

0.421

|

|

. |*.

|

|

|

. | .

|

|

|

6

|

0.067

|

0.063

|

1.0665

|

0.587

|

|

**| .

|

|

|

**| .

|

|

|

7

|

-0.201

|

-0.200

|

4.9261

|

0.177

|

|

.*| .

|

|

|

.*| .

|

|

|

8

|

-0.093

|

-0.099

|

5.7643

|

0.217

|

|

. |*.

|

|

|

. | .

|

|

|

9

|

0.086

|

0.056

|

6.4853

|

0.262

|

|

. |**

|

|

|

. |**

|

|

|

10

|

0.209

|

0.206

|

10.835

|

0.094

|

|

. | .

|

|

|

. | .

|

|

|

11

|

-0.039

|

-0.031

|

10.991

|

0.139

|

|

.*| .

|

|

|

.*| .

|

|

|

12

|

-0.085

|

-0.082

|

11.729

|

0.164

|

|

. | .

|

|

|

. | .

|

|

|

13

|

0.013

|

0.038

|

11.745

|

0.228

|

|

.*| .

|

|

|

.*| .

|

|

|

14

|

-0.064

|

-0.092

|

12.176

|

0.273

|

|

. | .

|

|

|

. | .

|

|

|

15

|

0.027

|

-0.024

|

12.254

|

0.345

|

ANNEXE 3 : Données relatives aux

douze fonctions.

· FONCTION 1

|

1997

|

1998

|

1999

|

2000

|

2001

|

2002

|

2003

|

2004

|

Janvier

|

1.94

|

5,42

|

4,93

|

-5,68

|

3,65

|

4,45

|

5,23

|

-2,66

|

Février

|

1.05

|

4,98

|

2,33

|

-2,38

|

0,71

|

8,40

|

3,67

|

-2,42

|

Mars

|

3.43

|

5,56

|

-4,10

|

5,33

|

0,45

|

6,40

|

-1,27

|

-1,76

|

Avril

|

8.12

|

5,86

|

-0,42

|

-1,19

|

0,82

|

6,63

|

-2,52

|

-1,80

|

Mai

|

5.09

|

9,67

|

-0,36

|

-0,31

|

3,60

|

2,64

|

-2,63

|

|

Juin

|

3.4

|

15,03

|

-6,33

|

3,51

|

0,00

|

8,48

|

-6,25

|

|

Juillet

|

1.97

|

10,15

|

-0,77

|

1,43

|

2,21

|

13,63

|

-10,72

|

|

Août

|

0.91

|

8,00

|

3,75

|

-0,77

|

1,15

|

7,70

|

-7,31

|

|

Septembre

|

-1.43

|

8,13

|

2,95

|

-1,28

|

3,28

|

2,80

|

-2,30

|

|

Octobre

|

-0.21

|

4,24

|

3,24

|

3,00

|

4,08

|

0,86

|

0,51

|

|

Novembre

|

4.17

|

4,02

|

-1,99

|

4,08

|

0,00

|

9,35

|

-1,97

|

|

Décembre

|

7.42

|

6,24

|

-6,76

|

8,36

|

4,70

|

0,84

|

-2,95

|

|

|

Source : INSAE

· FONCTION 2

|

1997

|

1998

|

1999

|

2000

|

2001

|

2002

|

2003

|

2004

|

|

Janvier

|

4,21

|

9,45

|

9,51

|

2,15

|

8,59

|

-1,20

|

0,34

|

4,40

|

|

Février

|

3,86

|

9,58

|

9,58

|

3,14

|

6,41

|

0,35

|

0,23

|

4,47

|

|

Mars

|

4,38

|

19,59

|

0,54

|

3,88

|

4,82

|

1,33

|

-0,79

|

4,45

|

|

Avril

|

4,63

|

19,33

|

0,82

|

3,81

|

4,49

|

0,10

|

0,38

|

4,73

|

|

Mai

|

4,89

|

19,08

|

0,54

|

4,88

|

19,39

|

-13,08

|

2,84

|

|

|

Juin

|

6,44

|

16,99

|

0,82

|

4,92

|

3,78

|

-0,09

|

5,40

|

|

|

Juillet

|

11,31

|

11,94

|

1,04

|

4,57

|

4,02

|

0,06

|

5,03

|

|

|

Août

|

12,11

|

11,14

|

1,19

|

4,79

|

4,56

|

-0,75

|

5,07

|

|

|

Septembre

|

13,45

|

9,90

|

0,97

|

5,68

|

3,47

|

-0,25

|

4,74

|

|

|

Octobre

|

13,00

|

10,07

|

1,42

|

5,37

|

3,58

|

-0,39

|

5,11

|

|

|

Novembre

|

13,55

|

9,34

|

1,19

|

6,42

|

0,00

|

19,86

|

-9,48

|

|

|

Décembre

|

13,06

|

10,37

|

1,73

|

6,34

|

1,47

|

16,97

|

-9,91

|

|

|

1997

|

1998

|

1999

|

2000

|

2001

|

2002

|

2003

|

2004

|

|

Janvier

|

0,33

|

0,91

|

4,11

|

0,10

|

3,19

|

1,35

|

0,76

|

-0,85

|

|

Février

|

0,38

|

2,33

|

2,60

|

0,16

|

3,15

|

1,34

|

0,80

|

-1,44

|

|

Mars

|

0,38

|

2,86

|

2,07

|

0,23

|

2,05

|

2,36

|

0,87

|

-0,96

|

|

Avril

|

0,38

|

2,86

|

1,95

|

2,93

|

-0,50

|

2,63

|

0,61

|

-0,96

|

|

Mai

|

0,37

|

2,89

|

1,93

|

4,01

|

-8,07

|

9,92

|

0,61

|

|

|

Juin

|

0,26

|

3,40

|

1,56

|

4,71

|

-1,45

|

1,82

|

0,61

|

|

|

Juillet

|

0,75

|

2,90

|

1,52

|

4,86

|

-1,49

|

1,77

|

0,61

|

|

|

Août

|

0,79

|

3,73

|

0,50

|

5,03

|

-1,61

|

1,92

|

0,14

|

|

|

Septembre

|

0,87

|

3,65

|

0,39

|

5,72

|

-2,02

|

1,77

|

0,15

|

|

|

Octobre

|

0,91

|

3,68

|

0,29

|

5,76

|

-1,85

|

1,59

|

0,16

|

|

|

Novembre

|

1,15

|

3,61

|

0,11

|

5,33

|

0,00

|

-4,95

|

5,50

|

|

|

Décembre

|

2,00

|

2,75

|

0,11

|

5,23

|

-1,11

|

-3,65

|

5,34

|

|

Source : INSAE

· FONCTION 4

|

1997

|

1998

|

1999

|

2000

|

2001

|

2002

|

2003

|

2004

|

|

Janvier

|

5,60

|

6,62

|

0,13

|

0,07

|

9,98

|

1,75

|

7,01

|

0,80

|

|

Février

|

6,18

|

7,64

|

-0,24

|

-0,12

|

8,34

|

1,30

|

10,65

|

-1,38

|

|

Mars

|

7,64

|

5,40

|

0,58

|

-0,70

|

8,84

|

-0,11

|

12,47

|

-1,83

|

|

Avril

|

6,99

|

6,86

|

-1,28

|

0,58

|

9,11

|

4,21

|

7,50

|

-2,02

|

|

Mai

|

10,00

|

3,94

|

-1,28

|

2,91

|

14,76

|

-7,54

|

11,12

|

|

|

Juin

|

10,30

|

4,39

|

-2,34

|

9,93

|

2,48

|

-1,63

|

8,60

|

|

|

Juillet

|

10,40

|

2,42

|

-1,24

|

10,90

|

2,67

|

-1,99

|

8,53

|

|

|

Août

|

9,91

|

1,97

|

0,53

|

9,31

|

3,09

|

6,62

|

-0,04

|

|

|

Septembre

|

8,92

|

3,01

|

1,31

|

8,50

|

3,47

|

6,28

|

0,24

|

|

|

Octobre

|

8,96

|

5,38

|

-1,71

|

16,23

|

-3,97

|

7,94

|

0,19

|

|

|

Novembre

|

9,00

|

6,27

|

-3,12

|

14,06

|

0,00

|

11,72

|

-5,10

|

|

|

Décembre

|

9,29

|

2,69

|

-0,86

|

13,74

|

-1,07

|

14,25

|

-5,19

|

|

|

1997

|

1998

|

1999

|

2000

|

2001

|

2002

|

2003

|

2004

|

|

Janvier

|

1,43

|

5,15

|

4,38

|

-0,66

|

1,10

|

3,65

|

0,37

|

-0,69

|

|

Février

|

1,47

|

6,40

|

3,19

|

-0,18

|

0,28

|

3,90

|

2,63

|

-2,85

|

|

Mars

|

2,33

|

5,12

|

3,23

|

0,72

|

0,30

|

3,29

|

2,81

|

-3,01

|

|

Avril

|

3,23

|

4,90

|

2,09

|

1,59

|

1,21

|

2,00

|

2,66

|

-2,94

|

|

Mai

|

3,49

|

6,03

|

0,62

|

1,83

|

5,24

|

-2,01

|

4,01

|

|

|

Juin

|

4,02

|

5,24

|

0,86

|

2,28

|

1,79

|

0,86

|

2,52

|

|

|

Juillet

|

4,72

|

7,27

|

-1,71

|

3,47

|

0,60

|

1,27

|

2,30

|

|

|

Août

|

4,86

|

7,30

|

-2,36

|

4,11

|

0,66

|

0,63

|

2,78

|

|

|

Septembre

|

4,89

|

7,36

|

-3,29

|

5,36

|

0,17

|

0,83

|

2,74

|