APPENDIX

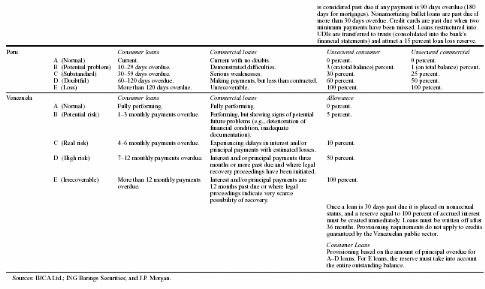

Appendix 1: Loan loss provisioning in selected emerging

markets

Appendix 1: (continued)

Appendix 1: (concluded)

Annex 2: The 25 core principles of the Basel Committee

on Banking Supervision

Principle 1: An effective system of banking

supervision will have clear responsibilities and objectives

for each agency involved in the supervision of banks. Each

such agency should possess operational independence and adequate resources.

A suitable legal framework for banking supervision is also necessary,

including provisions relating to authorisation of banking establishments and

their ongoing supervision; powers to address compliance with laws as well as

safety and soundness concerns; and legal protection for supervisors.

Arrangements for sharing information between supervisors and protecting

the confidentiality of such information should be in place.

Principle 2: The permissible activities of

institutions that are licensed and subject to supervision as banks must be

clearly defined, and the use of the word «bank» in names should be

controlled as far as possible.

Principle 3: The licensing authority must

have the right to set criteria and reject applications for

establishments that do not meet the standards set. The licensing process, at a

minimum, should consist

of an assessment of the banking organisation's ownership

structure, directors and senior management,

its operating plan and internal controls, and its projected

financial condition, including its capital base; where the proposed owner

or parent organisation is a foreign bank, the prior consent of its

home country supervisor should be obtained.

Principle 4: Banking supervisors must have

the authority to review and reject any proposals to transfer

significant ownership or controlling interests in existing banks to other

parties.

Principle 5: Banking supervisors must

have the authority to establish criteria for reviewing major

acquisitions or investments by a bank and ensuring that corporate

affiliations or structures do not expose the bank to undue risks or hinder

effective supervision.

Principle 6: Banking supervisors must set

minimum capital adequacy requirements for banks that reflect the risks

that the bank undertakes, and must define the components of capital, bearing in

mind

its ability to absorb losses. For internationally active banks,

these requirements must not be less than those established in the Basel Capital

Accord.

Principle 7: An essential part of any

supervisory system is the independent evaluation of a bank's policies,

practices and procedures related to the granting of loans and making of

investments and the ongoing management of the loan and investment

portfolios.

Principle 8: Banking supervisors must be

satisfied that banks establish and adhere to adequate policies,

practices and procedures for evaluating the quality of assets and the adequacy

of loan loss provisions and reserves.

Principle 9: Banking supervisors must be

satisfied that banks have management information systems that enable

management to identify concentrations within the portfolio and

supervisors must set prudential limits to restrict bank exposures to single

borrowers or groups of related borrowers.

Principle 10: In order to prevent

abuses arising from connected lending, banking supervisors must have in

place requirements that banks lend to related companies and individuals on an

arm's-length basis, that such extensions of credit are effectively

monitored, and that other appropriate steps are taken to control or

mitigate the risks.

Principle 11: Banking supervisors must be

satisfied that banks have adequate policies and procedures

for identifying, monitoring and controlling country risk and

transfer risk in their international lending and investment activities, and for

maintaining appropriate reserves against such risks.

Principle 12: Banking supervisors must be

satisfied that banks have in place systems that accurately measure, monitor

and adequately control market risks; supervisors should have powers to

impose specific limits and /or a specific capital charge on market risk

exposures, if warranted.

Principle 13: Banking supervisors must

be satisfied that banks have in place a comprehensive risk management

process (including appropriate board and senior management oversight)

to identify, measure, monitor and control all other material risks and, where

appropriate, to hold capital against these risks.

Principle 14: Banking supervisors must

determine that banks have in place internal controls that are adequate for

the nature and scale of their business. These should include clear

arrangements for delegating authority and responsibility; separation of the

functions that involve committing the bank, paying away its funds, and

accounting for its assets and liabilities; reconciliation of these processes;

safeguarding its assets; and appropriate independent internal or

external audit and compliance functions to test adherence to these controls

as well as applicable laws and regulations.

Principle 15: Banking supervisors must

determine that banks have adequate policies, practices and procedures

in place, including strict «know-your-customer» rules that

promote high ethical and professional standards in the financial sector

and prevent the bank being used, intentionally or unintentionally, by

criminal elements.

Principle 16: An effective banking supervisory

system should consist of some form of both on-site and off-site supervision.

Principle 17: Banking supervisors must have

regular contact with bank management and a thorough understanding of the

institution's operations.

Principle 18: Banking supervisors must have

a means of collecting, reviewing and analysing prudential reports and

statistical returns from banks on a solo and consolidated basis.

Principle 19: Banking supervisors must have

a means of independent validation of supervisory information either

through on-site examinations or use of external auditors.

Principle 20: An essential element of banking

supervision is the ability of the supervisors to supervise the banking group on

a consolidated basis.

Principle 21: Banking supervisors must be

satisfied that each bank maintains adequate records drawn

up in accordance with consistent accounting policies and

practices that enable the supervisor to obtain

a true and fair view of the financial condition of the bank and

the profitability of its business, and that the bank publishes on a regular

basis financial statements that fairly reflect its condition.

Principle 22: Banking supervisors must have

at their disposal adequate supervisory measures to bring about timely

corrective action when banks fail to meet prudential requirements

(such as minimum capital adequacy ratios), when there are regulatory

violations, or where depositors are threatened in any other way. In extreme

circumstances, this should include the ability to revoke the banking license

or recommend its revocation.

Principle 23: Banking supervisors

must practise global consolidated supervision over their

internationally active banking organisations, adequately monitoring

and applying appropriate prudential norms to all aspects of the business

conducted by these banking organisations worldwide, primarily at their foreign

branches, joint ventures and subsidiaries.

Principle 24: A key component of consolidated

supervision is establishing contact and information exchange with the various

other supervisors involved, primarily host country supervisory authorities.

Principle 25: Banking supervisors must require

the local operations of foreign banks to be conducted

to the same high standards as are required of

domestic institutions and must have powers to share information needed

by the home country supervisors of those banks for the purpose of carrying out

consolidated supervision.

|