Gestion du résultat, les déterminants de la structure financière et le coà»t de la dette: étude empirique sur les entreprises tunisiennes non financières cotées( Télécharger le fichier original )par Mohamed Ali Saadellaoui University of Carthage - Finance 2016 |

BibliographieA Ø Abbas, A.,(2013).,« Effect of capital structure on the performance of firms: Evidence from Pakistan and Indian stock market», Journal of Business and Management, Vol 12, No 6 , PP 83-93. Ø Abarbanell, J. et Lehavy, R., (2003), « Can Stok Recommendations Predict Earning Management and Analyst Earning orecast Erros ? », Journal of Accounting Research, vol 14, No 1, pp 1-332. Ø Adjaoud, F., Zeghal, D et Andaleeb, S., (2007), « The effect of board's quality on performance: a study of Canadian firms », Journal of Compilation, Vol 15, No 4. Ø Aghion, P. et Bolton, P., (1992), « An incomplete contracts approach to financial contracting » , Review of Economic Studies, Vol 59, pp 473-494. Ø Aharony, J. C., Lin, J. et Loeb, M. P., (1993), « Initial Public Offerings, Accounting Choices, and Management », Contemporary Accounting Research, Vol 10, No 1, pp. 61-81. Ø Ahmed, A. S, Nainar, S.M.K et Zhou, J (2001), « Do analysts forecasts fully reflect the information in accruals? », Syracuse University Working Paper. www.ssrn.com Ø Arnoud W. A. Boot (2000), « Relationship Banking: What Do We Know? »,Journal of Financial Intermediation, Vol 9, pp7-25 Ø Amblard, M., (2010), « La mesure comptable de la performance financière : évolution des normes, stabilité des principes », version 1, http://hal.archives-ouvertes.fr/docs/00/52/22/87/PDF/p203.pdf Ø Akerlof, G. 1970, « The Market For Lemons: Qualitative Uncertainty and the Market Mechanism », Qualterly Journal Of Economies, Vol. 85, pp488-500 . Ø Akhigbe, A., Martin. A. D, (2006), «Valuation impact of Sarbanes-Oxley: Evidence from disclosure and governance within the financial services industry», Journal of Banking & Finance, Vol 30 ,No3, pp 989-1006. Ø Albouy, M, (2002)., « L'actionnaire comme apporteur de ressources financières», Revue française de gestion, Vol 5 , No 141 cairn.info.sci-hub.org Ø Alchian, A. A., and Demsetz, H, (1972)., « Production, Information Costs, and Economic Organization », American Economic Review, Vol 62, pp 777-795. Ø Aldamen .H, Duncan .K et McNamara. R. (2010)., « Corporate Governance, Risk Assessment and Cost of Debt», School of Business, Bond University, Australia. Paper presented at the 2010 AFAANZ conference, Christchurch, New Zealand, pp1-32. Ø Altman, E. I., (1968)., «Financial Ratio, Discriminant Analysis and Prediction of Corporate Bankruptcy »Journal of Finance, September 1968, pp.589-610. Ø Andres, P., Azofra, V. et Lopez, F., (2005), « Corporate boards in OECD countries : size,composition, functioning and effectiveness », Journal of Blackwell Publishing Ltd, Vol 13, No 2, pp. 197-210. Ø Asano, T., Ishii, Y., Nakayama, S. et Tashiro, T., (2007), « Earnings management and the market performance of acquiring firms in stock-for-stock mergers : Evidence from Japan », 30th annual congress of European Accounting Association conference, Lisbonne. Ø Anderson R.c,.Mansi S.A.et Reeb,D.M.,(2004)., «Board characteristics, accounting report integrity, and the cost of debt», Journal of accounting and economics, Vol.37,pp.2003-243. Ø Ashbaugh-Skaife, H, D.W. Collings, and. LaFond, R.(2006)., «The Effects of Corporate Governance on Firms' Credit Ratings », Journal of Accounting and Economics,Vol42,pp203-243. Ø Asquitha, P., Beattyb, A et Webera. J (2005)., « Performance pricing in bank debt contracts», Journal of Accounting and Economics, Vol 40, pp 101-128. B Ø Baklouti, M, O., Matoussi, M et Ben Hamadi, S., (2011), «Désagrégation des accruals discrétionnaires et pertinence du bénéfice comptable», version1, http://hal.archivesouvertes.fr/docs/00/55/80/44/PDF/59MATOUSSI_BENHAMADI_BAKLOUTI.pdf Ø Balsam, S., (1998)., « Discretionary accounting choices and CEO compensation », Contemporary Accounting Research, Vol 15, No 3, pp. 229-252. Ø Balsam, S; Bartov, E. et Marquardt, C., (2002), « Accruals management, investor sophistication and equity valuation: Evidence from 10-Q filings », Journal of Accounting Research, September 2010. Ø Baik, B., Kang, J. K. et Morton, R. M., (2007), « Earnings Management in Takeovers of Privately Held Targets ». Working Paper, Florida State University Ø Ben Cheikh, S. et Zarai, M. A., (2008), « Importance des facteurs organisationnels sur le pouvoir managérial et la performance de la firme ». Colloque international fiscalité droit de gestion. Ø Ben Amar, I, N., (2009), « Free cach flow, gestion des résultants et gouvernement des entreprises : étude comparative des entreprises françaises et américaines ». thése Ø Ben Amar, F., (2009), « Free cach flow, gestion des résultats et gouvernement des entreprises : étude comparative des entreprises française et américaine », Journal de Financial Statement Analysis, Vol 4. Ø Ben Othman, H. et Zéghal, D., (2011), « analyse des déterminants de la gestion des résultats : cas des firmes canadiennes Françaises Et Tunisiennes », version 1, Comptabilité, Contrôle, Audit et Institution(S),Tunisie (2006), http://halshs.archives-ouvertes.fr/. Ø Bowen, R., Noreen , E, Lacey, J., (1981), « Determinants of The Corporate Decision to Capitalize Interest », Journal of Accounting and Economics, Vol 3, pp. 151-179. Ø Boynton, C., Dobbins, P. et Plesko, G., (1992), « Earning Management and the Corporate Alternative Minimum Tax », Journal o Accounting Research, vol 30, PP. 131-160. Ø Burgstahler, D. et Dichev, I., (1997), « Earnings management to avoid decreases and losses. », Journal of Accounting and Economics, Vol 24, pp. 99-126. Ø Breton, G. et Chenail, J. P., (1997), « Une étude empirique du lissage des bénéfices dans les entreprises canadiennes », Comptabilité - Contrôle - Audit, vol 1, no 3, p. 53-67. Ø Burgstahler, D. et Eames, M., (1998), « Management of earnings and analysts' forecasts », Working Paper, University of Washington. Ø Boynton, C., Dobbins, P. et Plesko, G., (1992), « Earning management and the corporate alternative minimum tax », Journal of Accounting Research, Vol 30, pp. 131-10. Ø Boisselier, P. et Jaouadi, M., (2011), « La gestion de résultat par les montages financiers de titrisation : le cas des sociétés françaises cotées », version 1, http://hal.archives-ouvertes.fr/docs/00/64/67/78/PDF/Boisselier_Jaouadi.pdf Ø Botsari, A. et Meeks, G., (2008), « Do acquirers manage earnings prior to a share for share bid? », Journal of Business Finance and Accounting, Vol 35, No 5-6, pp. 633-670. Ø Bauer, R., Frijns, B., Otten, R. et Tourani-Rad, A., (2008)., « The impact of corporate governance on corporate performance: evidence from Japan », Journal of Paci?c-Basin Finance, Vol 16, pp. 236-251. Ø Brown, L. D. et Caylor, L. M., (2006)., « Corporate governance and firm valuation », Journal of Accounting and Public Policy 25 (July-August), pp.409-434. Ø Ball, R., & Shivakumar, L, (2006)., « The role of accruals in asymmetrically timely gain and loss recognition», Journal of Accounting Research, Vol 44 , pp 207-242. Ø Baxter, D, (1967)., « Leverage, Risk of ruin and the Cost of capital »,Journal of Finance,Vol22, No4, pp395-403. Ø Beaver, W. H. (1966)., « Financial ratios as predictors of failures. Empirical Research in Accounting», Supplement to Journal of Accounting Research: pp 71-111. Ø Bharath, S. T., Sunder, J., Sunder S. V. (2004). « Do Sophisticated Investors Understand Accounting Quality? », Evidence from Bank Loans, Working Paper, University of Michigan. Ø Bhattacharya, Sudipto et Anjan .V, Thakor ,(1993)., «Contemporary Banking Theory»,, Journal of Financial Intermediation , Vol. 3, No 1, pp. 2-50. Ø Bhojraj ,S et Sengupta ,P, (2003)., « Effect of corporate governance on bond ratings and yields: The role of institutional investors and outside directors »The Journal of Business, 1086/jb.200376.issue- Vol 76, No 3 , JSTOR. Ø Blackwell, D.W. and Winters, D.B. (1997)., « Banking Relationships and the Effect of Monitoring on Loan Pricing», Journal of Financial Research, Vol 20, No. 2, pp.275-289. Ø Blackwell, David and David Kidwell, (1988), «An Investigation of the Cost Differences Between Public Sales and Private Placements of Debt», Journal of Financial Economics, Vol 22, pp253-278. Ø Boubakri, N et Ghouma, H .(2008)., «Managerial Opportunism, Cost of Debt Financing and Regulation Changes: Evidence from the Sarbanes-Oxley Act Adoption», Working Paper, School of Business and Management, HEC Montreal - Department of Finance. www.ssrn.com Ø Bradley M, Chen D, (2011)., «Corporate governance and the cost of debt: Evidence from director limited liability and indemnification provisions», Journal of Corporate Finance, Volume: 17, No 1, Publisher: Elsevier B.V, pp 83-107. Ø Brailsford, T. ., Barry O.., Pua S .L.H. (2002) «On the relation between ownership structure and capital structure»Accounting and Finance, Vol 42, pp.1-26. Ø Bushman .R, Piotroski. J et Smith A, (2003)., «What Determines Corporate Transparency? », University of Chicago and University of North Carolina, Working paper, (April). Ø Byreng, S.C, (2009), « the cost of private debt convenant violation », Duke university Working Paper C Ø Carpentier, C. et Suret, J., (2004), « Les manipulations comptables lors des émissions initiales au Canada », Université Laval, http://www.fsa.ulaval .ca /suretjm/index.htm. Ø Casati. R ,. (ý1999) « 1. QUESTIONS DE MÉTHODE 1.1. L'intérêt de l'analyse descriptive » http://hal.archivesouvertes.fr/docs/00/05/35/72/PDF/ijn_00000517_00.pdf. Ø Coughlan A, T et Smith, R. M., (1985)., « Executive compensation, management turnover, and firm performance: an empirical investigation. », Journal of Accounting and Economics, Vol. 7, pp. 43-66. Ø Coppensa, L. et Erik, E., (2005)., « An Analysis of Earnings Management by European Private Firms », Journal of International Accounting, Auditing & Taxation, Vol 14, No1, pp.1-17. Ø Cornett, M., McNutt, J. et Tehranian, H., (2006)., « Earnings Management at Large U.S. Bank Holding Companies », Document de travail, Southern Illinois University at Carbondale. Ø Calegari, M. J, (2000)., « The Effect of Tax Accounting Rules on Capital Structure and Discretionary Accruals », Journal of Accounting and Economics, Vol 30, No 1, PP.1-32. Ø Charreaux, G. A, Couret, P., Joffre, G. et Koening, B., (1987).,« La théorie positive de l'agence : une synthèse de la littérature », in de nouvelles théories pour gérer l'entreprise, de Montmorillon, Ed. Economica, Paris,1987,pp19-55 ouvrage Ø Charpin F (1998) « Une analyse économétrique multivariée du comportement des ménages » Revue de l'OFCE n° 66 / juillet 1998. Ø Cormier, D., Magnan, M. et Morard, B., (1998), « La gestion stratégique des résultats : le modèle anglo-saxon convient-il au contexte Suisse ? », Comptabilité, contrôle, audit, Vol 1, pp. 25-49. Ø Chalayer, S., (1994), « Identification et motivations des pratiques de lissage des résultats comptables des entreprises françaises cotées en Bourse », Thése de doctorat de gestion, Université de Saint-Etienne. Corrigé dans le mémoire. Thése Ø Chalayer, S., (1995), « Le lissage des résultats. Eléments explicatifs avancés dans la littérature », Comptabilité- Contrôle- Audit, Vol 2, No 1, pp 89- 104. Ø Copeland, R. M., (1968), « Income smoothing », Journal of Accounting Research, Empirical Research in Accounting, Selected (Supplement), pp. 101-106. Ø Chalayer, S., (1995), « Le lissage des résultats. Eléments explicatifs avancés dans la littérature », Comptabilité- Contrôle-Audit, Vol 2, No 1, pp. 89-104. Ø Cormier, D., Magnan, M., (1995), « La gestion stratégique des résultats : le cas des firmes publiant des prévisions lors d'un premier appel public à l'épargne », Journal de comptabilité- contrôle Audit, Vol 1, No 1, pp. 45-61. Ø Chabchoub, M. et Mrabet, M., (2011), « Gestion du résultat et introduction en bourse : cas des entreprises Tunisiennes », version 1, http://halshs.archives-ouvertes.fr/docs/00/54/49/54/PDF/p199.pdf Ø Cormier, D., Magnan, M. et Zéghal, D. M., (2000), « Le contenu informationnel et la capacité prédictive des mesures de performance financière : une comparaison France, Etats Unis et Suisse », Centre de recherche en gestion. Ø Cassar G, Cavalluzzo K.S et Christopher D.I, (2008)., « Cash Versus Accrual Accounting and the Availability and Cost of Small Business Debt », Working Paper Ø Chatterjee, S., and Price, B. (1991), « Regression Analysis by Example » (2nd ed.), New York, Wiley. Ouverage Ø Chatterjiee S., Hadi A.S., et Price B,.(2000), «Regrission analysis by exemple ». John Wiley et Sons Ø Chaney, P. K., Faccio, M., Parsley, D. (2011)., «The quality of accounting information in politically connected firms». Journal of Accounting and Economics, Vol 51,pp 58-76. Ø Chen Y.M, et Jian J.Y, (2006)., «the impact of information disclosure and transparency ranking system and corporate gouvernce structure on interest cost of debt », working paper www.ssrn.com Ø Chen,X et Cheng, Q (2002)., « Abnormal accruals -based anomaly and managers motivations to record ab normal accruals », Working paper, www.ssrn.com. Ø Chen. C and Zhu, S.,(2013)., « Financial Reporting Quality, Debt Maturity, and the Cost of Debt: Evidence from China», Emerging Markets Finance & Trade, Vol. 49, No 4, pp. 236-253. D Ø Dadashi. I, Zarei. S , Dadashi. B et Ahmadlou, Z (2013)., «Information Voluntary Disclosure and Cost of Debt Case of Iran», International Research Journal of Applied and Basic Sciences, Vol 4, No 6: pp1478-1483 Ø Defond, M et Jiambalvo, J, (1994).,« Debt covenant effects and the manipulation of accruals». Journal of Accounting and Economics Vol 17, pp 145-176. Ø Demirtas, K. O.; A. Ghosh; K. J. Rodgers; and J. Sokobin,(2006)., « Initial Credit Ratings and Earnings Management», Working Paper, City University of New York (2006). www.ssrn.com Ø Demirtas, K. Ozgur et Rodgers Cornaggia, Kimberly (2013)., «Initial credit ratings and earnings management», Review of Financial Economics, Vol 22 ,No 4, pp135-145. Ø Detragiache, Enrica, (1994)., «Public versus Private Borrowing: A Theory with Implications for Bankruptcy Reform», Journal of Financial Intermediation, Vol 3, pp 327-354. Ø Diamond, Douglas W., (1991)., « Monitoring and Reputation: The Choice Between Bank Loans and Directly Placed Debt», Journal of Political Economy, Vol 99,pp 689-721. Ø Dichev, I.D., Skinner . D.J, (2002)., « - Large sample evidence on the debt covenant hypothesis »Journal of Accounting Research», Vol 40 ,No 4, pp 1091-1123, Wiley Online Library. Ø Draief, S et Chouaya, A., (2012), « Effet de la gestion comptable et réelle des résultats sur le coût de la dette :analyse avant et après SOX », Journal of Accounting and Economics, Vol 42, pp203-243 Ø Draief, S.C, (2010)., « Gestion des résultats, atteinte des seuils et coût d'endettement», Manuscrit Auteur, Publié Dans La Comptabilite, Le Contrôle et L'audit Entre Changementet Stabilite ,France (2008). http://hal.inria.fr/docs/00/52/25/15/PDF/p83.pdf Ø Duke, J.C et Hunt. HG III(1900), « An empirical examination of debt covenant restrictions and accounting-related debt proxies» , Journal of Accounting and Economics Vol 12 pp 45-63. Ø DuCharme, L. L., Malatesta, P. H. et Sefcik, S. E., (2004), « Earnings Management, Stock issues, and shareholder lawsuits », Journal of Financial Economics, Vol 71, pp.27-49. Ø DeAngelo, L., (1986), « Accounting numbers as market valuation substitutes: a study of management buyouts of public stockholders », the accounting Review, Vol 61, No 3, pp.400-420. Ø DeFond, M. L et Jiambalvo, J., (1994)., « Debt Covenant Violation and the Manipulation of Accruals », Journal of Accounting and Economics, Vol 17, pp.145-176. Ø Dechow, P., Sloan, R et Sweeney, A., (1995), « Detecting earnings management », Journal of the Accounting Review, Vol 70, No 2, pp. 193-225. Ø DeAngelo, L., (1988), « Managerial competition, information costs, and corporate governance, the use of accounting performance measures in proxy contests ». Journal of Accounting and Economics, Vol 10, No 1, pp. 3-36. Ø Dechow, P, M. et Skinner, D., J, (2000), « Earnings Management:Reconciling the Views of Accounting Academics, Practitioners, and Regulators », Journal of Americain Accounting Association Accounting Horizons, Vol 14, No 2, pp. 235-250. Ø Dumontier, P. et Sloan, R., (1991), « Executive incentives and the horizon problem : an empirical investigation » , Journal of accounting and Economics, Vol 14, No 1, pp. 51-89. Ø Dumontier, P. et Elleuch, S., (2002), « How does the French stock market react to discretionary accruals », 25 th Annual Congress of the European Accounting Association, Copenhagen Business School, Denmark, pp 1 -20. Ø Draief, S., (2010), « Structure financière, gestion des résultats et caractéristiques de la firme », version 1, http://hal.archives-ouvertes.fr/docs/00/54/81/13/PDF/39-DRA IEF .pdf. Ø Dye, R., (1988), « Earnings Management in an Overlapping Generations Model », Journal of Accounting Research, Vol 26, No 2, pp 195-235.. Ø De Angelo, H., De Angelo, L. E., et Skinner, D. J., (1994)., « Accounting choice in troubled companies », Journal of Accounting and Economics, Vol 17, pp. 113-143. Ø DeAngelo, H.; DeAngelo, L. et Wruck, K., (2002)., « Asset liquidity, debt covenants and managerial discretion in financial distress: the collapse of L.A.Gear », Journal of financial economics, Vol 64, pp. 3-34. Ø DeAngelo, H., et Masulis, R., (1980), « Optimal capital structure under corporate and personal taxation », Journal of Financial Economics, Vol 8, No 1, pp. 3-29. Ø DeAngelo, L., (1986), « Accounting numbers as market valuation substitutes: a study of management by outs of public stockholders », The Accounting Review, Vol 61, July, pp. 400-420. Ø Dechow, P., Sloan R. et Sweeney, A. P., (1995), « Detecting earnings management », The Accounting Review, pp. 193-225. Ø Defond, M. et Jiambalvo, J., (1994), « Debt covenant effects and the manipulation of accruals », Journal of Accounting and Economics, Vol 17, pp. 145-176. Ø Degeorges, F., Patel, J. et Zeckhauser, R., (1999), « Earning Management to Exceed Thresholds », Journal of Business, vol 72, No 1, pp.1-33. Ø DeAngelo, H., DeAngelo, L. E., Skinner, D. J., (1994), « Accounting choice in troubled companies », Journal of Accounting and Economics, Vol 17, pp.113-143. Ø Dechow, P. M., Richardson, S. A et Tuna, I., (2003), « Why are earnings kinky? An examination of the earnings management explanation », Review of Accounting Studies, No 8, pp. 355-384. Ø Djama, C., (2003)., « Le risque de faillite modifie-t-il la politique comptable ? », Cahier de recherche, No 156, Louvain, IAE Toulouse. E Ø Elleuch, H. S., (2010), « Les spécificités de la gestion des résultats des entreprises tunisiennes à travers une analyse qualitative », version 1, http://hal.archives-ouvertes.fr/docs/00/52/48/87/PDF/p96.pdf Ø Elyasiani E, Jia J, Mao C, (2010)., « Institutional ownership stability and the cost of debt», Department of Finance, Fox School of Business and Management, Temple University, Philadelphia, PA 19122, USA. Ø Eng, L. et Nabar, S., (2007), « Loan loss provisions by banks in Hong Kong, Malaysia and Singapore », Journal of International Financial Management and Accounting, Vol 18, No1, pp.18-38. Ø El Mir, A. et Seboui, S., (2007)., « La gestion des résultats entre l'opportunisme managérial et la pression des résultats », La Revue des Sciences de Gestion, Direction et Gestion, No 224-225, pp. 93-102. Ø Erickson, M., Hanlon, M. et Maydew, E., (2004)., « Is there a link between executive compensation and accounting fraud ? », working paper, http://ssrn.com Ø Erickson, M. et Wang, S. W., (1999), « Earnings Management by Acquiring Firms in Stock for Stock Mergers », Journal of Accounting and Economics, Vol 27, pp. 149-176. Ø Erickson. M, Hanlon. M et Maydew, E.L., (2004), « How Much Will Firms Pay for Earning That Do Not Exist ? Evidence Taxes Paid on Allegedly Fraudulent Earning », The Accounting Review, Vol 79, No 2, PP. 387-408. F Ø Friedland, J. M., (1994), « Accounting choices of issuers of initial public offerings », Contemporary Account-31ing Research, Vol 11, pp.1-31. Ø Fama, E., (1970), « Efficient Capital Markets: A Review of Theory and Empirical Work », Journal of Finance, Vol 25, pp. 383-417. Ø Frank, M. et Goyal, V., (2003), «Testing the pecking order theory of-capital structure », Journal of Financial Economies, Vol 67, pp 217-248. Ø Francis, J., LaFond, R., Olsson, P et Schipper, K, (2005)., «The market pricing of accruals quality» ,.Journal of Accounting and Economics, Vol 39 ,pp 295-327. Ø Franz, R., HassabElnaby, H.R. et Labo, G. J., (2012), « Impact of Proximity to Debt convenant violation on earning management », Working paper. Ø Farrelly, G. E., Baker, H. K. et Edelman. R. D., (1985), « A Survey of Management Views on dividende Policy » , Journal of Financial Management, Vol 14, pp. 78 - 84. G Ø Guenther, D. A., (1994), « Earnings Management in Response to Corporate Tax Rate Changes: Evidence from the 1986 Tax Reform Act », The Accounting Review, Vol 69, No 1, pp 230-243. Ø Gul, F.; Leung, S. et Srinidhi, B., (2000), « The effect of investment opportunity set and debt level on earnings-returns relationship and the pricing of discretionary accruals », Working paper, www.ssrn.com. Ø Garnotel, G. et Loux, P., (2008), « Politiques de rémunération des dirigeants et investissements liés à l'innovation dans les industries de haute technologie », Journal de Finance Contrôle Stratégie, Vol 11, pp. 65-85. Ø Guan, L., Wright, C. J. et Leikam, S. L., (2005), « Earnings Management and Forced CEO Dismissal », Advances in Accounting, Vol 21, pp. 61-81. Ø Gong, G., Louis, H. et Sun A,X., (2008), « Earnings Management and Firms Performance Following Open-Market Repurshases », The Journal of Finance, Vol 63, pp.947-986. Ø Guenther, D., (1994)., « Earnings management in response to corporate tax rate changes: Evidence from the 1986 tax reform act ». The Accounting Review, Vol 69, No 1, pp.230 - 243. Ø Ghosha .A,et Jain P.C (2000), « Financial leverage changes associated with corporate mergers », Journal of Corporate Finance, Vol 6, pp 377-402 Ø Graham, J. R., Tucker, A., (2006),«Tax shelters and corporate debt policy». Journal of Financial Economics, Vol 81, pp563-594. H Ø Hergli, M., Bellalah, M. et Abdennadher, N., (2007), « Gouvernance d'entreprise et valeurs de marché en Tunisie », Journal International de Business et Finance, 4th International Finance conférence, Vol 21, pp 414-427. Ø Hurlin. C (2002)., « L'Econométrie des Données de Panel Modèles Linéaires Simples », Séminaire Méthodologique, Ecole Doctorale Edocif. Ø Hervé, S. et Gaetan, B.,(2003)., « La gestion des données comptables : une revue de la littérature », Comptabilité-Contrôle-Audit / Tome 9 - Vol 1 - Mai 2003. Ouvrage Ø Hermalin, B. et Weisbach, M., (1998)., « Endogenously chosen boards of directors and their monitoring of the CEO », American Economic Review, Vol 88, pp. 96-118. Ø Hagerman, R. L. et Zmijewski, M., (1979)., « Some Economic Determinants of Accounting Policy Choice », Journal of Accounting and Economics, Vol 1, No 2, pp.141-161. Ø Hrichi, Y., (2013)., « Les effets de l'adoption obligatoire des normes IFRS sur la gestion du résultat comptable : une analyse de 100 entreprises françaises », La Revue des Sciences de Gestion, Direction et Gestion No 263-264, pp. 163-170. Ø Hribar, P., Thorne, J. N., Johnson,W. B., (2006)., « Stock Repurchases as an Earnings Management Device », Journal of Accounting and Economics, Vol. 41, No 1, pp. 3-27. Ø Healy, P. et Wahlen, J., (1999)., « A review of the earnings management literature and its implications for standard setting », Journal of Accounting Horizons, Vol 13, No 4, pp. 365-383. Ø Healy, P., (1985), « The effect of bonus schemes on accounting decisions »., Journal of Accounting and Economics, Vol 7, pp.85-107. Ø Han, J. C. Y. et Wang, S., (1998), « Political costs and earnings management of oil companies during the 1990Persian Gulf crisis », The Accounting Review, Vol 73, pp. 103-117. Ø Hsiao, C., (1986), « Analysis of Panel Data », Econometric society Monographs, N 11, Cambridge Universirty Press. Ø Holthausen, R., Larcker, D. et Sloan. R, (1995), « Annual bonus schemes and the manipulation of earnings », Journal of Accounting and Economics, Vol 19, No 29, pp.74- 25. Ø Harris, M., Raviv, A, (1990)., «Capital structure and the informational role of debt »,Journal of Finance , Vol45, pp321-349 Ø Hamilton, L. C, (2004)., «Statistics with Stata», (Updated for Version 8), Paci?c Grove, CA. Ø Hergli, S etTeulon,F,(2013).,«Déterminants de la structure du capital : le cas tunisien» journal de Gestion 2000 , Vol 31, No5, pp49-73. Ø Hayn, C., (1995).,« The information content of losses », Journal of Accountings and Economics, Vol 20, pp. 125-153. Ø Healy, P., (1985), « The effect of bonus schemes on accounting decisions », Journal of Accounting and Economics, vol 7, pp.85-107. Ø Healy, P. et Wahlen, J., (1999), « A review of the earnings management literature and its implications for standard setting », Journal of Accounting Horizons, Vol 13, No 4, pp. 365-383. Ø Hugounenq, R,(2003)., « L'imposition des revenus du capital et des entreprises en Europe », Revue de l'OFCE, Vol 3 ,No 86, pp 43-81 cairn.info.sci-hub.orgJ Ø Jennifer, B., (2010), « les déterminants de la gestion des résultats lors des fusions: étude des sociétés absorbantes initiatrices et cibles », http://hal.archives-ouvertes. fr/docs/00/47/9 5/ 35 /PDF/p122.pdf. Ø Jones, J., (1991), « Earnings management during import relief investigations », Journal of Accounting Research, Autumn, Vol 29, No 2, pp.193-228. Ø Jeanjean , T., (2011), « Contribution a L'analyse de la Gestion du Résultat des Sociétés Cotées », http://hal.inria.fr/docs/00/58/46/33/PDF/JEANJEAN.PDF. Ø Janes, T. D, (2003)., «Accruals, financial distress and debt covenants», Working paper, University of Michigan Business School. Ø Janin, R. (2000), « Gestion des chiffres comptables, contenu informationnel du résultat et mesure de la création de valeur », Thèse de Doctorat, Université Pierre Mendés France, Grenoble, 321 pages. Thèse Ø Jean-Danial,G and Vilanova, l , (1999)., « Les vertus du financement bancaire :fondements et limites », revue finance, Control, stratégie, Vol 2, pp97-133. Ø Jensen, M. C, (1986)., « Agency cost or free cash flow, corporate finance and takeover», American Economic Review, Vol76, pp 323-329. Ø Jiang, J,(2008)., « Beating earnings benchmarks and the cost of debt», The Accounting Review, Vol 83, No2, Pp 377-416. Ø Johnson, S. A., (1997), « An empirical analysis of the determinants of corporate debt ownership structure »; Journal of Financial and qualitative analysis, Vol 31,No 1,pp. 47-69. Ø Juniarti et Lia, N., « (2012) Corporate Governance Perception Index (CGPI) and Cost of Debt», International Journal of Business and Social Science ,Vol 3 ,No. 18 pp 223-232 Ø Jadlaoui, F. et Hallara, S.,( 2013), « Analyse de l'effet de gestion de résultat sur l'utilité des données comptables : cas du contexte français », Revue Marocaine de Comptabilité, Contrôle et Audit, No2, pp.1-32. Ø Jeanjean, T., (2001), « Incitations et contraintes à la gestion du résultat », Journal of Comptabilité Contrôle Audit, Vol 7, No 1, pp.61-76. Ø Jensen, M. C. et Meckling, W., (1976), « Theory of the firm : managerial behavior, agency costs and ownership structure », Journal of Financial Economics, Vol 3, pp. 305-360. Ø Janin, R., (2000), « Gestion des chiffres comptables, contenu informationnel du résultat et mesure de la création de valeur », Thèse de Doctorat, Université Pierre Mendés France, Grenoble, p321. Ø Jensen, M.C., (1986), « Agency cost or free cash flow, corporate finance and takeover », American Economic Review, Vol 76, pp. 323-329. K Ø Klibi, M. F. et Matoussi, H., (2010), « Gestion des résultats et performance comptable et boursiere des entreprises émettrices de nouvelles actions », version 1, http: //ha ls hs.archives-ouvertes.fr/docs/00/53/47/52/PDF/p15.p df. Ø Kartobi, S.D, (2013)., « Déterminants De La Structure Financière Et Réactions Du Marche Boursier Aux Décisions De Financement : Cas Des Sociétés Marocaines Cotées A La Bourse Des Valeurs De Casablanca », Thèse En Cotutelle Internationale, http://tel.archivesouvertes.fr/docs/00/86/68/66/PDF/2013NICE0008.pdf Ø Karjalainen .J, (2008)., «Auditor Choice and Cost of Debt Financing for Private SMEs», Department of Business and Management, University of Kuopio, working paper, pp1-26. Ø Karjalainen .J, (2011)., « Audit Quality and Cost of Debt Capital for Private Firms: Evidence from Finland», International Journal of Auditing, Vol 15, pp 88-108. Ø Kebewar, M., (2011), « La structure du capital et la profitabilité une étude empirique sur données de panel françaises », Journal de Munich Personal RePEc Archive, Vol 2, No 1. Ø Kebewar, M., (2012), « La structure du capital et la profitabilité une étude empirique sur données de panel françaises », Journal de Munich Personal RePEc Archive, Vol 2, No 1. http://arxiv.org/ftp/arxiv/papers/1212/1212.6795.pdf Ø Kenndy, P., (1985), « A guide to econometrics», Basil Blakwell, Southam pton Ø Kim, B. H., Lisic, L. L et Pevzner, M.., (2011). « Debt covenant slack and real earnings management», Working paper, American University, Kogod School of Business. Ø Kothari, S. P., Leone, A. J., Wasley, C. E., (2005) « Performance-matched discretionary accrual measures», Journal of Accounting and Economics, Vol 39 ,pp 163-197. Ø Kaplan, S., (1989), « The Effects of Management Buyouts on Operating Performance and Value », Journal of Financial Economics, Vol. 24, pp 217-254. Ø Kothari, S. P., Leone, A et Wasley, C., (2005), « Performance matched discretionary accrual measures », Journal of Accounting and Economics, Vol 39, No 2, pp.163-197. Ø Kolsi, M. et Ghorbel, H., (2011), « Effet des mécanismes de gouvernance sur la performance financière et boursière : cas des entreprises canadiennes », version1, Manuscrit auteur, publié dans "Comptabilités, économie et société, Montpellier http://hal.archives-ouvertes.fr/docs/00/65/05/37/PDF/Kolsi_Ghorbel.pdf Ø Kholbadalov .U (2012) « The relationship of corporate tax avoidance, cost of debt and institutional ownership: evidence from Malaysia », Atlantic Review of Economics, Vol 2 , unagaliciamoderna.com. Ø Kelly, E. C., (2013)., « Capital Structure, Earnings Management, and Sarbanes-Oxley: Evidence from Canadian and U.S. Firms », Journal of American Accounting Association , Vol 27, No 2, pp 301-318. Ø Kim, M. et Ritter, J., (1999)., « Valuing IPOs », Journal of Financial Economics, Vol 53, pp. 409-437. Ø Koubaa, A. et Halioui, K, (2013)., « Importance relative des mesures de performance non financières dans les contrats de rémunération des dirigeants, un moyen de réduction de l'ampleur de la gestion de résultat », Journal of Financial and Quantitative Analysis, La Revue Gestion et Organisation, Vol 5, No 2, pp 103-112. Ø Kasznik, R., (1999).,« On the association between volontary and earning management », Journal of Association Research, Vol 37, No 1, pp. 57-81. Ø Kaplan, S., (1989), « The Effects of Management Buyouts on Operating Performance and Value », Journal of Financial Economics, vol. 24, PP. 217-254. L Ø Lambert, C. A. et Sponem, S. A., (2010), « Gouvernance d'entreprise et gestion du résultat, les contrôleurs de gestion de l'autre côté du miroir », version 1, http://hals hs.archives ouvertes.fr/docs/00/17/02/11/PDF/ Lam bertSponemafc20 03C OM0 38.pdf. Ø Lev, B. et Kunitzky, S., (1974)., « On the Association Between Smoothing Measures and the Risk of Common Stocks », The Accounting Review, Vol 49, No 2, pp 259-270. Ø Louis, H., (2004)., « Earnings Management and the Market Performance of Acquiring Firms », Journal of Financial Economics, Vol 74, pp. 121-148. Ø Lim, S. et Matolcsy, Z., (1999)., « Earnings management of firms subject to product price controls. », Accounting and Finance, Vol 39, pp.131-150. Ø Lehn, K. et Poulsen,A. B., (1989)., « Free Cash Flow and Stockholder Gains in Going Private Transactions », Journal of Finance, Vol. 44, pp. 771-787. Ø Lambert, C., (2003)., « Management controller's job: when ambiguity leads to job crafting », Congrès de l'European Accouting Association, Copenhague, 2003. Ø Leland, H., and D. H. Pyle, (1977).,« InformationaI Asymmetries, Financial Structure and Financial Intermediation », Journal of Finance, Vol 32, No. 2, pp371-387 Ø Lehn, K. et Poulsen,A. B., (1989)., « Free Cash Flow and Stockholder Gains in Going Private Transactions », Journal of Finance, Vol 44, pp 771-787. Ø Li, S., & Richie, N, (2009)., « Income smoothing and the cost of debt», working paper. http://www.fm a.org/Ren o /Papers/IncomeSmoothingandtheCostofDebtJan2009.pdf Ø Lim, Y. D, (2011)., « Tax avoidance, cost of debt and shareholder activism: Evidence from Korea». Journal of Banking & Finance, Vol 35,pp 456 - 470. Ø Lim, Y.D., (2010)., « Tax Avoidance and Underleverage: Korean Evidence », Working Paper, University of New South Wales. Ø Lin .S, Ma .Y, Malatesta .P et Xuan Y., «2010. Ownership structure and the cost of corporate borrowing», Chinese University of Hong Kong and Harvard Business School, Boston, MA, USA, working paper, (March). Ø Lobez F et Statnik . J-C (2007) « La complémentarité entre dette bancaire et dette obligataire : une interprétation en termes de signaux », Revue de l'association française de finance, Vol. 28, No 1, pp 5-27 M Ø Marnet, O., (2006), « History repeats it self: the failure of rational choice models governance », Journal Critical perspectives on accounting, Vol 17, pp. 587- 607. Ø Moreira, J. A. C. et Pope, P.F., (2007), « Earnings management to avoid losses : accost of debt explanation », Working paper, www.ssrn.com. Ø Mard, Y., (2004)., « Gestion des résultats comptables : l'influence de la politique financière de la performance et du contrôle », version 1, http://halshs.archives-ouvert es.fr/docs/00/ 59 /4 0 /12/PD F/Mard.pdf Ø Malecot J, F, (1984)., « Théorie financière et coûts de faillite », Thèse de doctorat d'Etat, p534. Ø Miller, M, (1977).,« Debt and Taxes », The Journal of Finance, Vol 32, pp. 261-275. Ø Minton, A et Schrand, C, (1999)., «The impact of cash flow volatility on discretionary investment and the costs of debt and equity financing», the journal of financial economics, Vol 54, pp 423-460.. Ø Modigliani F. et Miller M.H. (1958)., «The Cost of Capital, Corporate Finance, and the Theory of Investment», American Economic Review .Vol 48, pp. 261-297. Ø Modigliani, F et Miller, M. H, (1963)., Corporate Income Taxes and the Cost of Capital: A Correction, American Economic Review Vol 53 ,No 3,pp 433-443. Ø Moreira, J. A. C., Pope, P. F, (2007)., « Earnings management to avoid losses: a cost of debt explanation »,Working paper, Université de Porto. Ø Myers.S et N.S. VlajJuf (1984)., «Corporate finallcing and investmcnt dccisiolls when firms have information that investor do not have», Journal of Finaneia 1Econom ies, Vol 13, pp187-221 Ø Myers, S.C., (1977)., « Determinants of Corporate Borrowing », Journal of Financial Economics Vol 5, pp. 147-175. Ø Matoussi, M., Ben Hamadi, S. et Baklouti, M, O., (2011)., « Désagrégation des accruals discrétionnaires et pertinence du bénéfice comptable », Journal de HAL, version1, Janvier 2011. http://hal.archives-ouvertes.fr/docs/00/55/80/44/PDF/59-MATOUSSI_BENHAMADI_BAKLOUTI.pdf. Ø Murphy, K. et Zimmerman, J., (1993)., « Financial Performance Surrounding CEO Turnover », Journal of Accounting and Economics, Vol 16, pp. 273-316. Ø Mard, Y. et Marsat, S., (2009).,« La gestion du résultat comptable autour d'un changement de dirigeant en France Earnings management surrounding CEO changes in France», Comptabilité - Contrôle - Audit / Numéro thématique - Décembre 2009, pp. 141- 170. Ø Mard, Y. et Marsat, S., (2008)., « Les stratégies comptables entourant un changement de dirigeant en France Accounting Policies surrounding CEO Changes in France », http :// hal sh s.archives-ouvertes.fr/docs /00/52/54/ 27/P DF /p44.pdf. Ø Myers, L. et Skinner, D., (1999), « Earnings momentum and earnings management »,Working Paper Accounting Research Network, http://www.ss rn.com /update/ar n/arn _fi nacctg.html. Ø Matsumoto, D. A., (2002)., « Management's Incentives to Avoid Negative Earnings Surprises », The Accounting Review, Vol 77, pp.483-514. Ø Mard, Y. et Marsat, S., (2011)., « Gestion des résultats comptables et structure de l'actionnariat : le cas français », http://hal.archives-ouvertes. fr/docs/00/6 5/05/50/P DF/Mard_Marsat.pdf. Ø Mard, Y., (2011)., « Vers une information comptable plus transparente : l'apport des recherches portant sur la gestion des résultats comptables », http://hal.inria. fr/doc s/ 0 0/58/12/ 29 /pdf/62.pdf. Ø Morse, D. et Richardson, G., (1983), «The LIFO/FIFO decision ». Journal of Accounting Research, Vol. 21, pp. 106-127. Ø Mohammad, R. E,. Farzad ,E, Reza ,S .B et Ghorban ,S.,(2013) « The Impact of Capital Structure on Firm Performance: Evidence from Tehran Stock Exchange», Australian Journal of Basic and Applied Sciences ,Vol 7, No 4 ,pp: 1-8. Ø Malmquist, D., (1990)., « Efficient contracting and choice of accounting method in the oil and gas industry », Journal of Accounting and Economics, Vol 12, No (1-3), pp. 173-205. Ø Musiega, M .G, Chitiavi,M.S,. B.Alala.O et Douglas.M., (2013), « Capital Structure And Performance: Evidence From Listed Non-Financial Firms On Nairobi Securities Exchange (Nse) Kenya», International Journal for Management Science and Technology, Vol 1,No 2 ,pp 1-19 N Ø Navisssi, F., (1999)., « Earnings Management Under Price Regulation », Contemporary Accounting Research, Vol 1, No 2, pp. 281- 304. Ø Naz .I, Bhatti . K, Ghafoor . A ,Khan,H. H,(2011)., « Impact of Firm Size and Capital Structure on Earnings Management: Evidence from Pakistan», International Journal of Contemporary Business Studies, Vol 2, No 12, pp 22-31 Ø Nawaeze, T. E., (2002)., « Income-increasing / Income-decreasing accruals: trends and firm characteristics », Working Paper. Ø Nekhili .M (1999)., « Le choix du type et de la maturité de la dette par les firmes françaises », Université de Bourgogne, Finance Contrôle Stratégie, Vol 2, N° 3, septembre 1999, p. 179 - 206. Ø Neter, J., Wasserman,W. and Kutner, M.H. (1989), « Applied Linear Regression Models», Homewood, IL: Richard D. Irwin, Inc Ø Nini. G., Smith. DC et Sufi, A, (2009)., « Creditor control rights and firm investment policy» ,Journal of Financial Economics, Vol 92 pp 400-420 O Ø Olivier, V., (2010), « La gestion du résultat pour atteindre des seuils : un cadre d'analyse», / 46/ 47/ 88/PDF/AFC-2007m 03-GRetSeuils-UnCa%20dre%20DAnalyse.pdf"http://hal.archives-ouvertes.fr/docs/00/46/47/88/PDF/AFC-2007m03-GRetSeuils-UnCa dre DAnalyse.pdf. Ø Olivier, V., (2013), « Gestion du résultat pour éviter de publier une perte : les montants manipulés sont-ils marginaux ? », http:/ /hal.arch ives ouvertes.fr/ docs /00/84/09 /10/PDF/ CCA-2010-Seuils_GRmarginale-PourPublication.pdf. Ø Omri, M. A., et El Aissi, B. A. I., (2007)., «Planification fiscale et valeur de l`entreprise : Cas des entreprises tunisiennes cotées », 6ème colloque international de la recherche en sciences de gestion, ATSG 6, Hammamet (Tunisie), le 1-2-3 Mars 2007. P-Q Ø Pastor, M. J. et Poveda, F., (2005), « Earnings management as an explanation of the equity puzzle », Journal of Financial Economics, papier de travail, Universidad Alicante, vol 19, pp. 109-126. Ø Parfet, W., (2000), « Accounting subjectivity and earnings management: a preparer perspective. », Accounting Horizons, vol 14, no4, pp. 481-488. Ø Pochet, C. et Yeo, H., (2004), « Les comités spécialisés des entreprises françaises cotées : mécanismes de gouvernance ou simples dispositifs esthétiques ? », Comptabilité, contrôle, audit, Tome 10, Vol.2, pp. 31-54. Ø Posner, R. A., (1974), «Theories of economic regulation, Bell journal of economics and management science », Vol 5, pp. 335-358. Ø Patten, D. M et Trompeter, G. M., (2001), «Political costs, environmental disclosure and earnings management: an examination of the impact of catastrophic events on intra-industry management actions », http://papers.ssrn.com/sol3/delivery.cmf? Abs tract_id=273277. Ø Pae, J., (2011), « A synthesis of accrual quality and abnormal accrual models: An empirical implementation », Asia-Pacific Journal of Accounting and Economics, No 18,p p. 27-44. Ø Parienté, S (2013)., « Analyse financière et évaluation d'entreprise: Méthodologie, diagnostic, prix d'offre », books.google.com ovrage Ø Parfet, W., (2000), « Accounting subjectivity and earnings management: a preparer perspective », Accounting Horizons, Vol 14, No 4, pp. 481-488. Ø Piot, C. et Piera, F. M., (2006), « Corporate governance, audit quality and the cost of debt financing of French listed companies », 28 ème congrés de l'Association Francophone de Comptabilité. Ø Pourciau, S., (1993), « Earnings Management and Nonroutine Executive Changes », Journal of Accounting and Economics, Vol 16, pp. 317-336. Ø Petersen, M,A et Rajan, R,G, (1994)., « . - . The benefits of lending relationships: Evidence from small business data», The journal of finance, Vol 49, no 1, pp 3-37,Wiley Online Library Ø Piot C, Missonier F, (2007)., « Corporate governance, audit quality and the costs of debt financing of French listed companies», The European Accounting Review, Vol 10, No 3, pp461-499. Ø Piot,C, (2011)., « Relations d'agence, opportunités de croissance et notoriété de l'auditeur externe : une étude empirique du marche français », publié dans "21ème congres de l'afc, france (2000) http://halshs.archives-ouvertes.fr/docs/00/58/75/01/PDF/PIOT.pdf Ø Prevost, A. K., Skousse, C. J et Rao, R. P, (2008)., « Earnings management and the cost of debt», Working paper , Othio University Ø Qi C.Z, K.R. Subramanyam K.R, Jieying Zhang, J, (2010)., « Accrual quality, bond liquidity, and cost of debt », Working paper. R Ø Raffournier, B., (1990), « La théorie positive de la comptabilité ; une revue de la littérature », Economie et Société ; Série Sciences de Gestion, No 16, pp. 137-166. Ø Roosenboom, P., Goot, T. et Mertens, G., (2003), « Earnings management and initial public offerings: evidence from Netherland s », Journal International of Accounting, Vol 38, No 3, pp.243-266. Ø Reitenga, A. et Tearney, M., (2003), « Mandatory CEO Retirements, Discretionary Accruals, and Corporate Governance Mechanisms », Journal of Accounting, Auditing and Finance, Vol 18, pp. 255-279. Ø Raghuram, Rajan, R et Winton, A (2005),« Covenants and Collateral as Incentives to Monitor»,The Journal of Finance, Vol 50, No 4 ,pp 1113-1146, Wiley Online Library. Ø Recasens. G, (2001)., « Aléa moral, financement par dette bancaire et clémence de la loi sur les défaillances d'entreprises », Revue de l'Association Française de Finance, Vol. 22, No 1, p65-86. Ø Roberts, M.R, Sufi .A ,(2009),. « Renegotiation of financial contracts: Evidence from private credit agreements», Journal of Financial Economics Vol 93 pp 159-184. Ø Roy, D, (1996)., «The demand for external auditing : Size, debt and ownership influences : A replication and extension», Cahier de recherche HEC Montréal N96, pp 09 -22 pages. Ø Richardson, V. J., (1998), «Information asymmetry and earnings management: some evidence», Working paper, www.ssrn.com. S Ø Safdar, H. T,. Hazoor ,.M. S, and Syed, Z. A.S., (2011)., «Impact of Earnings Management on Capital Structure of Non- Financial Companies Listed On (KSE) Pakistan » , Global Business and Management Research: An International Journal , Vol. 3, No. 1, pp. 96-105 Ø Scharpe, S., (1990), « Asymmetric information, Bank lending, and implicit contracts : a Stylized model of customer relationships » , Journal of Finance, Vol 45, pp. 1069-1087. Ø Sengupta, P, (1998)., «Corporate disclosure quality and the cost of debt», The Accounting Review, Vol 73,pp 459-474. Ø Shen C, Huang Y. (2011)., « Effects of earnings management of bank cost of debt », Journal of accounting and finance, Vol.53, pp.235-300. Ø Standard & Poor's, 2005 Corporate Ratings Criteria 2006, Standard & Poor's Inc., http://www2.standardandpoors.com/spf/pdf/fixedincome/corporateratings_2006.pdf Ø Subramanyam, K. R, (1996)., « The pricing of discretionary accruals»,. Journal of Accounting and Economics, Vol 22 , pp249-281. Ø Scott, W. R., (2009), « Financial Accounting Theory, 5th edn, Pearson/Prentice Hall : Canada. » ouvrage Ø Stolowy, H. et Breton, G., (2003), « La gestion des données comptables : Une revue de la littérature », Comptabilité - Contrôle - Audit, Vol 1, No 9, pp. 125-151. Ø Schipper, k., (1989), «Commentary on earnings management », Journal of Accounting Horizons, Vol 3, No 4, pp.91-102. Ø Sloan, R. G., (1996), « Do Stock Prices Fully Reflect Information in Accruals and Cash Flows about Future Earnings? », The Accounting Review, Vol 71, No 3, pp. 289-315. T -V -W -X-Z Ø Takasu. Y (2012)., « Income Smoothing and the Cost of Bank Loans :The Effect of Information Asymmetry», Graduate School of Commerce and Management, Hitotsubashi University ,No.143,working paper. Ø Trablsi .El Gharbi, M , (2009)., « Le Choix De La Source De Dettes Par Les Grandes Firmes : Le Cas Français», Thèse En Cotutelle Internationale, ftp://ftp.univ-orleans.fr/theses/myriam.trabelsi_1766.pdf thése Ø Tahir S.H., Sabir H. M. and Ali S. Z. (2011). Impact of Earnings Management on Capital Structure of Non- Financial Companies Listed On (KSE) Pakistan. Global Business and Management Research: An International Journal, vol 3 , no 1, pp96-105. Ø Teoh, S., Welch, I. et Wong, T., (1998), « Earning management and the post - issue underperformance of seasoned equity offering », Journal of Financial Economics, Vol, 50, pp. 63-100. Ø Thomas, J., (1989).,« Unusual patterns in reported earnings », The Accounting Review, Vol 64, No 4, pp. 773-787. Ø Teoh, S. H., Wong, T. J. et Rao, J., (1998)., « Are accruals during initial public offerings opportunistic? », Review ofAccounting Studies, Vol 3, pp 175-208. Ø Vigneron. L (2008)., « Conditions de financement de la PME et relations bancaires », Journal of Banking and Finance, Thèse pour obtenir le grade de Docteur de l'Université de Lille 2 en Sciences de Gestion, halshs.archives-ouvertes.fr Ø Warner, Jerold,( 1977)., « Bankruptcy costs: Some evidence », Journal of Finance ,Vol 32, pp337-347. Ø Watts, R. et Zimmerman, J., (1990), « Positive accounting theory: A ten year perspective », The Accounting Review, Vol 65, pp.131-156. Ø Warner, J., Watts, R. et Wruck, K., (1988), « Stock Prices and Top Management Changes », Journal of Financial Economics, Vol 20, pp. 461-492. Ø Watts, R et Zimmerman, J., (1978), « Towards a Positive Theory of the Determination of Accounting Standards », The Accounting Review, Vol 53, pp 112-134. Ø Watts, R. L. et Zimmerman, J. L., (1986), « Positive accounting theory », Englewood Cliffs, NJ: Prentice-Hall. Ø Williamson, O. E., (1985), « The Economics institution of capitalism: firms, markets and relational contracting. Mcmillan, The Free Press. http://www.sp.uconn.edu/~langlois/Williamson%20(1985),%20chapter%201.pdf Ø Watts, R. L. et Zimmerman, J. L., (1983), «Agency problems, auditing and the theory of the firm: some empirical evidence », Journal of Law and Economics, Vol 26, No. 3, pp 613-633. Ø Warfield, T., Wild, J. et Wild, K., (1995)., « Managerial ownership, accounting choices and in formativeness of earnings » , Journal of accounting and economics, Vol 20, pp 61-91. Ø Wang, Z., Swift, K. et Lobo, G., (1993)., « Earnings management and the informativeness of accruals adjustments », Working paper, Montana State University. Ø Xie, H., (2001), « The mispricing of abnormal accruals », The Accounting Review, Vol 76, No3, pp 357-373 Ø Xue, Y., (2003)., « Information content of earnings management: evidence from managing earnings to exceed thresholds » , Working paper, www.ssrn.com Ø Zorgui, I, (2009)., « Le choix de financement entre la dette et l'équité : survol de la théorie et application pour les firmes canadiennes de 1998 à 2003 », http://www.archipel.uqam.ca/2312/1/M10927.pdf. Ø Zulkufly, R, (2013)., «Corporate Governance, Shareholder Monitoring and Cost of Debt in Malaysia» International Journal of Social, Human Science and Engineering, Vol7 ,No4, pp494- 505. Annexes Pour le modèle d'étude : Annexe 1

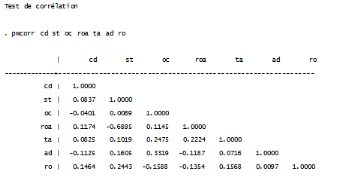

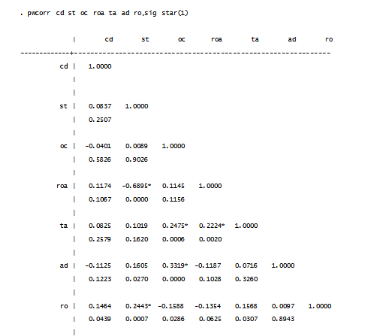

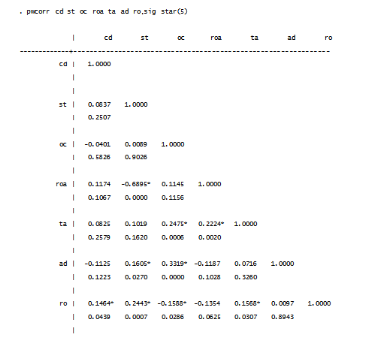

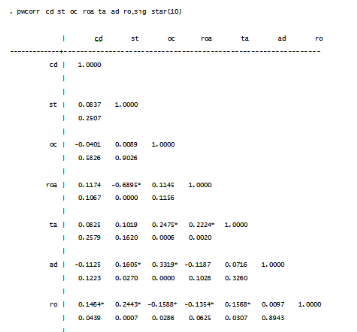

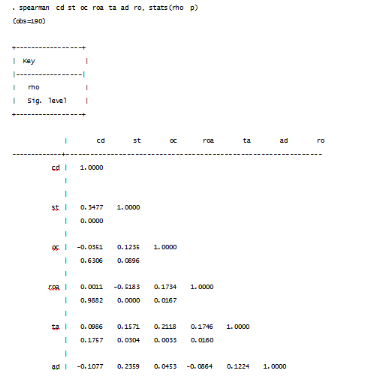

Annexe 2 Test de spearman

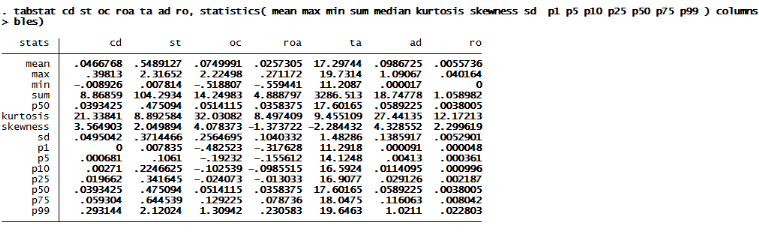

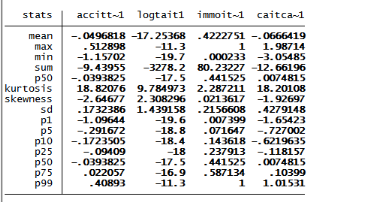

Statistiques descriptive du modèle d'étude : Annexe 3

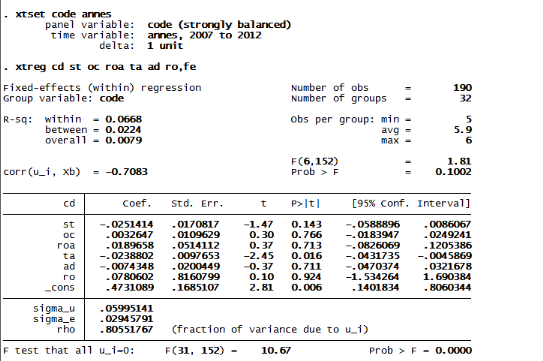

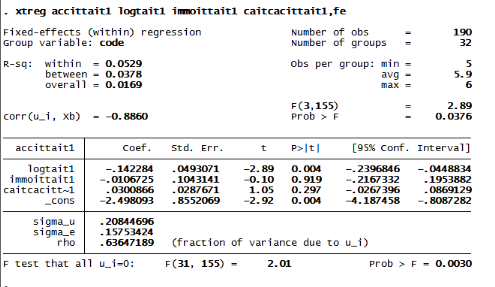

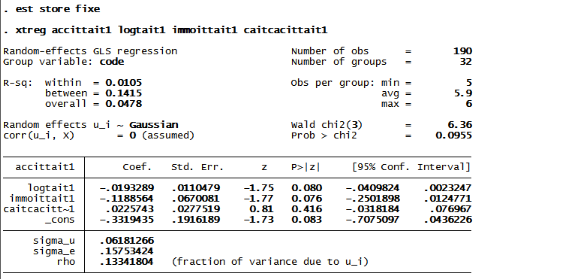

Annexe 4 Régression panel : effet fixe

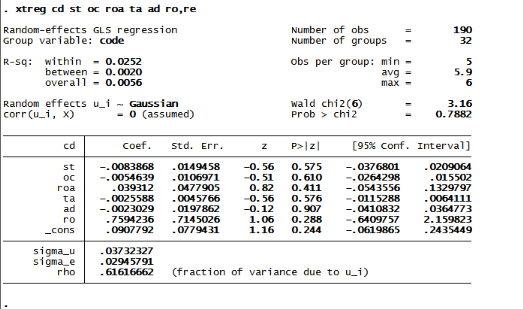

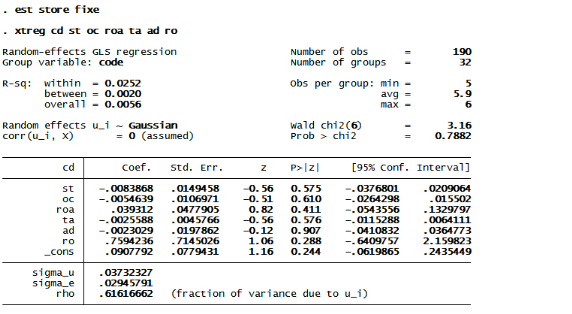

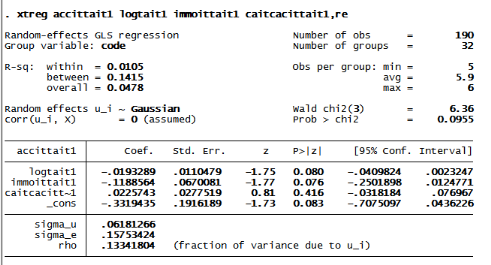

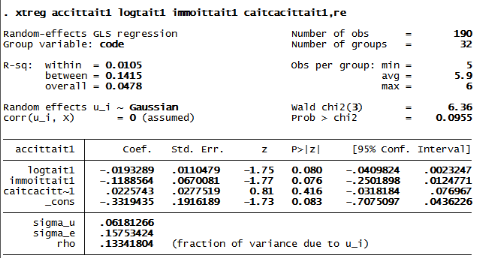

Annexe 5 Régression panel : effet aléatoire

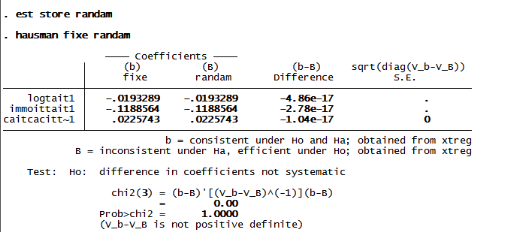

Annexe 6 Test de Housman

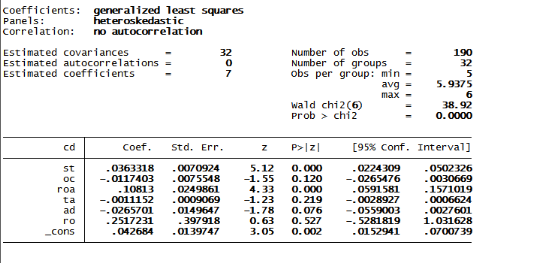

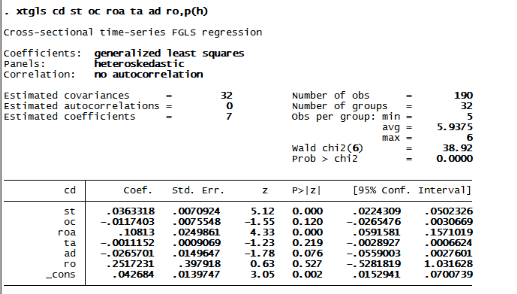

Annexe 7 Estimation du modèle d'étude final

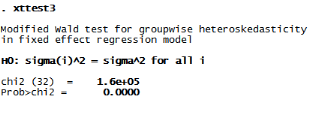

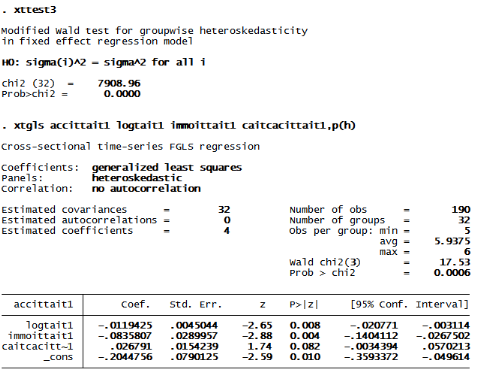

Annexe 8 Pout tester le problème d'heteroxédasticité

en a Prob>chi2 = 0.0000 <0.005 donc on a un problème d'heteroxédasticité Pour la correction le problème d'heteroxédasticité

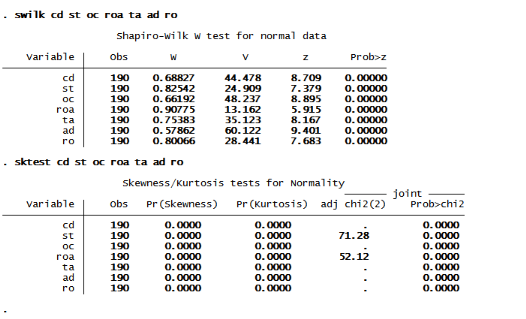

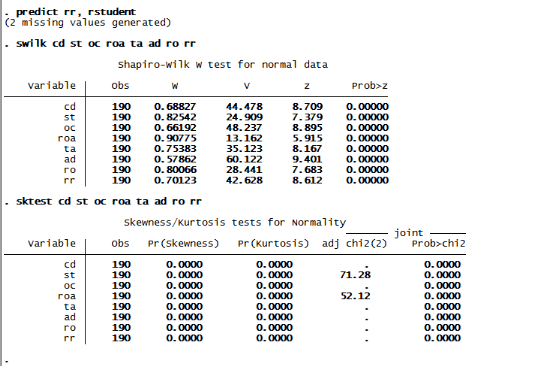

Annexe 9 Test de normalité Annexe 10 Test de normalité des

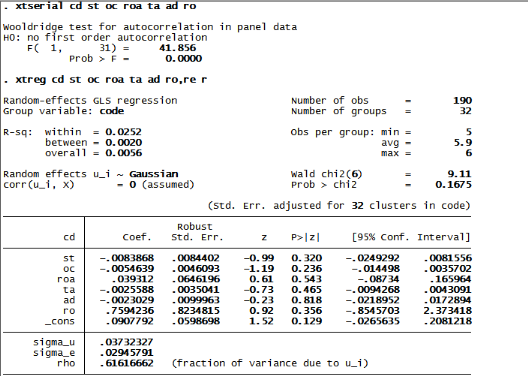

résidus : Annexe 11 Test d'autocorrélation et la commende de correction

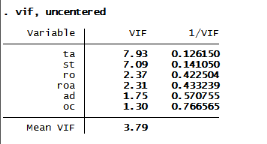

Annexe 12 Test de multicolinarité

v Estimation du modèle de Jones modifié (modèle des accruals) Annexe 13 Statistique descriptive du modèle des accruals

Annexe 14 Régression panel effet fixe

Annexe 15 Régression panel effet aléatoire

Annexe 16 Test de Housman

Annexe 17 Pout tester le problème d'heteroxédasticité

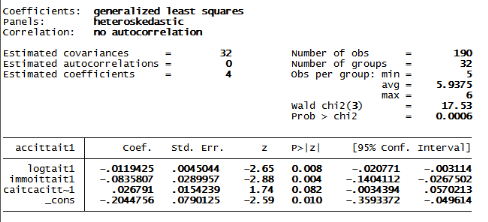

Annexe 18 Estimation final du modèle de Jones modifié (modèle des accruals)

|

|