Assessing the viability of a rural microfinance network: the case of FONGS Finrural( Télécharger le fichier original )par Oniankitan Grégoire AGAI Solvay Brussels School of Economics and Management, Université Libre de Bruxelles - Advanced Master in Microfinance 2012 |

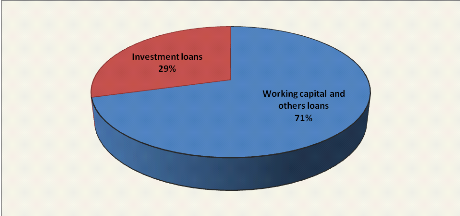

4.3.3.2 CreditLoan products Mainly focused on rural financing, surveyed MFIs extend miscellaneous loan products to meet their members' financial needs. The figure 6 gives an overview of the importance of two main products in 4 MFIs (Tattaguine, Méckhé, Koyli Wirndé and Pékésse) in 2011. Figure 6: Split of loan products in 4 MFIs in 2011 as % of the GLP

Source: Our survey (may-august 2012) The main loan product delivered is the seasonal credit or working capital loan which helps farmers finance their basic activities. This loan terms, varying according to the MFIs, depend essentially on the targeted groups with a maturity betwixt 6 and 15 months and usually a bullet repayment in capital and interest. Likewise, the charged nominal interest rates are comprised between 15% and 25%. If these terms seem common, it appears important to evince some specificity. For example, the MFI of Pékésse caters 4 variants of the seasonal credit regarding loan maturity and including cattle fattening (6 months), agriculture, vegetable production, poultry farming (8 months), and staple food storage (7 months). Small business such as retail sales, handcrafts, agricultural food processing also benefit from working capital loans with different maturity. The second most important loan product is the investment loan with very low interest rate over 12 to 48 months. These kinds of long term loans over 3 years have increased tremendously from 9% to 28% between 2005 and 2010 in Senegal (MEF/DRSSFD, 2010). All the seven MFIs are experiencing this innovative product through the support of the «Fonds d'Appui aux Iniatives Rurales» (FAIR)16(*) which finances agricultural, commercial and handcrafts long term investments such as material, land management etc...without tangible collateral, the loan applicant mother association constituting the moral guarantee. As for the seasonal credit, loan terms (maturity, repayment schedule) are discussed with the borrowers based on the FAIR method which includes small project devising. The interest charged by the FAIR is about 4% for MFIs. In return MFIs are allowed by the FAIR agreement to charge a maximum interest of 12% with no compulsory savings regardless the MFI. Therefore, MFIs can make a maximal margin of about 8% on the investment loans in other to sustain their social action toward their members. Many other loan products exist and are specific to each MEC, depending on the operating area and the real needs of the targeted population. Those loans include energy loans, consumption loans, and education credits, express or emergency loans. Credit policies and Loan size Whereas for regulated MFIs, involving in credit delivery supposes the enforcement of well devised credit policies in order to prevent drifts and subsequently ensure a better credit risk management, the situation seems quite paradoxical at FONGS FINRURAL. Indeed, only one of the surveyed MFIs hold a procedure manual thus hampering the accuracy and the dedication to loan granting processes. Nonetheless, credit committees and the staff members have empiric knowledge about the products supplied and their characteristics. The average duration for a loan application approval is one month in most of the MFIs except for emergency loans; this because some MFIs require a minimum number of loan applications for the credit committee to sitting whilst credit committee of other sits in a monthly base. Acknowledging that for efficiency purposes the maximum duration for a microfinance loan approval should be less than 30 days, it can be deduced that the current situation in the MFIs might undermine good credit policy practices. The loans size varies between MFIs from 5000 FCFA and 5000000 FCFA and depends on the type and the object of the credit. The MFI of Meckhé recorded the highest average loan size (455000 FCFA) over the last four years. For all the loans, no tangible asset is asked to people as guarantee. The main guarantee is the compulsory saving and the minimum capital requirement or savings requirement in the demand deposits account. Is there a risk of cash flow cycle mismatch? The overall remark is that besides the investment credit for which the repayment schedule is split in frequent instalments after one year or 6 months, the others loans are mainly repaid in bullet. If those repayment policies do meet with most of MFIs members, it appears important to stress out that granting always more than 3 months maturity loans with a balloon repayment could jeopardize MFIs. Indeed, the fact to apply yearly or semi-annual instalments may undermine borrowers' incentive to repay back their loans (Buchenau, 2003), thus breaking down the loan repayment culture. Likewise, repaying loans at once in fine in capital and interest may not be affordable for borrowers especially when they cannot get their revenue at once. Another aspect that should be underscored is the loan diversion, specifically the use of seasonal credit for shorter cash flow cycle activities. In Podor for example some beneficiaries invest their seasonal credit in their retail sales, restaurants, handcrafts activities. The mismatch between the disbursement/reimbursement of the loans and the cash flow cycle of households might increase the loan delinquency and MFIs' turnovers accordingly. For Bédécarrats, Baur & Lapenu (2011), the bankruptcy of number of microfinance institutions due to important customers drop out and to the increase in arrears show up that MFI don't always provide adapted financial services such as credit. When can a loan be adapted? Is it when it meets members' needs or when its terms fit the cash flow of households? For the common understanding and numerous scholars such as Pearce, Goodland & Mulder (2004) and Collings, Morduch, Rutherford & Ruthven (2009), a financial product, particularly the credit is adapted not only when it is affordable but also when it is flexible, meaning that disbursement / reimbursement periods meet with the cash flow cycles of households. In agriculture financing especially, flexible credits are crux elements for a well attainment albeit they are likely to worsen loan portfolios and imply liquidity management issues17(*). It is therefore on the responsibility of MFIs and their members to find out the balanced situation which will not put at risk MFIs operations while fulfilling rural households' needs. * 16 Rural Initiatives Support Funds * 17 See http://www.ruralfinance.org/fileadmin/templates/rflc/documents/1114413150253_WB_AIN_07_01.pdf |

|