Assessing the viability of a rural microfinance network: the case of FONGS Finrural( Télécharger le fichier original )par Oniankitan Grégoire AGAI Solvay Brussels School of Economics and Management, Université Libre de Bruxelles - Advanced Master in Microfinance 2012 |

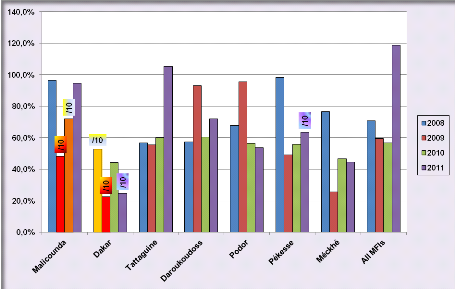

5.1.3 Profitability: Cost Ratio AnalysisThe cost ratio indicator is used to evaluate how much MFIs spend in operating cost to make their income. It also helps to know whether MFIs are losing money or not. The figure 11 shows the cost ratio of the seven MFIs assessed and the Network as a whole. Figure 11: Cost Ratios 2008-2011

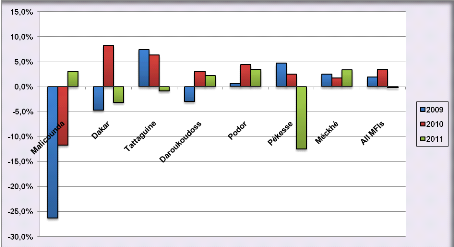

/X: The real value is X times de value on the figure Source: Our survey (may-august 2012) It comes out that the MFIs cost ratios vary inconstantly over year. Most of the MFIs reported below but nearer 100% meaning that they are neither losing money, nor extorting money from their operations. However, opposite trend is witnessed at the MEC FAM of Dakar scoring above 200% except in 2010 when good performance was recorded. It can be deduced an indubitable loss of money at that MFI over years. The impressive cost ratio of the MEC MFR of Pékésse in 2011 (above 600%) is mainly due to a grant training programme and technical assistance they benefited and for which they have contributed. In the same vein, the MEC SAPP of Tattaguine reported an increasing cost ratio meaning excessive expenses given that their portfolio is increasing. The cost ratio of the entire 07 MFIs was minatory in 2011 due exclusively to high operating expenses of the MEC SAPP of Tattaguine and the MEC MFR of Pékésse. The CREC Méckhé presents a relatively soothing cost ratio the last two years (44-46%) despite its impressive negative loan loss provision expenses in 2011. The negative figure of the loan loss provision expenses is due to the important recovery on loan loss provision made by the MFIs for that year. 5.1.4 Sustainability5.1.4.1 Volatile and low Returns on AssetsIt is generally ascertained that the Return on Assets ratio is an important indicator for profitability analysis because it measures the efficiency of managing assets investment and measures the profit gained pertained to the level of investment in total assets18(*). We however recognize that it is also a device for assessing sustainability within a company, especially in MFIs. The evolution of the Returns on assets of the seven MFIs is shown in the figure 12. Figure 12: Returns on Assets 2009-2011

Source: Our survey (may-august 2012) The analysis of the figure shows that while some MFIs present alternatively negative and positive figures of ROA, other report quite stable one over the last three years. Specifically in 2009 and 2010 the MEC MFR of Malicounda obtained high negative values of return on assets mainly attributed to highly negative net incomes. Indeed, net incomes increased negatively between 2009 and 2010 of about 2455% and 9% respectively. This situation might be attributed to the fact that from 2010 the MFI recorded a tremendous increase in its Gross loan portfolio induced by the support of the FAIR. But as most of the loans maturities are one year and the MFI applies a bullet repayment schedule, the loans disbursed in 2010 are repaid partially in 2011. As the MFI apply a cash-based bookkeeping, this induces strong fluctuations in the indicators. Another reason is that during that period, the MFI didn't operate really but kept supporting administrative and staff expenses. The positive figure of ROA observed in 2011 is partially due to the increase in loan portfolio and in interest and fees received from the loans disbursed. The GLP of Dakar is boosted by the external funding (loans and operating expenses). But as the organisation was already struggling with the management of the GLP, this boost has worsened the organisation situation. The ROA of MFR PEKESSE decreased over years from a positive figure (4.7%) in 2009 to a negative situation (-12.5%) in 2011. As aforementioned, the situation in 2011 is to a high investment in staff and board members training along with technical assistance. The inflated personal and administrative expenses (46%) and the loan losses provisioning expenses (9%) at the MEC SAPP of Tattaguine might ascribe the negative figure of their ROA in 2011. For all the remaining MFIs, the ROA are below 10% showing a low profitability. This finding is in line with Lafoucarde et al. (2005) according to whom MFIs in Africa tend to report lower levels of profitability, as measured by return on assets, than MFIs in other global regions. * 18 See http://bizfinance.about.com/od/financialratios/a/Profitability_Ratios.htm |

|