WEBOGRAPHIE

http://www.fenapec.cd/economie-rdc.

TABLE DES MATIERES

Pages

DEDICACE

REMERCIEMENTS

LISTE DES ACRONYMES

0.INTRODUCTION

1

0.1. ETAT DE LA QUESTION

1

0.2. PROBLEMATIQUE

4

0.3. HYPOTHESES

8

0.4. OBJECTIFS DU TRAVAIL

9

0.5. INTERETS DU TRAVAIL

10

0.6. METHODES ET TECHNIQUES

10

0.7. DELIMITATION DU TRAVAIL

10

0.8. SUBDIVISION DU TRAVAIL

11

Chapitre un :

CONSIDERATIONS GENERALES

12

Section 1 : CADRE THEORIQUE

12

I.1.1. Elucidation des concepts usuels

12

I.1.2. Théorie sur le financement d'une

économie

17

I.1.3. Liminaires théoriques de la croissance

économique

23

I.1.4. Notion sur le développement

économique

26

Section 2 : APPROCHE METHODOLOGIQUE

30

I.2.1. Méthode

30

I.2.2. Technique

30

I.2.3. Méthodes utilisées

31

I.2.4. Techniques utilisées et documents

consultés

31

I.2.5. Aperçu théorique de la

modélisation Var

32

Chapitre deux :

FINANCEMENT EXTERIEUR DE L'ECONOMIE

DE LA REPUBLIQUE DEMOCRATIQUE

DU CONGO

38

Section 1 : BREF APERÇU SUR LE MODE DE

FINANCEMENT EXTERIEUR DE L'ECONOMIE CONGOLAISE

38

II.1.1. L'entrée en programme avec les

Institutions de Bretton Woo

38

I.1.2. La suspension de programme avec les

Institutions de Bretton Woods après le pillage de 1991 et 1993

42

II.1.3. Reprise de programme en 2003 avec les

institutions de Bretton Woods

43

II.1.4. L'impact des investissements chinois sur le

financement du développement de la RDC

51

Chapitre trois :

PRESENTATION, ANALYSE

DES DONNEES ET INTERPRETATION

DES RESULTATS

57

Section 1 : PRESENTATION ET ANALYSE DES DONNEES

57

III.1.1. Analyse descriptive des données

59

III.1.2. Analyse de la stationnarité des

données et test de cointégration

61

III.1.3. Estimation et spécification du

modèle

64

III.1.4. Tests économétriques

66

III.1.5. Test de causalité de Grange

68

III.1.6. Conclusion sur la validité du

modèle

68

Section 2 : INTERPRETATION DE RESULTAT

69

Section 3 : DISCUSSION

70

CONCLUSION

73

BIBLIOGRAPHIE

77

WEBOGRAPHIE

80

TABLE DES MATIERES

81

ANNEXES

ANNEXES

1 .Test d'ADF sur le taux de

croissance

|

Null Hypothesis: D(TCE) has a unit root

|

|

|

Exogenous: None

|

|

|

|

Lag Length: 0 (Automatic based on SIC, MAXLAG=7)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

t-Statistic

|

Prob.*

|

|

|

|

|

|

|

|

|

|

|

|

Augmented Dickey-Fuller test statistic

|

-4.989548

|

0.0000

|

|

Test critical values:

|

1% level

|

|

-2.650145

|

|

|

5% level

|

|

-1.953381

|

|

|

10% level

|

|

-1.609798

|

|

|

|

|

|

|

|

|

|

|

|

2 .Test d'ADF sur les Dettes

Extérieures

|

Null Hypothesis: D(DEXT) has a unit root

|

|

|

Exogenous: None

|

|

|

|

Lag Length: 0 (Automatic based on SIC, MAXLAG=7)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

t-Statistic

|

Prob.*

|

|

|

|

|

|

|

|

|

|

|

|

Augmented Dickey-Fuller test statistic

|

-3.428795

|

0.0013

|

|

Test critical values:

|

1% level

|

|

-2.650145

|

|

|

5% level

|

|

-1.953381

|

|

|

10% level

|

|

-1.609798

|

|

|

|

|

|

|

|

|

|

|

|

3. Test d'ADF sur l'Indicateur de

Développement humain

|

Null Hypothesis: D(IDH) has a unit root

|

|

|

Exogenous: Constant

|

|

|

|

Lag Length: 1 (Automatic based on SIC, MAXLAG=7)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

t-Statistic

|

Prob.*

|

|

|

|

|

|

|

|

|

|

|

|

Augmented Dickey-Fuller test statistic

|

-5.225590

|

0.0002

|

|

Test critical values:

|

1% level

|

|

-3.699871

|

|

|

5% level

|

|

-2.976263

|

|

|

10% level

|

|

-2.627420

|

|

|

|

|

|

|

4. Test de stationnarité des résidus

|

Null Hypothesis: RESIDS has a unit root

|

|

|

Exogenous: Constant, Linear Trend

|

|

|

Lag Length: 0 (Automatic based on SIC, MAXLAG=7)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

t-Statistic

|

Prob.*

|

|

|

|

|

|

|

|

|

|

|

|

Augmented Dickey-Fuller test statistic

|

-1.974635

|

0.5902

|

|

Test critical values:

|

1% level

|

|

-4.309824

|

|

|

5% level

|

|

-3.574244

|

|

|

10% level

|

|

-3.221728

|

|

|

|

|

|

|

|

|

|

|

|

|

*MacKinnon (1996) one-sided p-values.

|

|

|

|

|

|

|

|

|

|

|

|

|

Augmented Dickey-Fuller Test Equation

|

|

|

Dependent Variable: D(RESIDS)

|

|

|

Method: Least Squares

|

|

|

|

Date: 06/23/11 Time: 13:55

|

|

|

|

Sample (adjusted): 1981 2009

|

|

|

|

Included observations: 29 after adjustments

|

|

|

|

|

|

|

|

|

|

|

|

|

Variable

|

Coefficient

|

Std. Error

|

t-Statistic

|

Prob.

|

|

|

|

|

|

|

|

|

|

|

|

RESIDS(-1)

|

-0.248202

|

0.125695

|

-1.974635

|

0.0590

|

|

C

|

-1.170425

|

1.384941

|

-0.845108

|

0.4058

|

|

@TREND(1980)

|

0.080759

|

0.081187

|

0.994720

|

0.3290

|

|

|

|

|

|

|

|

|

|

|

|

R-squared

|

0.136403

|

Mean dependent var

|

0.070216

|

|

Adjusted R-squared

|

0.069973

|

S.D. dependent var

|

3.638580

|

|

S.E. of regression

|

3.508971

|

Akaike info criterion

|

5.446220

|

|

Sum squared resid

|

320.1348

|

Schwarz criterion

|

5.587664

|

|

Log likelihood

|

-75.97019

|

F-statistic

|

2.053324

|

|

Durbin-Watson stat

|

1.769849

|

Prob(F-statistic)

|

0.148608

|

|

|

|

|

|

5. Estimation du Modèle Var

|

Vector Autoregression Estimates

|

|

|

Date: 06/23/11 Time: 14:06

|

|

|

Sample (adjusted): 1981 2009

|

|

|

Included observations: 29 after adjustments

|

|

Standard errors in ( ) & t-statistics in [ ]

|

|

|

|

|

|

|

|

|

|

TCE

|

DEXT

|

IDH

|

|

|

|

|

|

|

|

|

|

TCE(-1)

|

0.765832

|

40.80178

|

1.76E-06

|

|

(0.11910)

|

(22.3547)

|

(0.00019)

|

|

[ 6.43001]

|

[ 1.82520]

|

[ 0.00910]

|

|

|

|

|

|

DEXT(-1)

|

-0.001056

|

1.015734

|

-2.83E-06

|

|

(0.00063)

|

(0.11895)

|

(1.0E-06)

|

|

[-1.66641]

|

[ 8.53944]

|

[-2.74922]

|

|

|

|

|

|

IDH(-1)

|

-138.1215

|

6640.172

|

0.536359

|

|

(83.1282)

|

(15602.6)

|

(0.13509)

|

|

[-1.66155]

|

[ 0.42558]

|

[ 3.97052]

|

|

|

|

|

|

C

|

62.89689

|

-2459.681

|

0.204382

|

|

(37.3664)

|

(7013.41)

|

(0.06072)

|

|

[ 1.68325]

|

[-0.35071]

|

[ 3.36589]

|

|

|

|

|

|

|

|

|

|

R-squared

|

0.653557

|

0.924713

|

0.888404

|

|

Adj. R-squared

|

0.611984

|

0.915679

|

0.875012

|

|

Sum sq. resids

|

298.6585

|

10521298

|

0.000789

|

|

S.E. equation

|

3.456348

|

648.7310

|

0.005617

|

|

F-statistic

|

15.72065

|

102.3545

|

66.34074

|

|

Log likelihood

|

-74.96329

|

-226.7727

|

111.2815

|

|

Akaike AIC

|

5.445744

|

15.91536

|

-7.398721

|

|

Schwarz SC

|

5.634336

|

16.10395

|

-7.210129

|

|

Mean dependent

|

-0.113674

|

7975.702

|

0.395448

|

|

S.D. dependent

|

5.548716

|

2234.067

|

0.015887

|

|

|

|

|

|

|

|

|

|

Determinant resid covariance (dof adj.)

|

149.2095

|

|

|

Determinant resid covariance

|

95.59224

|

|

|

Log likelihood

|

-189.5690

|

|

|

Akaike information criterion

|

13.90131

|

|

|

Schwarz criterion

|

14.46709

|

|

|

|

|

|

|

|

|

|

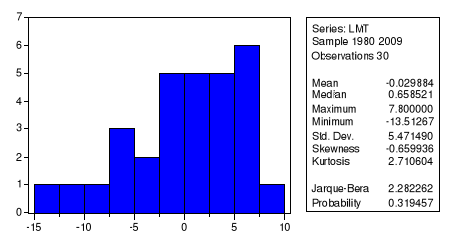

6. Test de normalite de Jarque

Bera(jb)

251658240

7. Test du multiplicateur de la grange (lm

test)

|

Breusch-Godfrey Serial Correlation LM Test:

|

|

|

|

|

|

|

|

|

|

|

|

|

F-statistic

|

1.407955

|

Probability

|

0.262376

|

|

Obs*R-squared

|

15.89141

|

Probability

|

0.196261

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Test Equation:

|

|

|

|

Dependent Variable: RESID

|

|

|

|

Method: Least Squares

|

|

|

|

Date: 07/06/11 Time: 22:08

|

|

|

|

Presample missing value lagged residuals set to zero.

|

|

|

|

|

|

|

|

|

|

|

|

Variable

|

Coefficient

|

Std. Error

|

t-Statistic

|

Prob.

|

|

|

|

|

|

|

|

|

|

|

|

C

|

11.36249

|

14.30970

|

0.794041

|

0.4396

|

|

DEXT

|

0.037762

|

0.150731

|

0.250524

|

0.8056

|

|

IDH

|

-28.13148

|

35.96178

|

-0.782261

|

0.4462

|

|

RESID(-1)

|

0.107888

|

0.262642

|

0.410782

|

0.6870

|

|

RESID(-2)

|

-0.300813

|

0.264707

|

-1.136398

|

0.2736

|

|

RESID(-3)

|

-0.139917

|

0.275094

|

-0.508616

|

0.6184

|

|

RESID(-4)

|

-0.435843

|

0.274397

|

-1.588363

|

0.1331

|

|

RESID(-5)

|

-0.440951

|

0.288459

|

-1.528641

|

0.1472

|

|

RESID(-6)

|

-0.412420

|

0.306563

|

-1.345301

|

0.1985

|

|

RESID(-7)

|

-0.175219

|

0.312722

|

-0.560301

|

0.5835

|

|

RESID(-8)

|

-0.019567

|

0.301011

|

-0.065006

|

0.9490

|

|

RESID(-9)

|

-0.191976

|

0.276954

|

-0.693167

|

0.4988

|

|

RESID(-10)

|

-0.084845

|

0.286107

|

-0.296550

|

0.7709

|

|

RESID(-11)

|

-0.266833

|

0.286995

|

-0.929748

|

0.3672

|

|

RESID(-12)

|

0.011530

|

0.303333

|

0.038011

|

0.9702

|

|

|

|

|

|

|

|

|

|

|

|

R-squared

|

0.529714

|

Mean dependent var

|

5.92E-17

|

|

Adjusted R-squared

|

0.090780

|

S.D. dependent var

|

3.083307

|

|

S.E. of regression

|

2.940028

|

Akaike info criterion

|

5.301568

|

|

Sum squared resid

|

129.6564

|

Schwarz criterion

|

6.002166

|

|

Log likelihood

|

-64.52352

|

F-statistic

|

1.206818

|

|

Durbin-Watson stat

|

1.959952

|

Prob(F-statistic)

|

0.360242

|

|

|

|

|

|

|

|

|

|

|

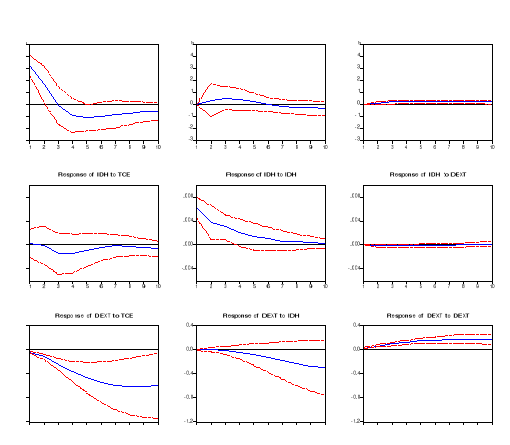

2516556808. Impact du choc entre les variables

(réponses impulsionnelles)

|